Data Analysis

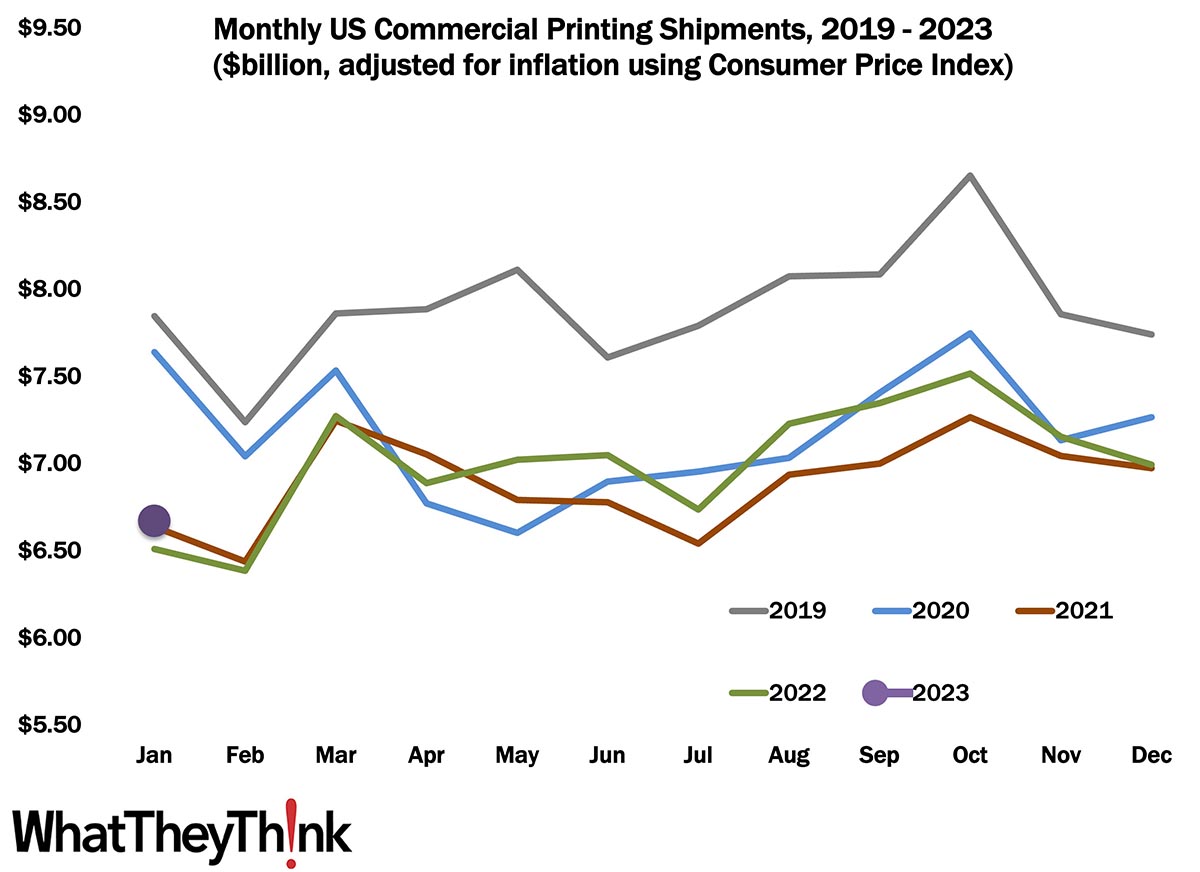

August Shipments: …And We’re Up Again

Published: October 27, 2023

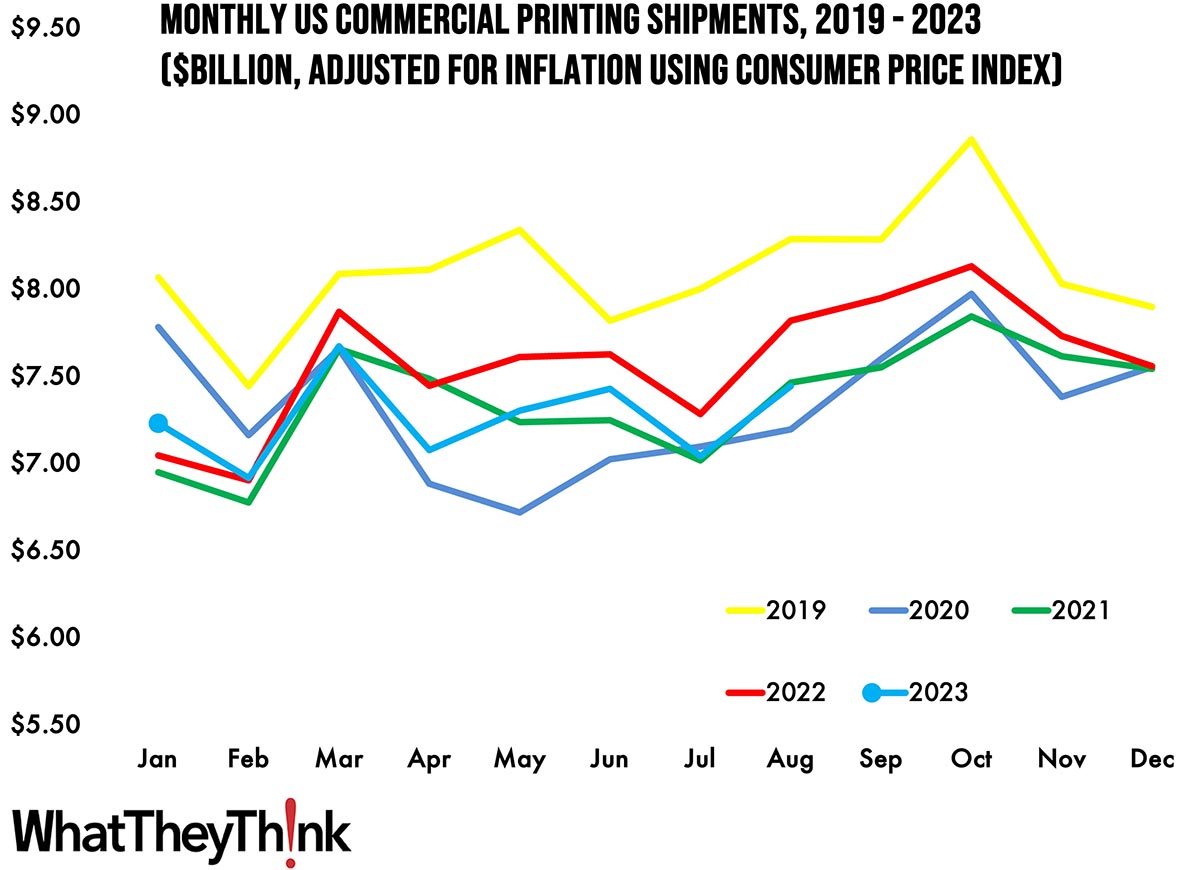

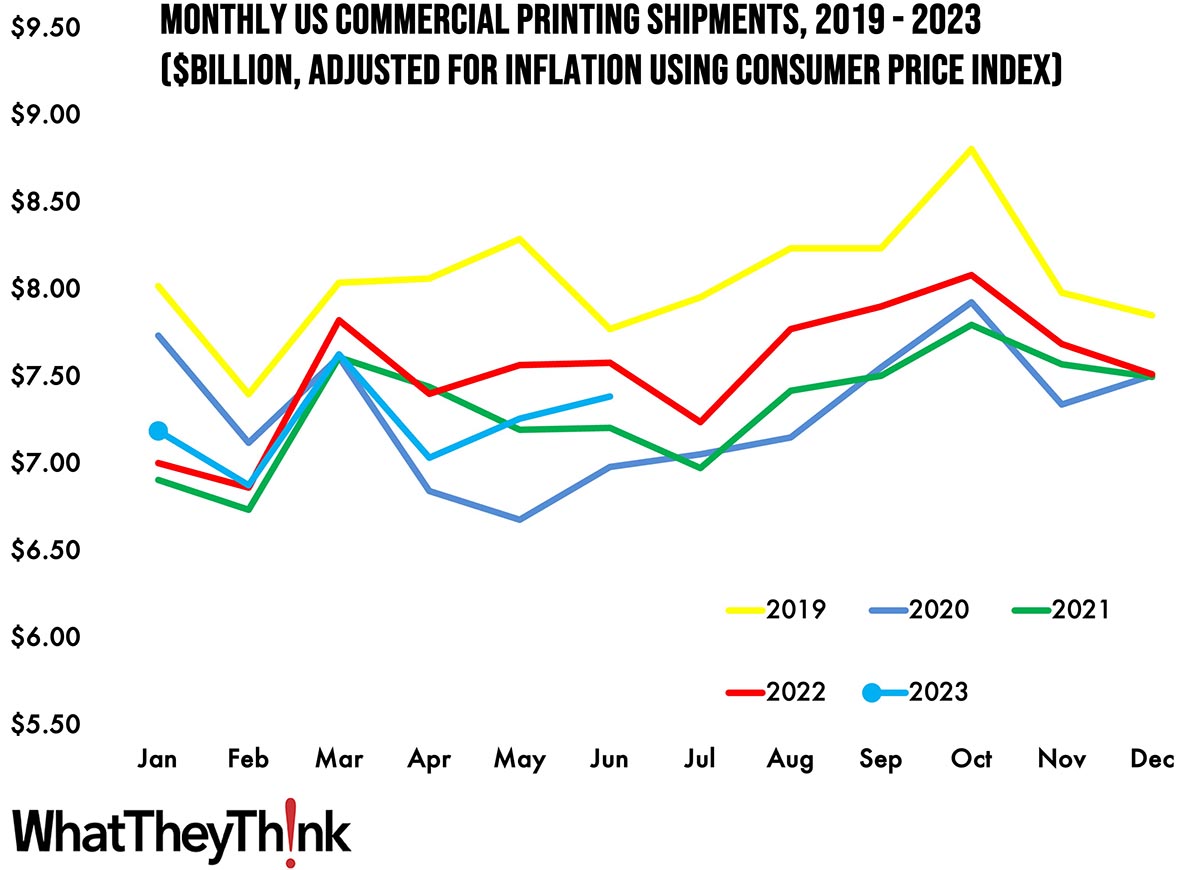

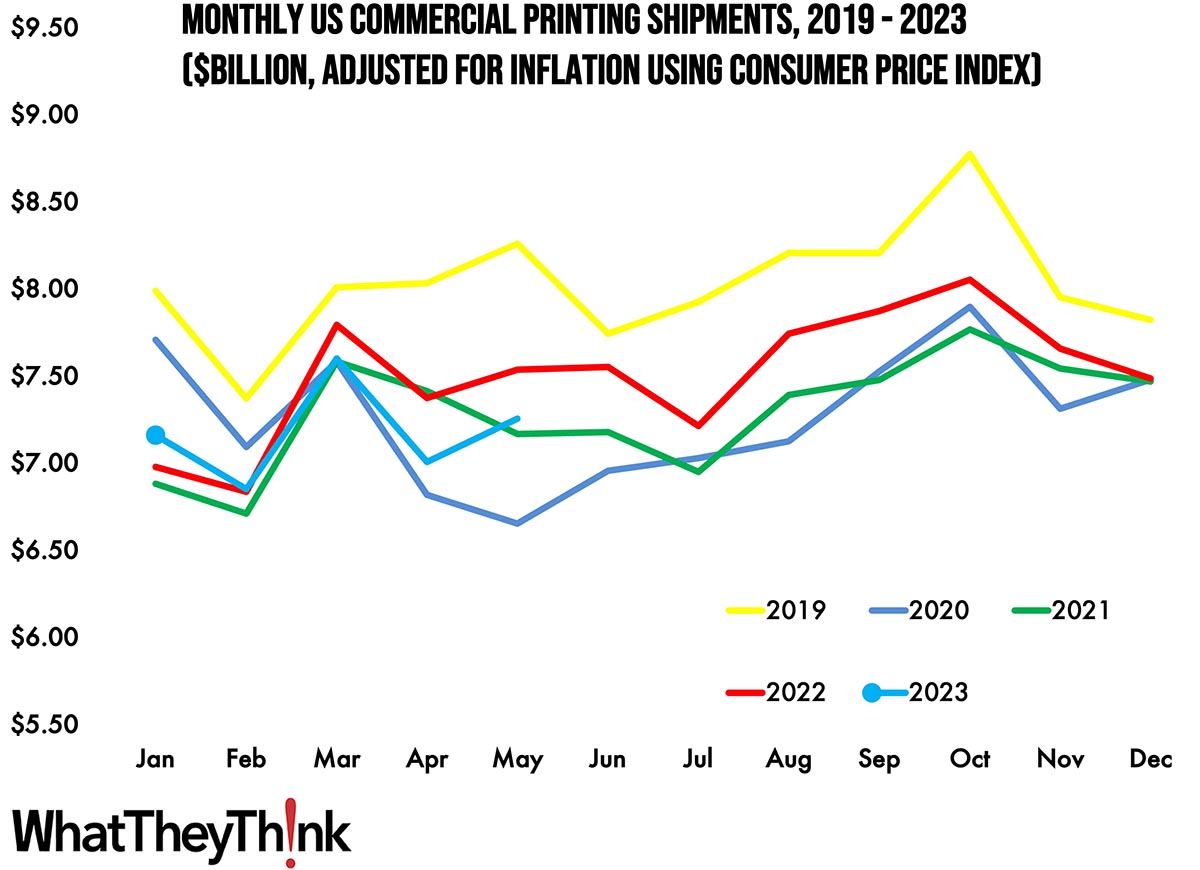

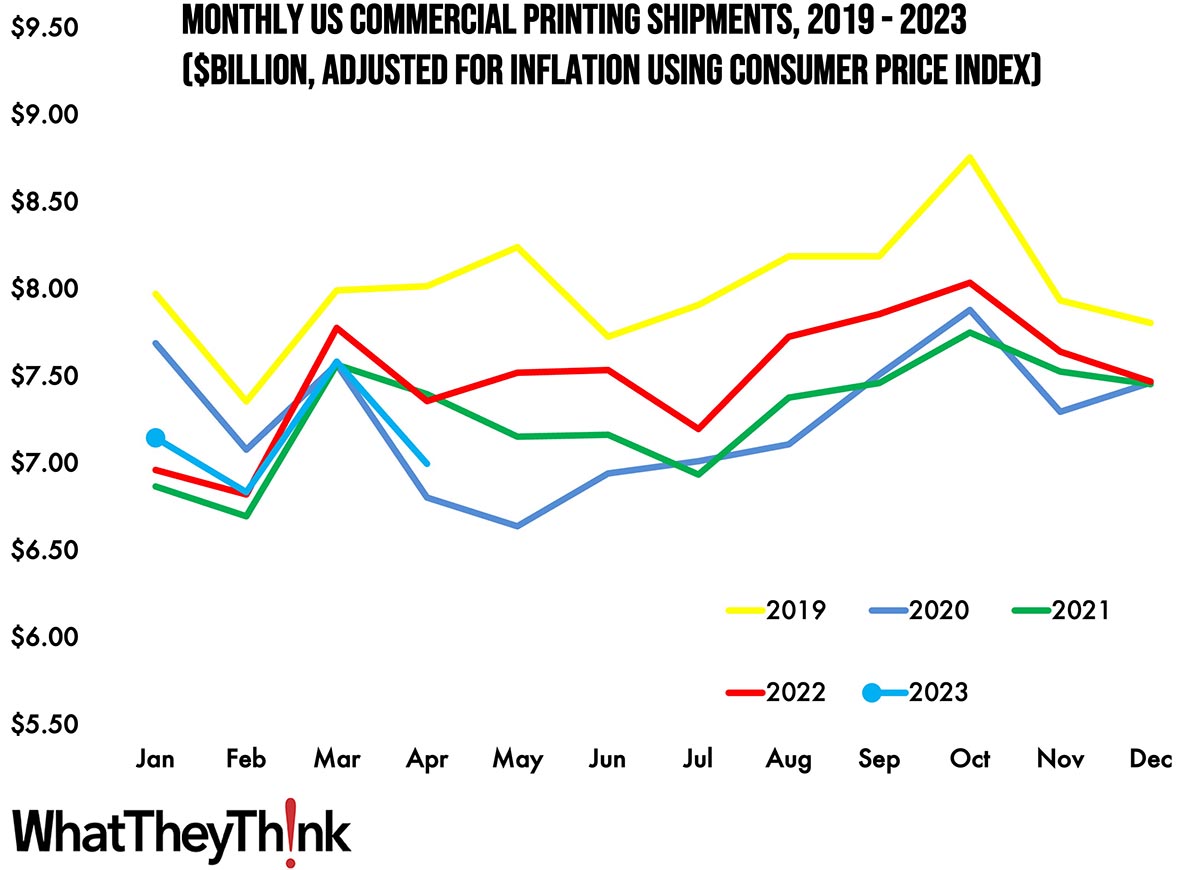

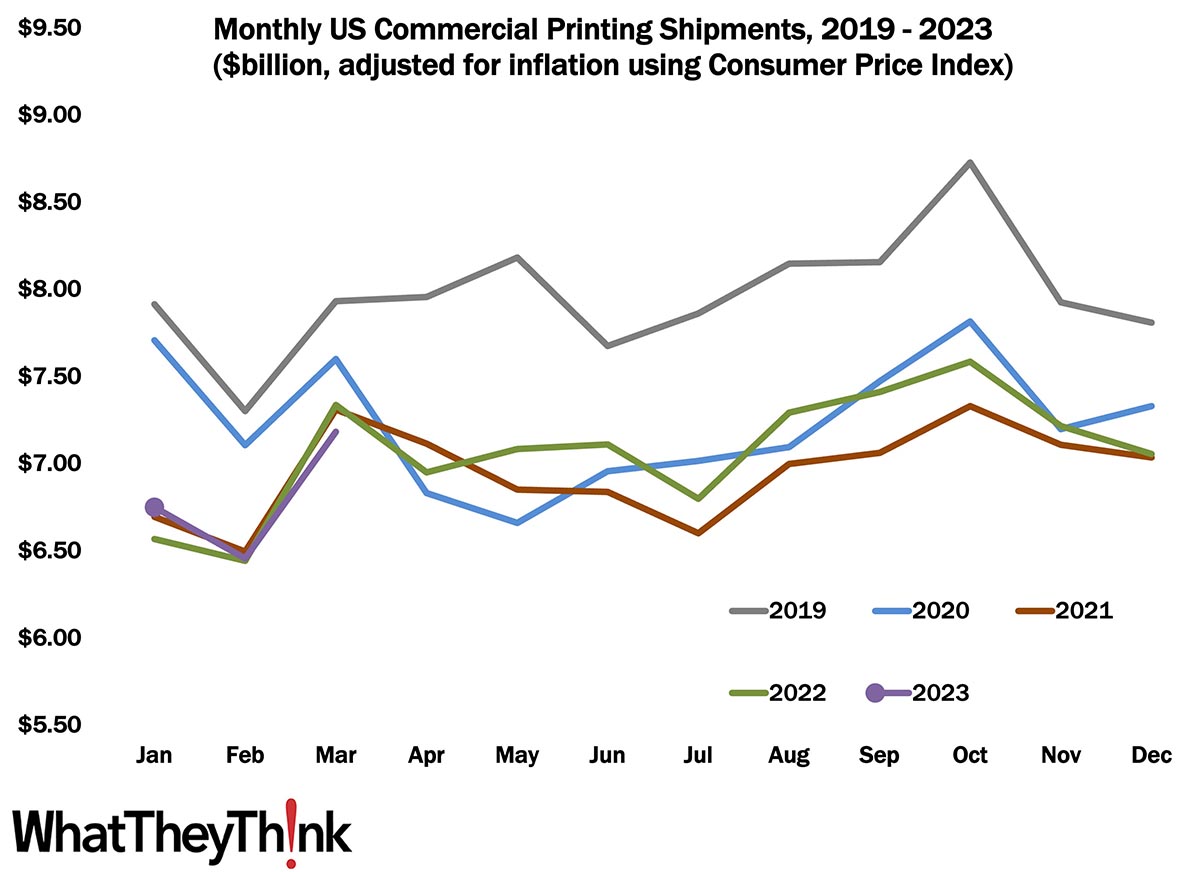

August 2023 printing shipments came in at $7.44 billion, up from July’s $7.04 billion. Full Analysis

Book Printing Establishments—2010–2021

Published: October 20, 2023

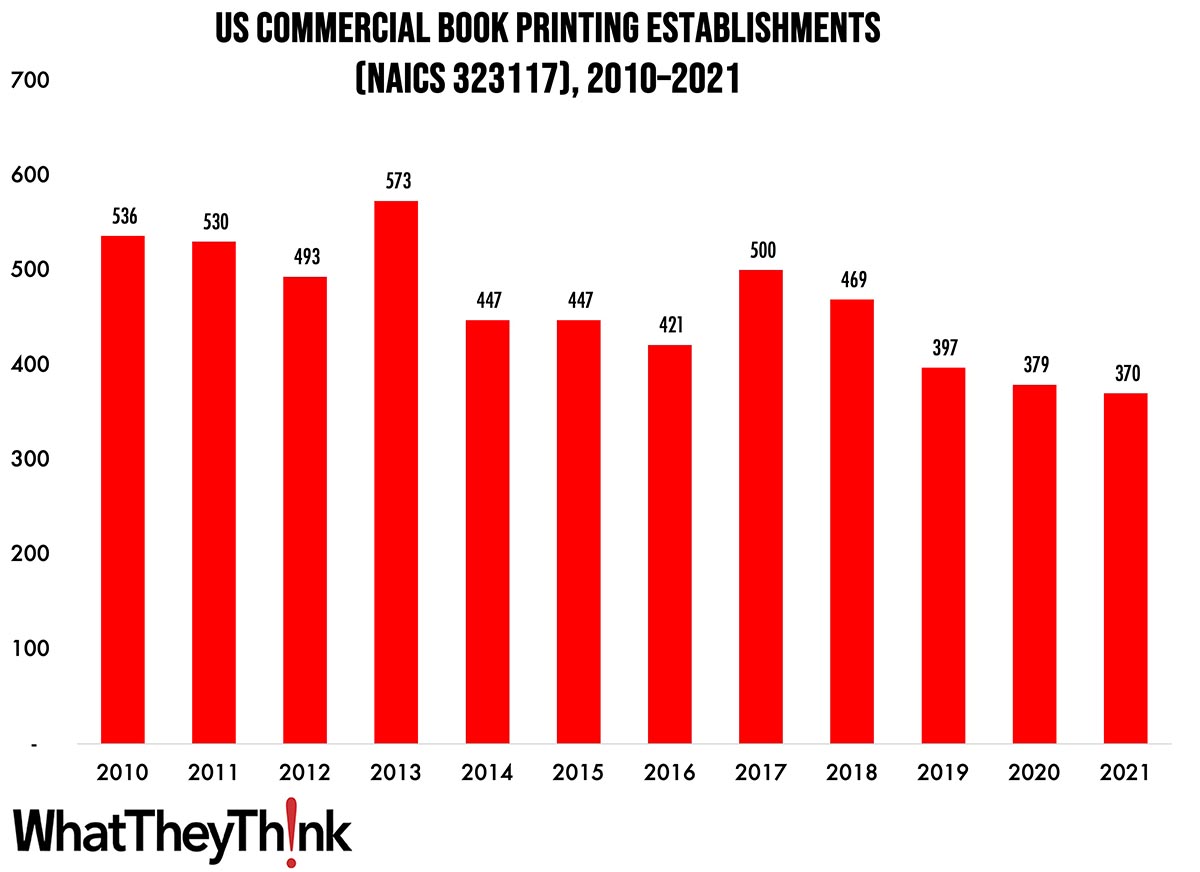

According to the latest, recently released edition of County Business Patterns, in 2021 there were 370 establishments in NAICS 323117 (Commercial Book Printing). This represents a decrease of 31% since 2010—but a decrease of -2.4% from 2020. In macro news, AIA’s Architecture Billings Index (ABI) indicates that demand for design services decelerated in September, boding ill for commercial real estate construction and thus signage projects. Full Analysis

Turnover and Employment in Print in Europe—Romania

Published: October 17, 2023

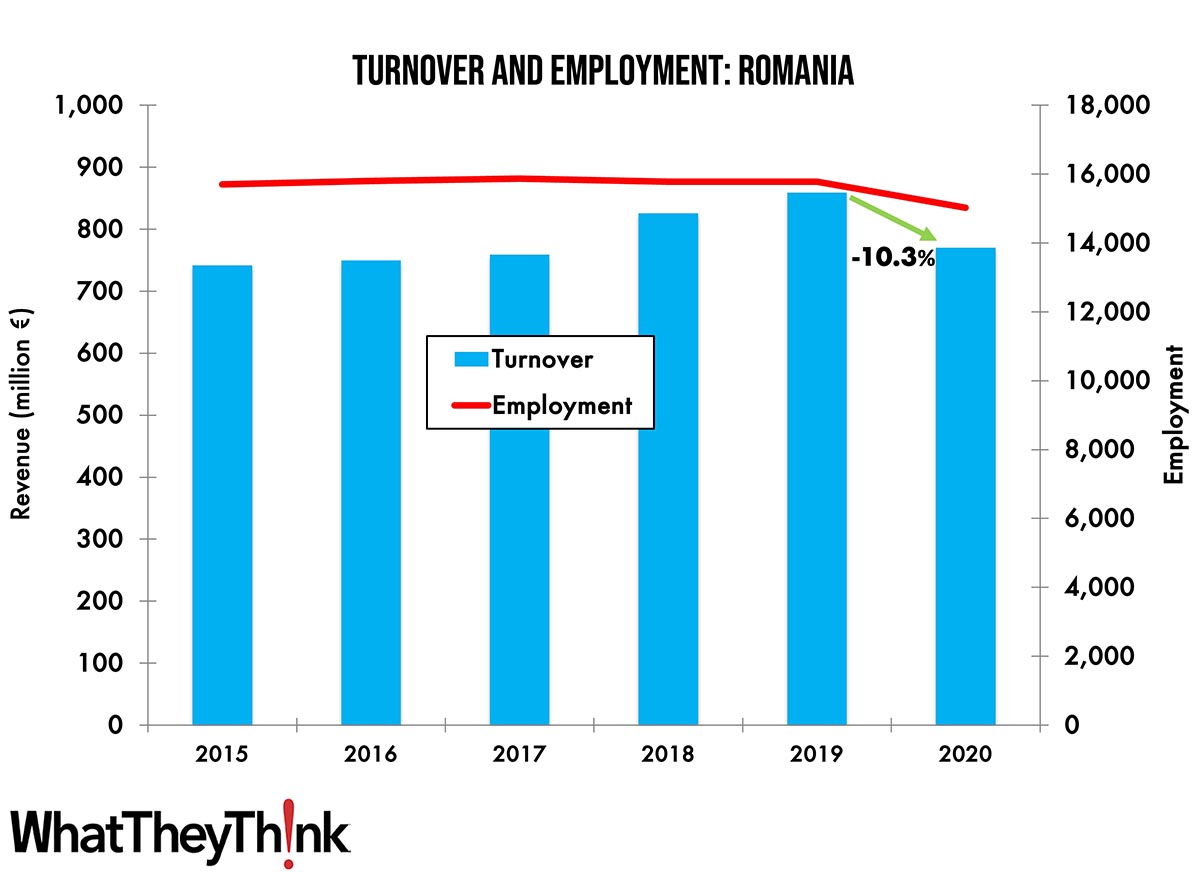

This bi-weekly series of short articles aims to shed a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Romania, the fourth-largest printing industry by turnover in Central and Eastern Europe. Full Analysis

Q2 Industry Profits: The Latest From the Two Cities

Published: October 13, 2023

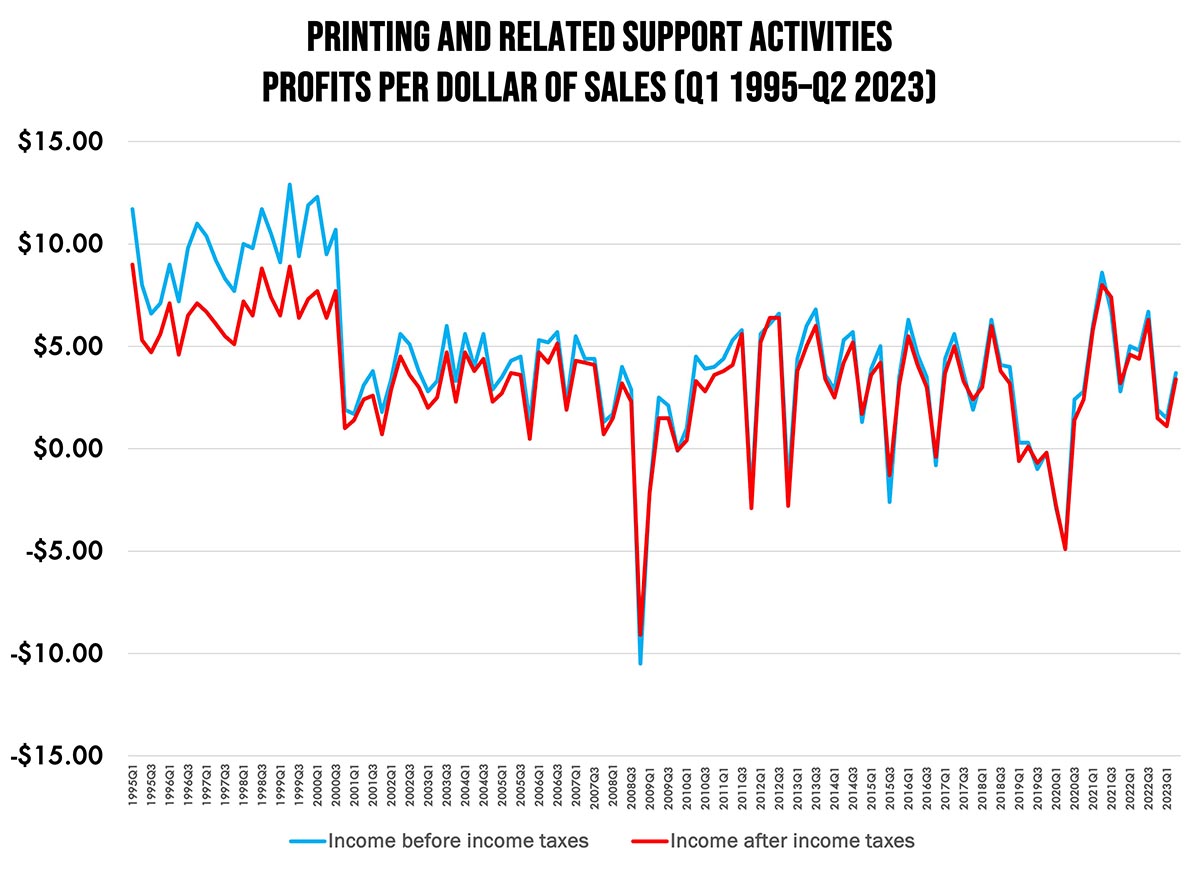

Quarter-over-quarter profit margin data can be fairly noisy but we’re on a general upward trend since the trough of the pandemic. Full Analysis

Tales from the Database: A Complete Package?

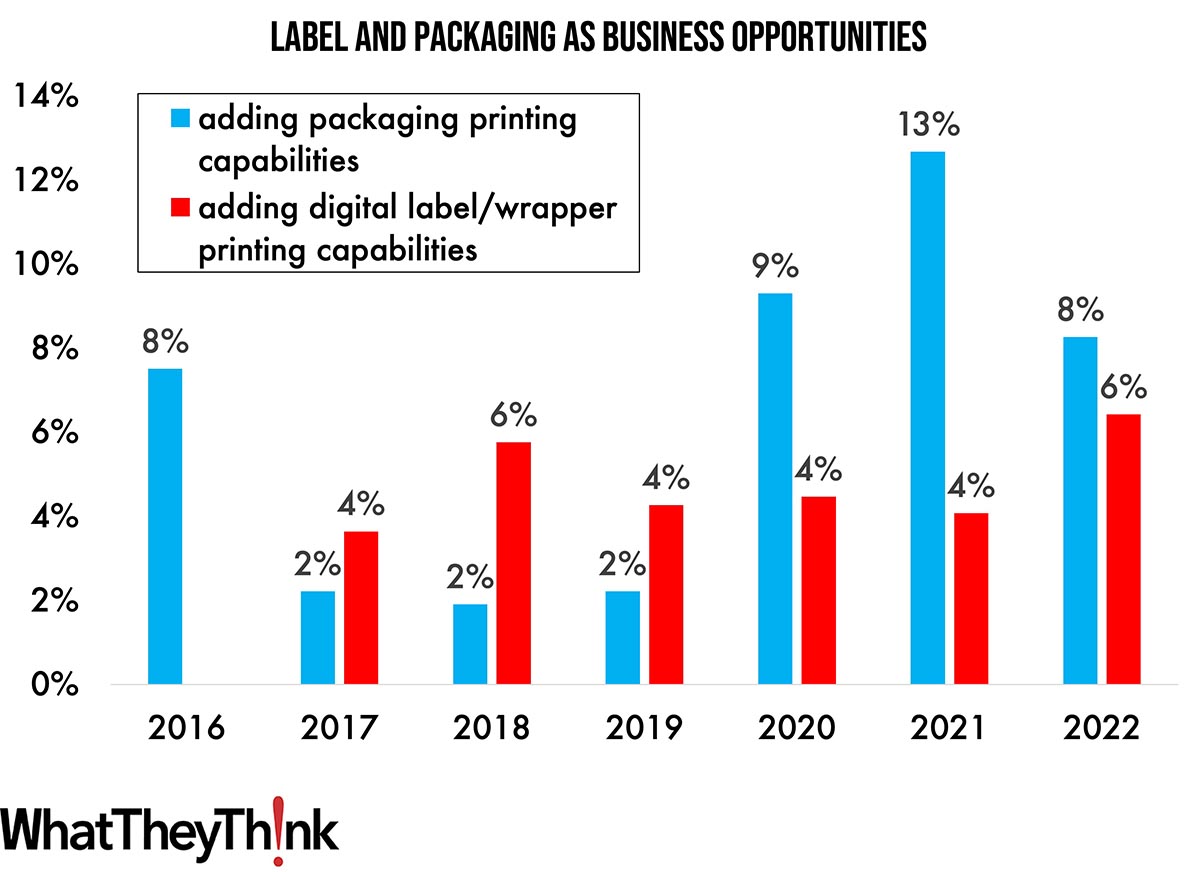

Published: October 6, 2023

Drawing on six years’ worth of Print Business Outlook surveys, our “Tales from the Database” series looks at historical data to see if we can spot any particular hardware, software or business trends. In this installment, we turn our attention to labels and packaging. Full Analysis

Screen Printing Establishments—2010–2020

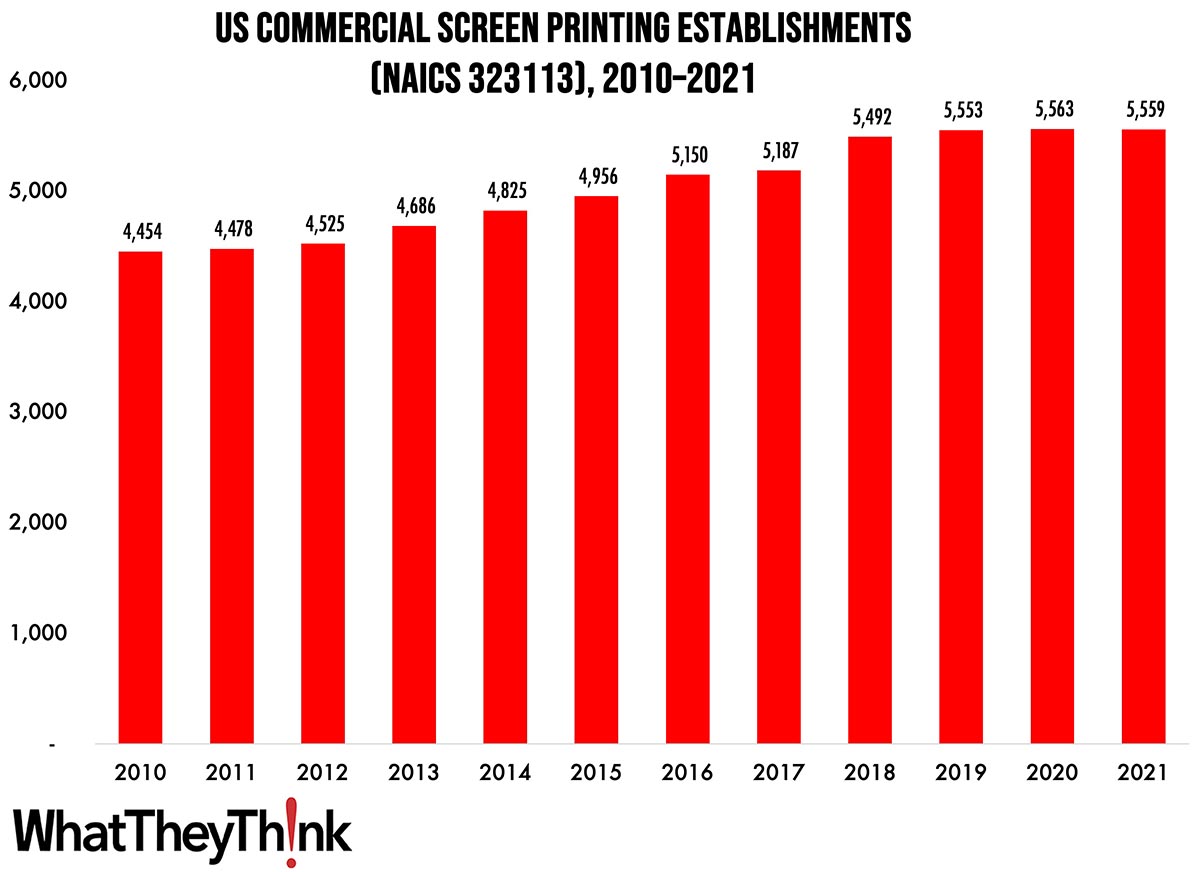

Published: September 29, 2023

According to the latest, recently released edition of County Business Patterns, in 2021 there were 5,559 establishments in NAICS 323113 (Commercial Screen Printing). This represents an increase of 25% since 2010—but a decrease of -0.1% from 2020. In macro news, the third estimate of Q2 GDP is unchanged, but with some subtle changes “under the hood.” Full Analysis

Turnover and Employment in Print in Europe—Switzerland

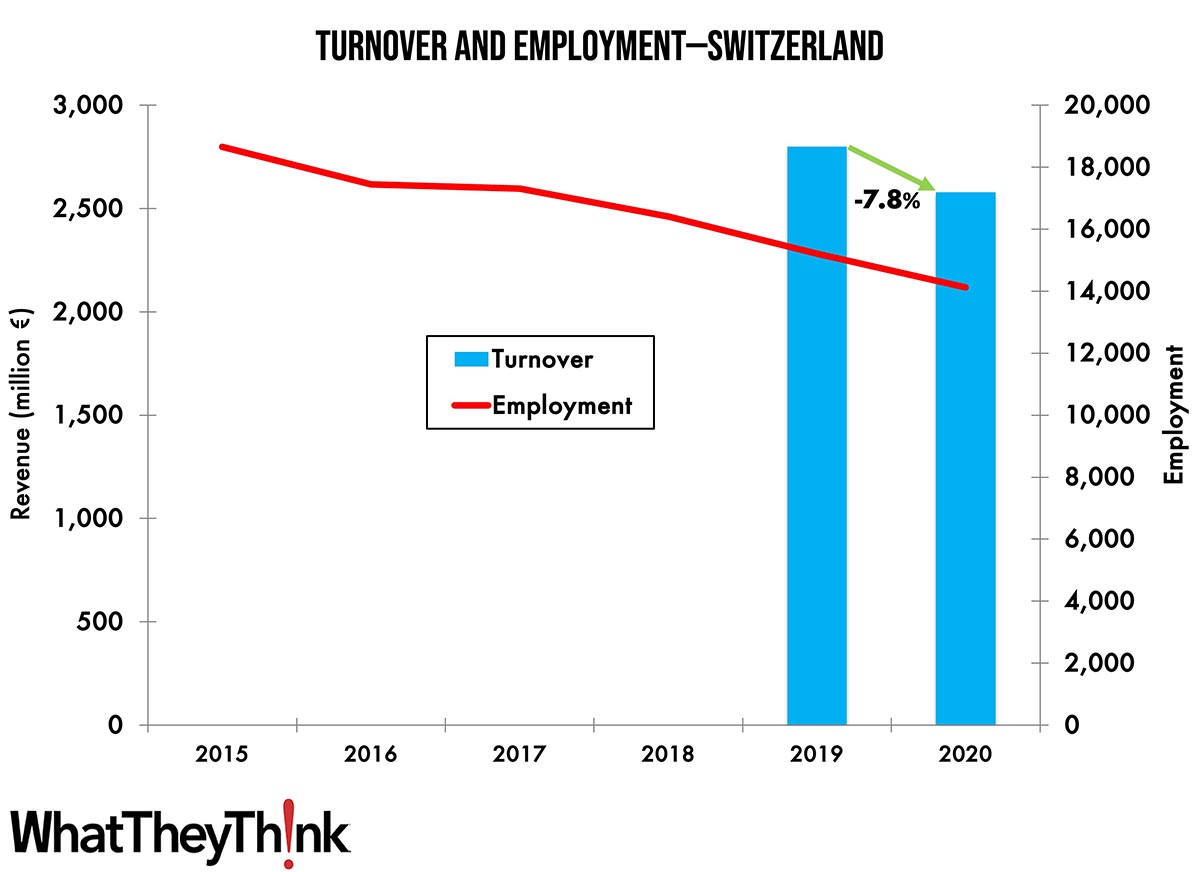

Published: September 27, 2023

This bi-weekly series of short articles aims to shed a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Switzerland, the eighth-largest printing industry by turnover in Europe. Full Analysis

July Shipments: Down, Down We Go

Published: September 22, 2023

In a year that continues to surprise, July 2023 printing shipments came in at $7.04 billion, down from June’s $7.40 billion. Full Analysis

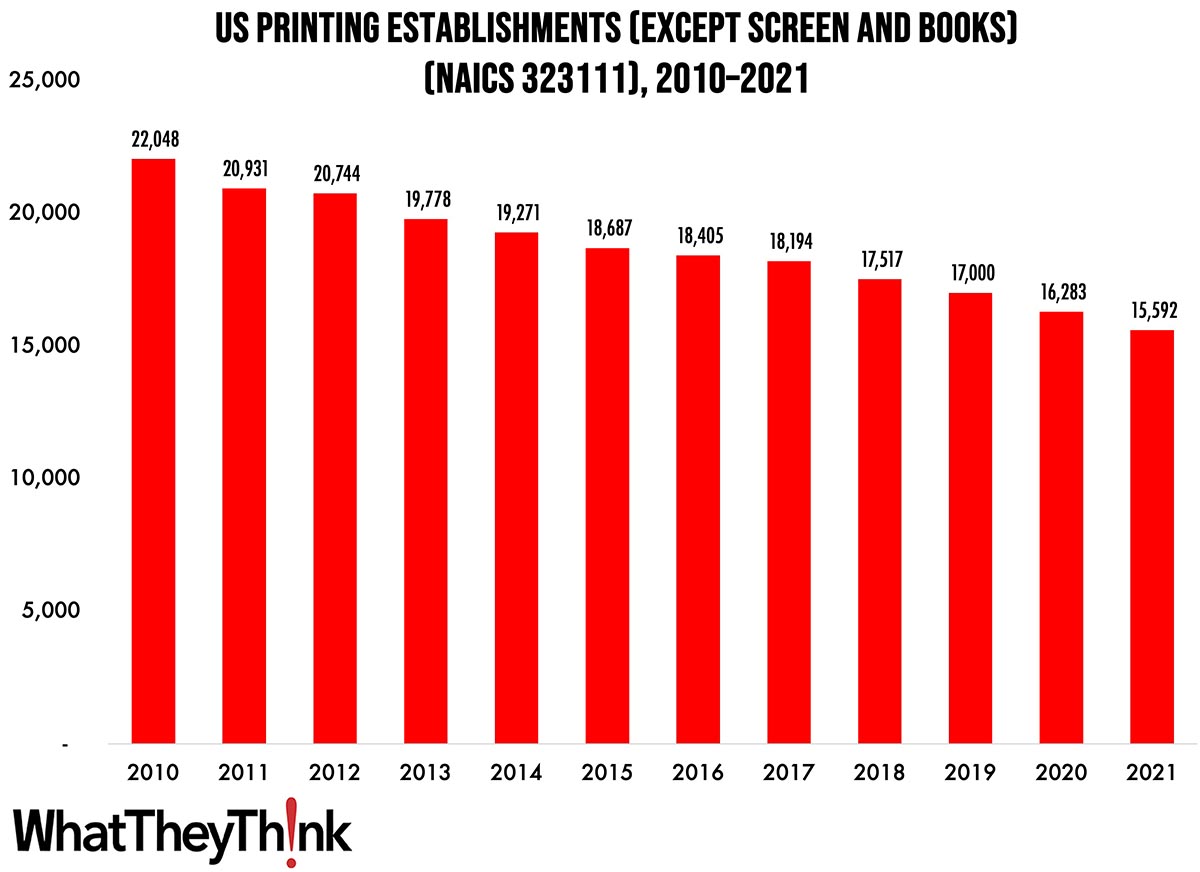

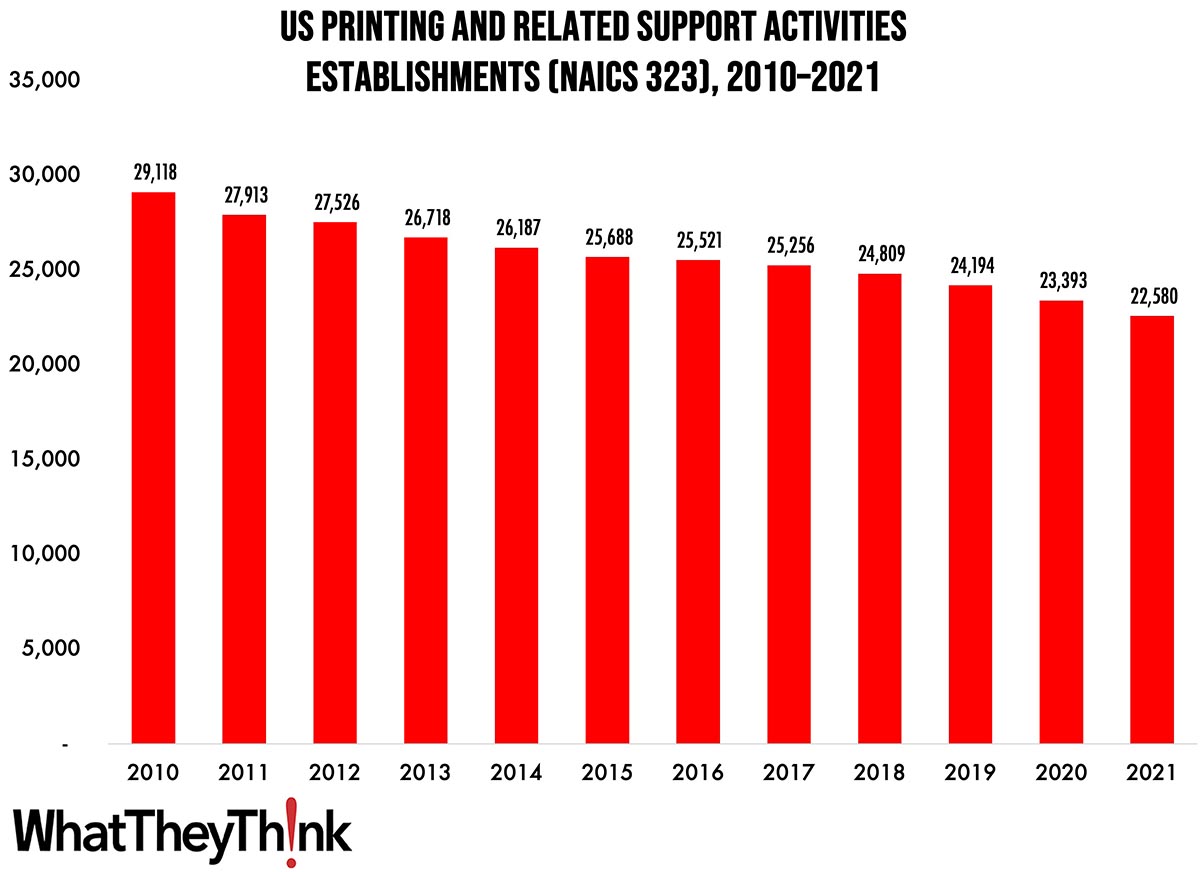

Commercial Printing Establishments—2010–2021

Published: September 15, 2023

According to the latest, recently released edition of County Business Patterns, in 2021 there were 15,592 establishments in NAICS 323111 (Commercial Printing except Screen and Books). This represents a decline of 26% since 2010. In macro news, inflation is alas up. Full Analysis

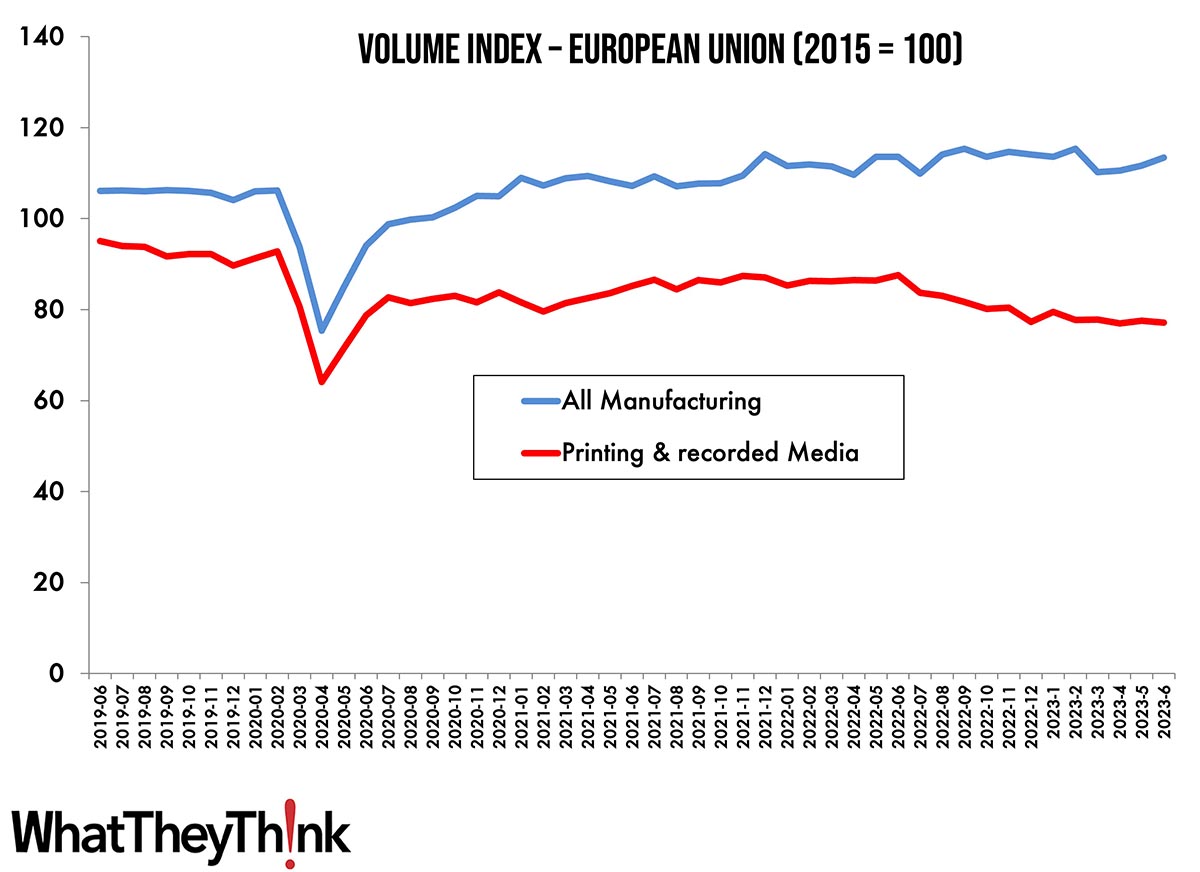

European Print Volume Trends

Published: September 12, 2023

European section editor Ralf Schlözer takes a break from the Europen country-by-country look at turnover and employment to provide a bigger-picture look at print volumes in Europe pre- and post-pandemic. Full Analysis

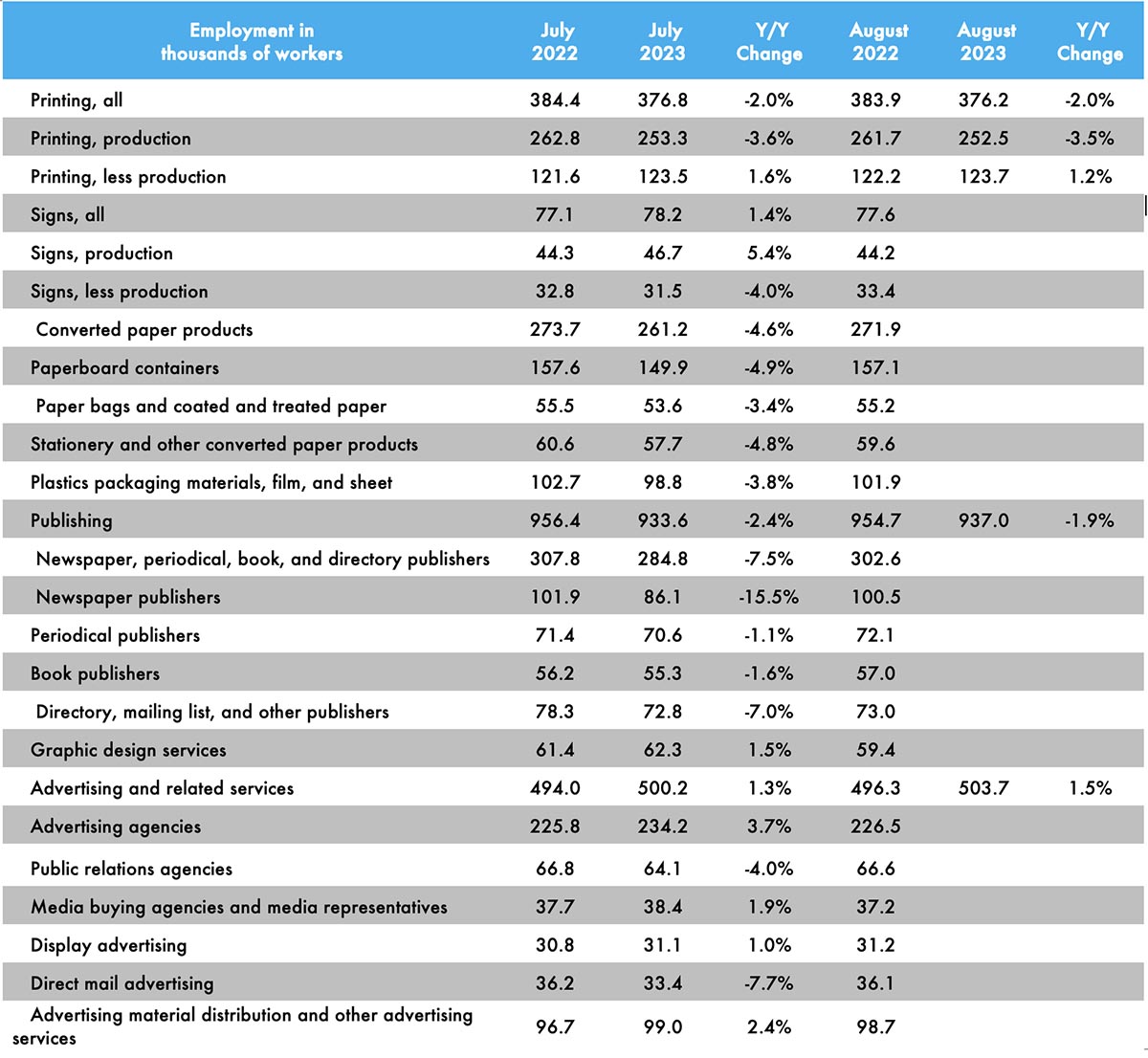

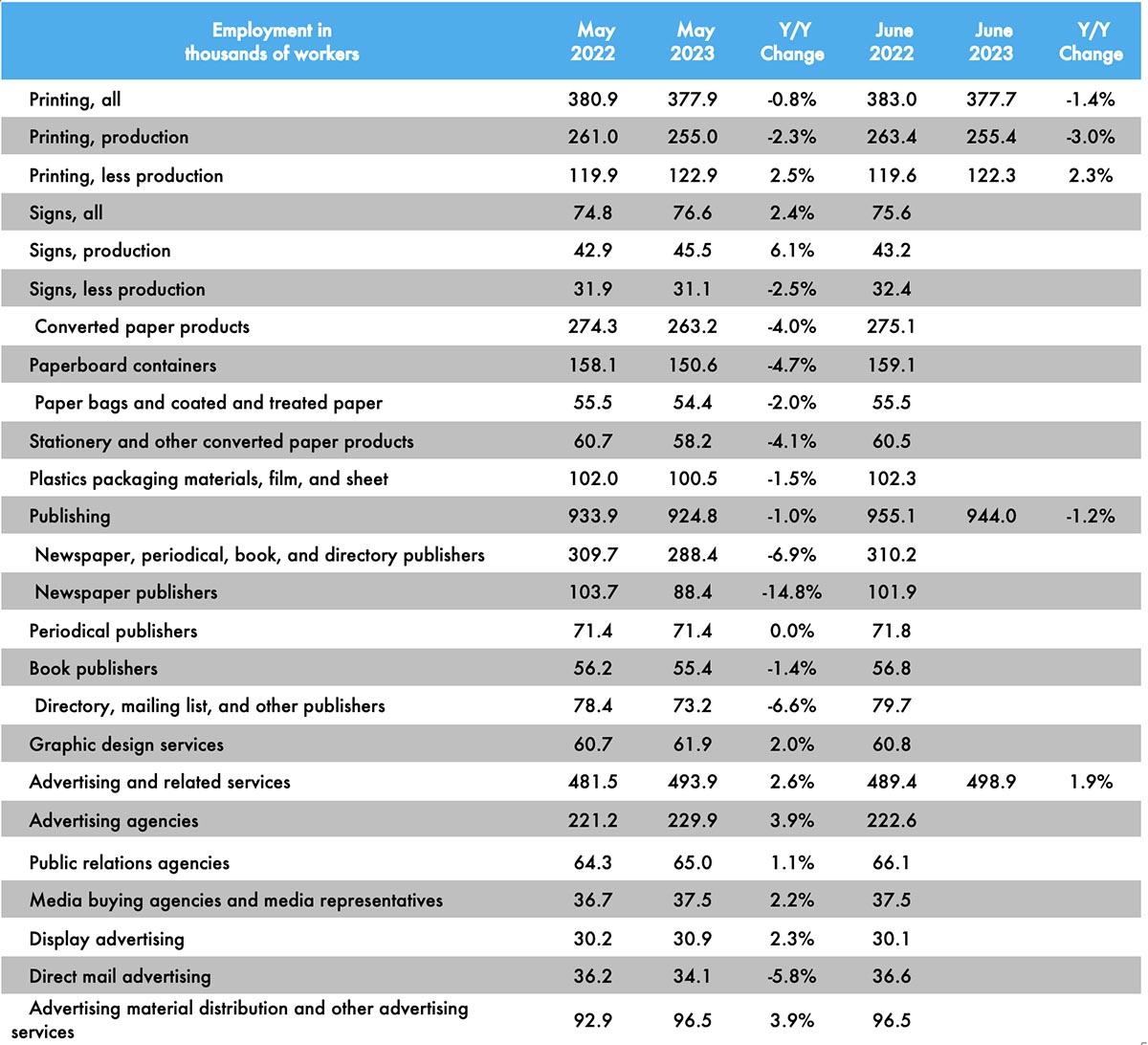

August Printing Production Employment Basically Flat

Published: September 8, 2023

Overall printing employment in August 2023 was down 0.2% from July. Production employment was down 0.3% while non-production employment was up 0.2%. Full Analysis

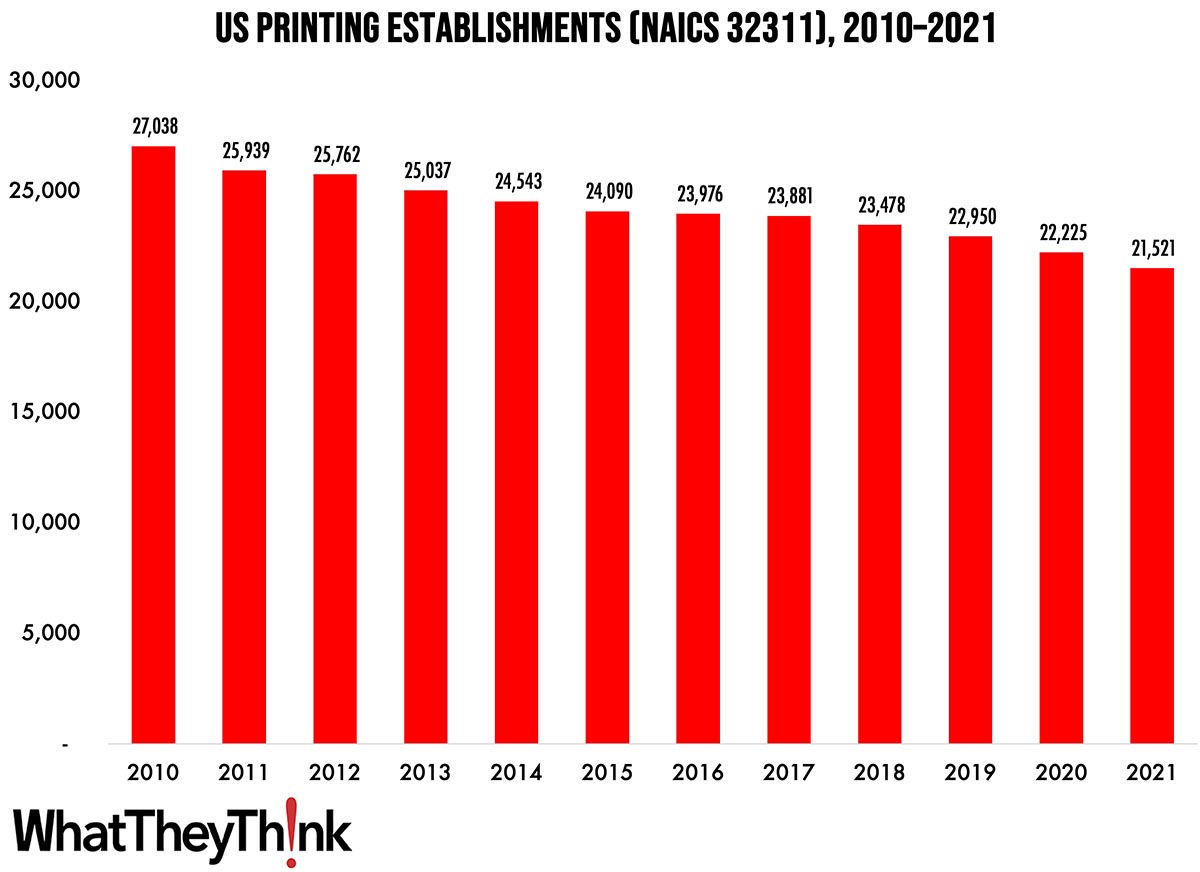

Printing Establishments—2010–2021

Published: September 1, 2023

According to the latest, just-released edition of County Business Patterns, in 2021 there were 21,521 establishments in NAICS 32311 (Printing). This represents a decline of 20% since 2010. In macro news, Q2 GDP revised downward. Full Analysis

June Shipments: Up, Up, and Away

Published: August 25, 2023

In a year that continues to surprise, June 2023 printing shipments came in at $7.38 billion, up from May’s $7.26 billion. Full Analysis

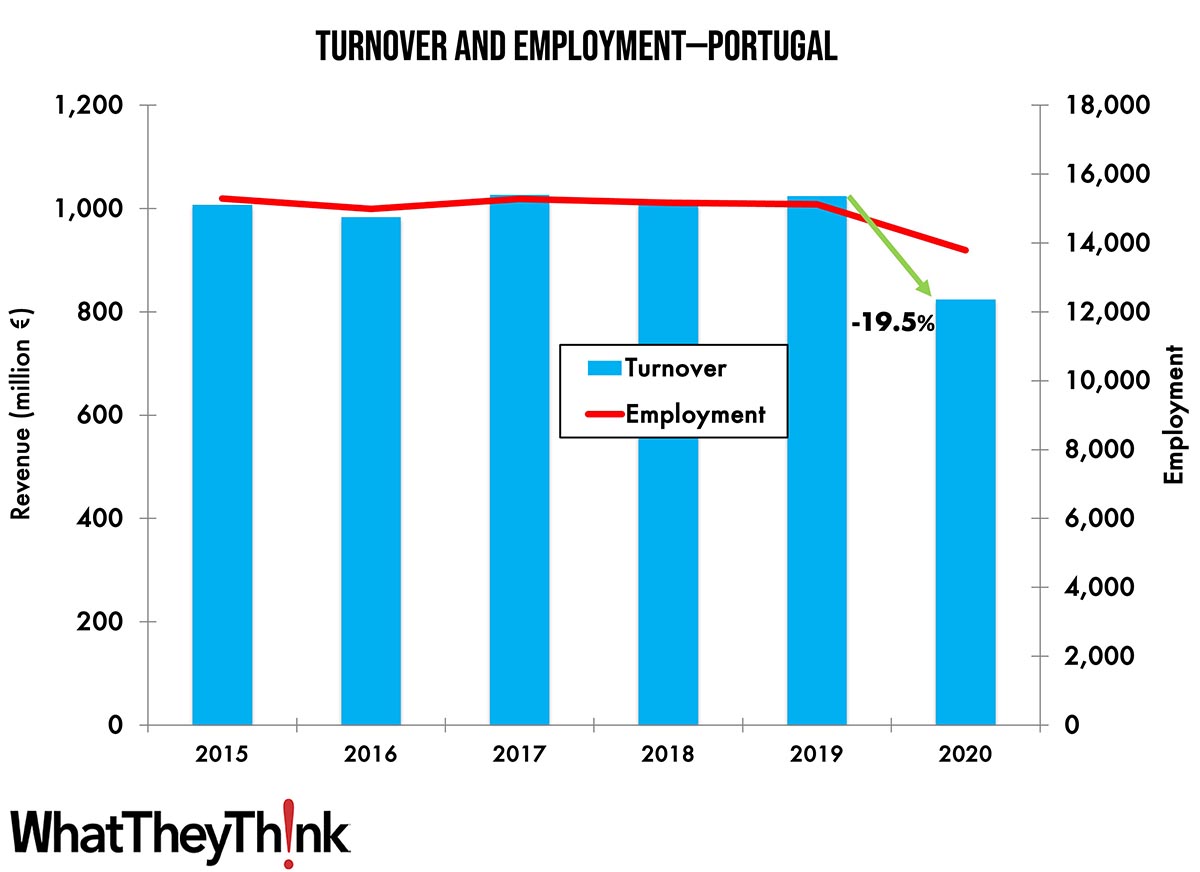

Turnover and Employment in Print in Europe—Portugal

Published: August 21, 2023

This bi-weekly series of articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Portugal, the 15th-largest printing industry by turnover in Europe. Full Analysis

Printing Establishments—2010–2021

Published: August 18, 2023

According to the latest, just-released edition of County Business Patterns, in 2021 there were 22,580 establishments in NAICS 323 (Printing and Related Support Activities). This represents a decline of 22% since 2010. In macro news, July retail sales came in above expectations. Full Analysis

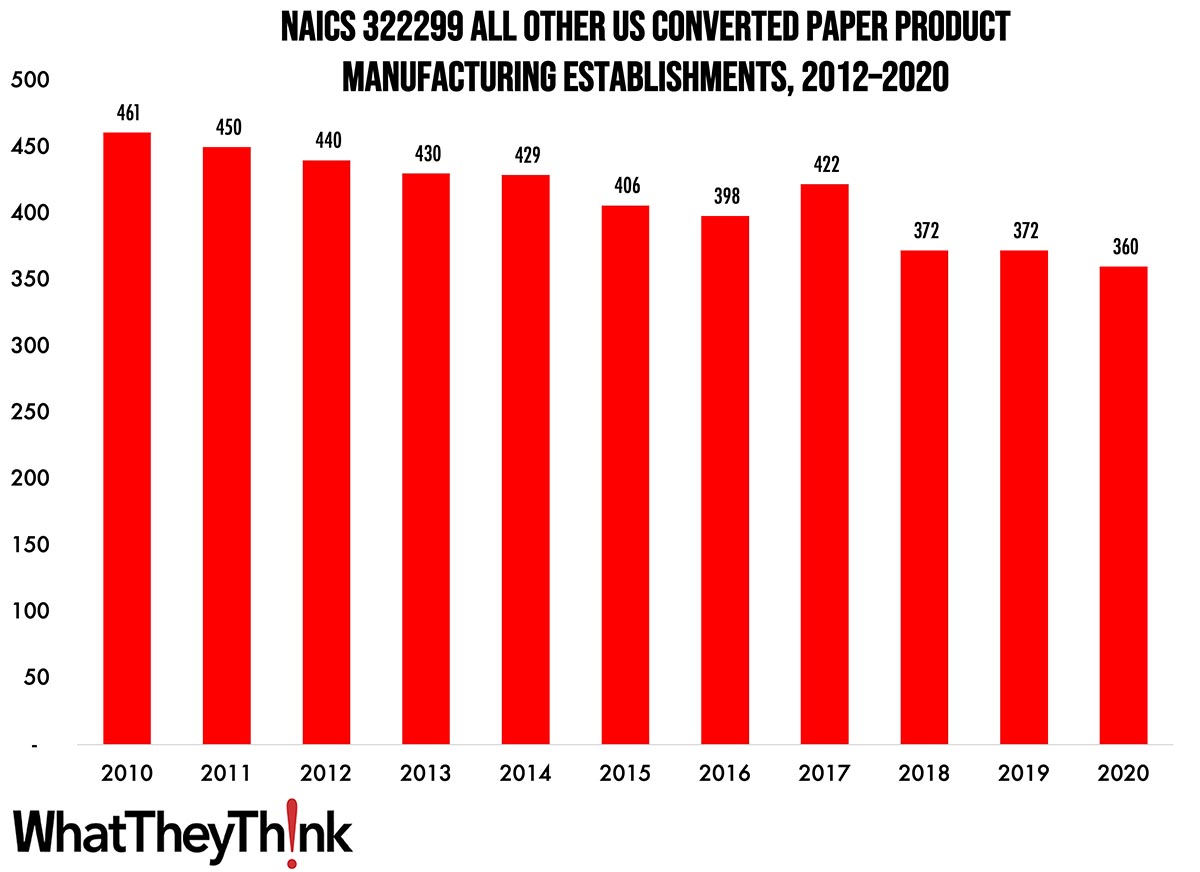

All Other Converted Paper Product Manufacturing Establishments—2010–2020

Published: August 4, 2023

According to County Business Patterns, in 2020 there were 360 establishments in NAICS 322299 (All Other Converted Paper Product Manufacturing). This category saw a net decrease in establishments of -22% since 2010. In macro news, Q2 GDP is up. Full Analysis

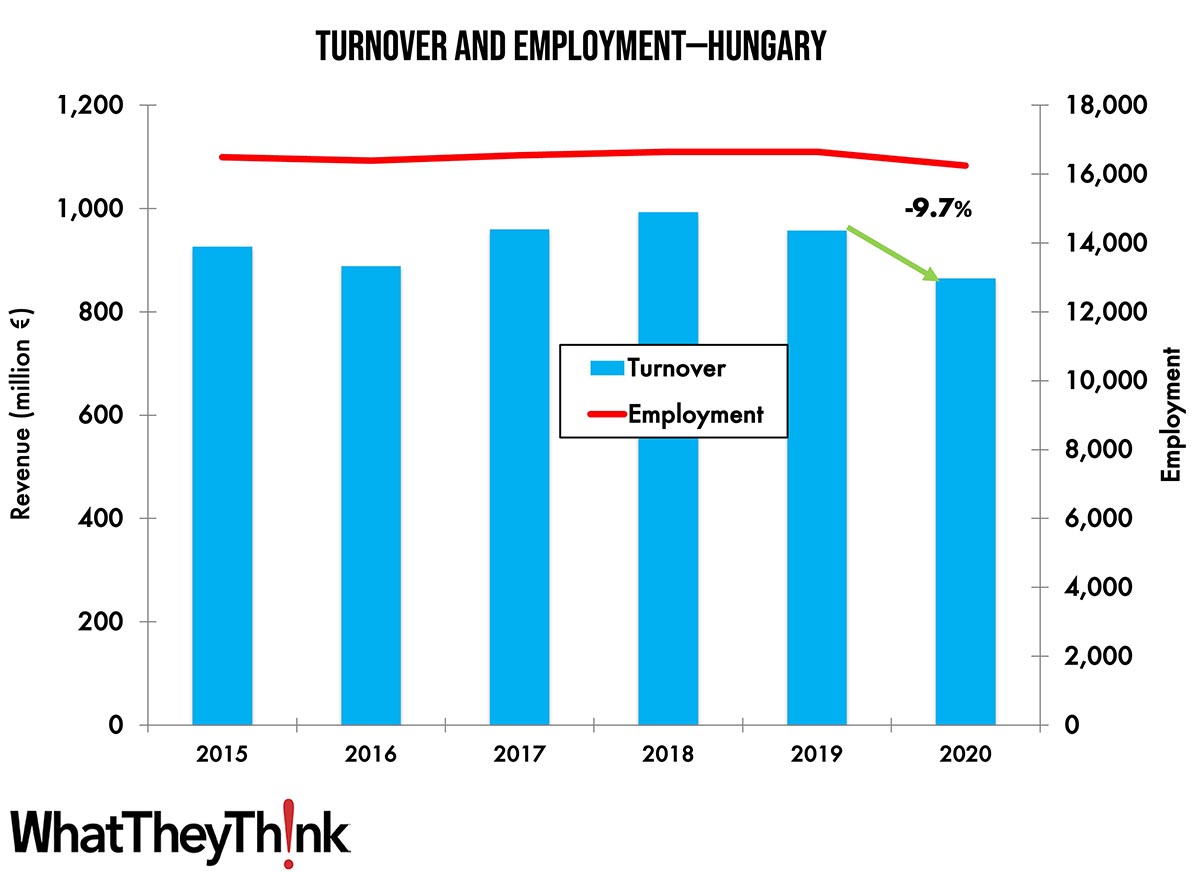

Turnover and Employment in Print in Europe—Hungary

Published: August 1, 2023

This series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Hungary, the 13th-largest printing industry by turnover in Europe and third largest in Central and Eastern Europe. Full Analysis

May Shipments Take an Unexpected—But Welcome—Turn

Published: July 28, 2023

May 2023 printing shipments came in at $7.26 billion, unexpectedly up from April’s $7.01 billion. Full Analysis

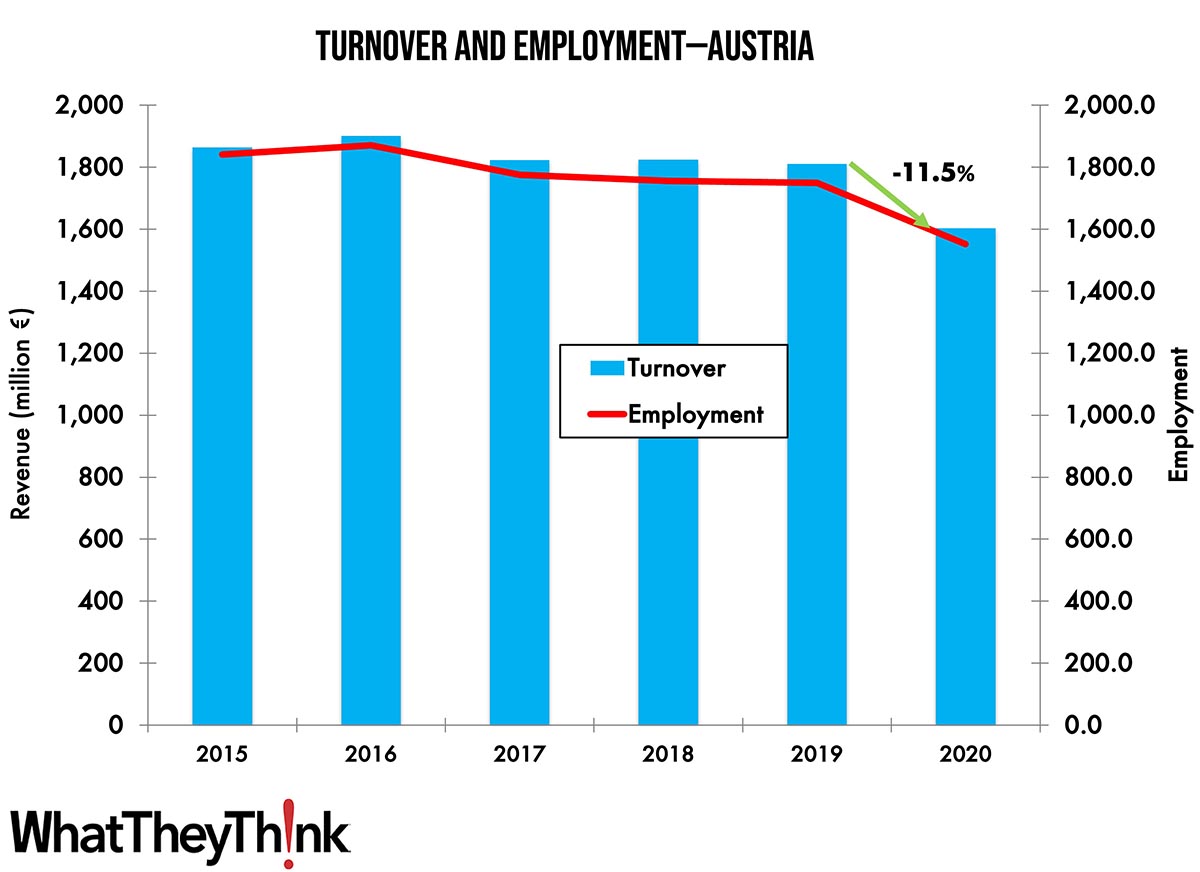

Turnover and Employment in Print in Europe—Austria

Published: July 25, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Austria, the tenth-largest printing industry by turnover in Europe. Full Analysis

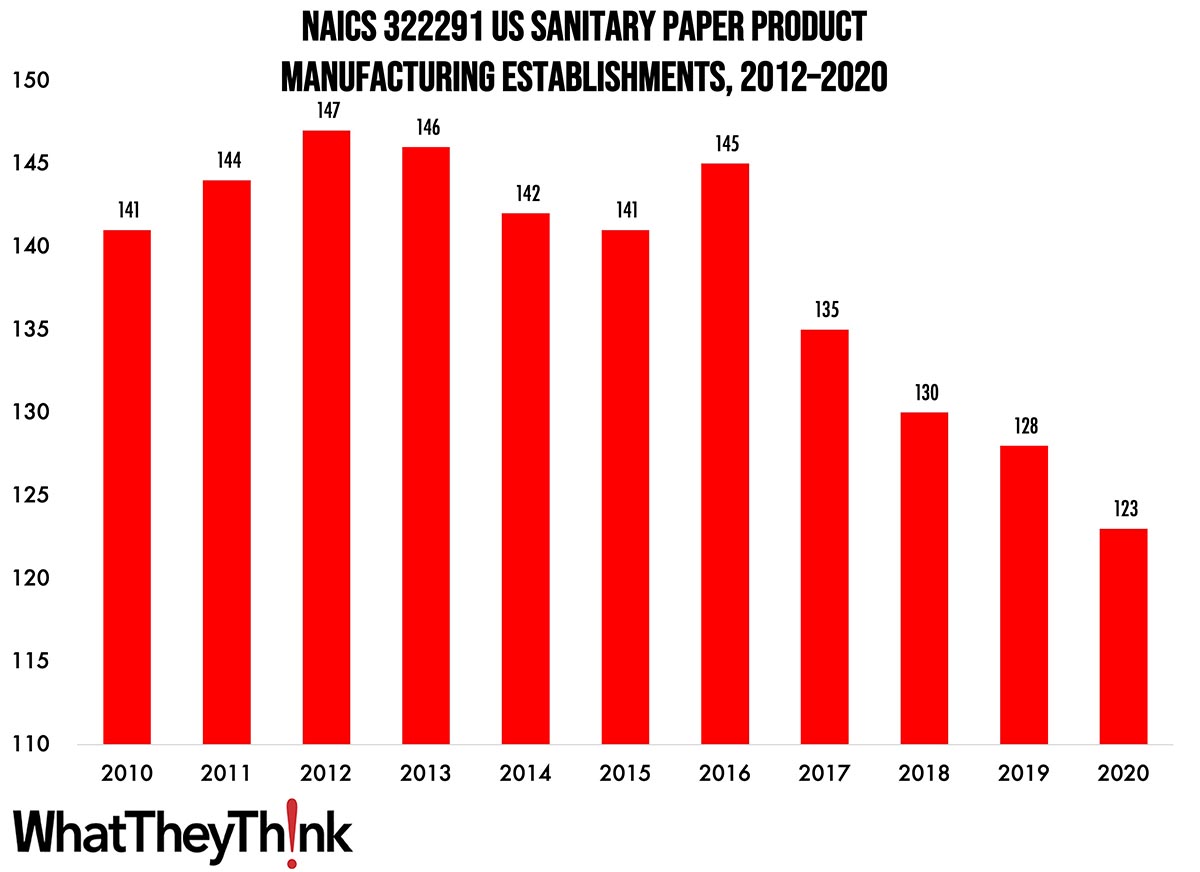

Sanitary Paper Product Manufacturing Establishments—2010–2020

Published: July 21, 2023

According to County Business Patterns, in 2020 there were 123 establishments in NAICS 322291 (Sanitary Paper Product Manufacturing). This category saw a net decrease in establishments of -13% since 2010. In macro news, new business applications continue to rise. Full Analysis

June Printing Production Employment Up Slightly, Non-Production Down

Published: July 14, 2023

Overall printing employment in June 2023 was down -0.2% from March. Production employment was up 0.4% while non-production employment was down -0.6%. Full Analysis

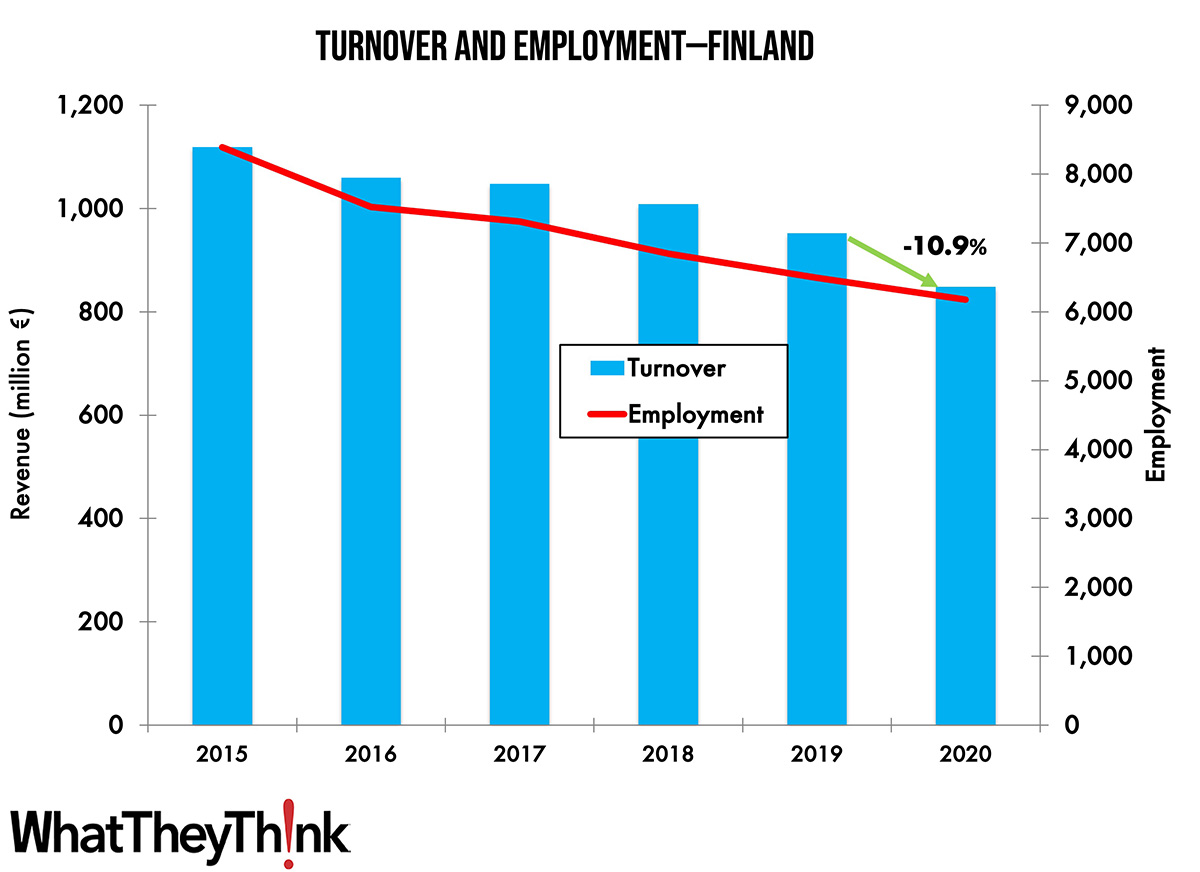

Turnover and Employment in Print in Europe—Finland

Published: July 11, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Finland, the 14th largest printing industry by turnover in Europe and the second largest in the Nordic region. Full Analysis

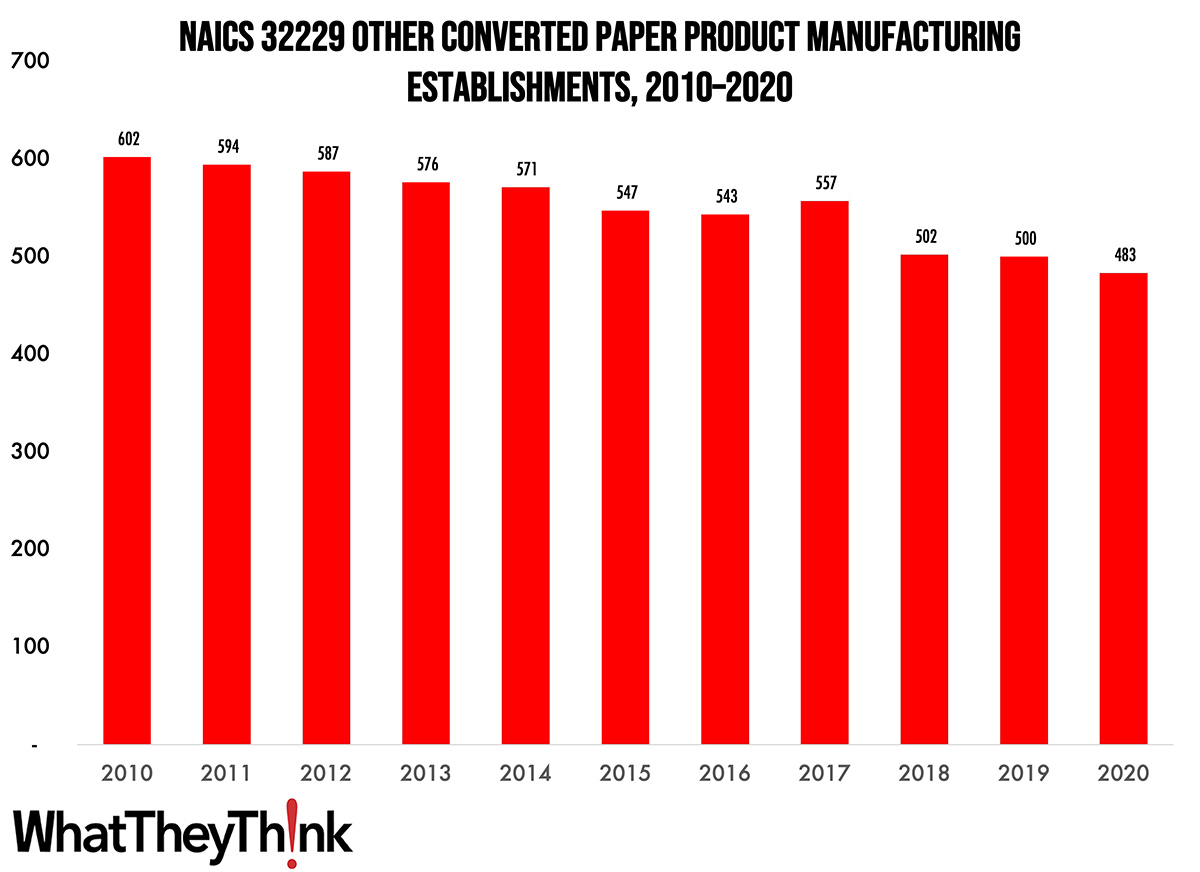

Other Converted Paper Product Manufacturing Establishments—2010–2020

Published: June 30, 2023

According to County Business Patterns, in 2020 there were 483 establishments in NAICS 32229 (Other Converted Paper Product Manufacturing). This category saw a net decrease in establishments of -20% since 2010. In macro news, BEA revises Q1 GDP up. Full Analysis

April Shipments Maintain Seasonality—Just as We Feared

Published: June 23, 2023

April 2023 printing shipments came in at $7.00 billion, down from March’s $7.58 billion and in line with annual seasonality—although it is a bit below the previous two Aprils. Full Analysis

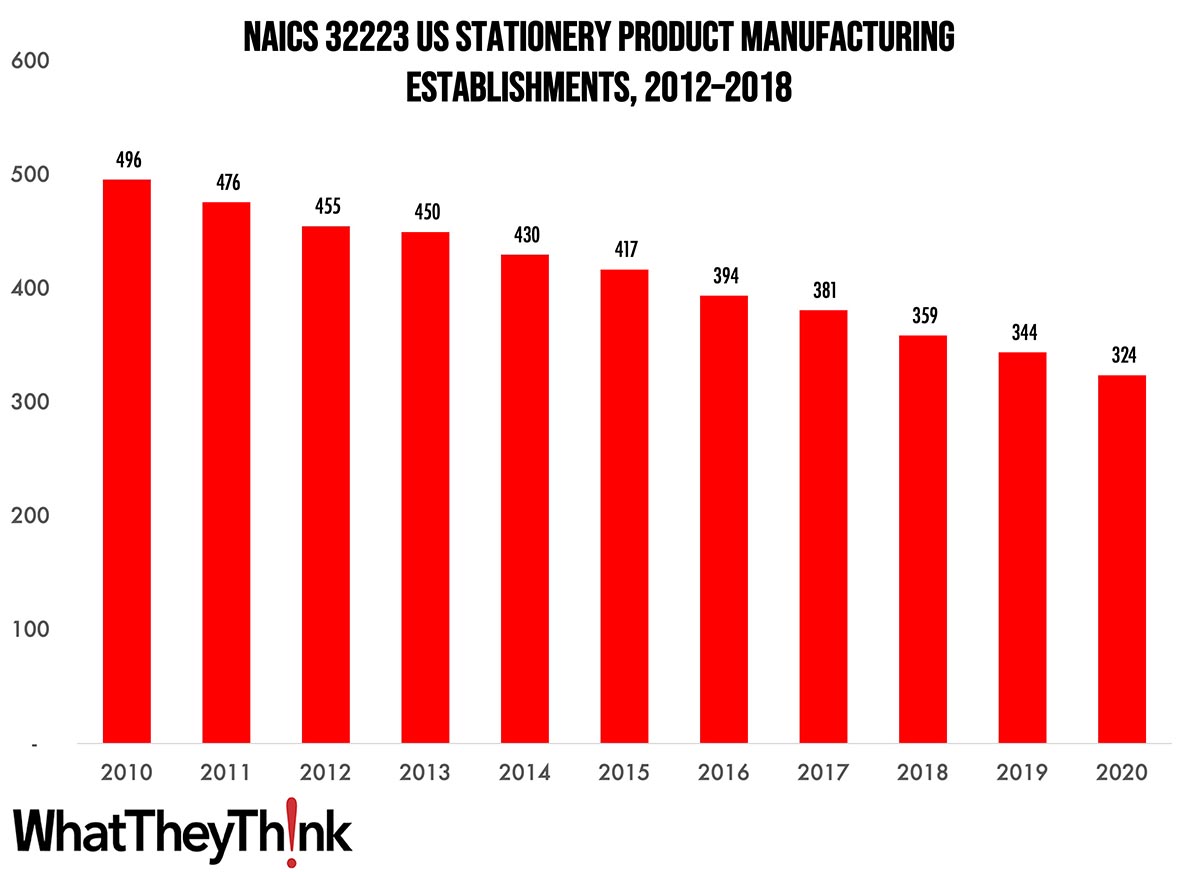

Stationery Product Manufacturing Establishments—2010–2020

Published: June 16, 2023

According to County Business Patterns, in 2020 there were 324 establishments in NAICS 32223 (Stationery Product Manufacturing). This category saw a net decrease in establishments of -35% since 2010. In macro news, the US birth rate increased insignificantly in 2022—the latest in a worrying demographic trend. Full Analysis

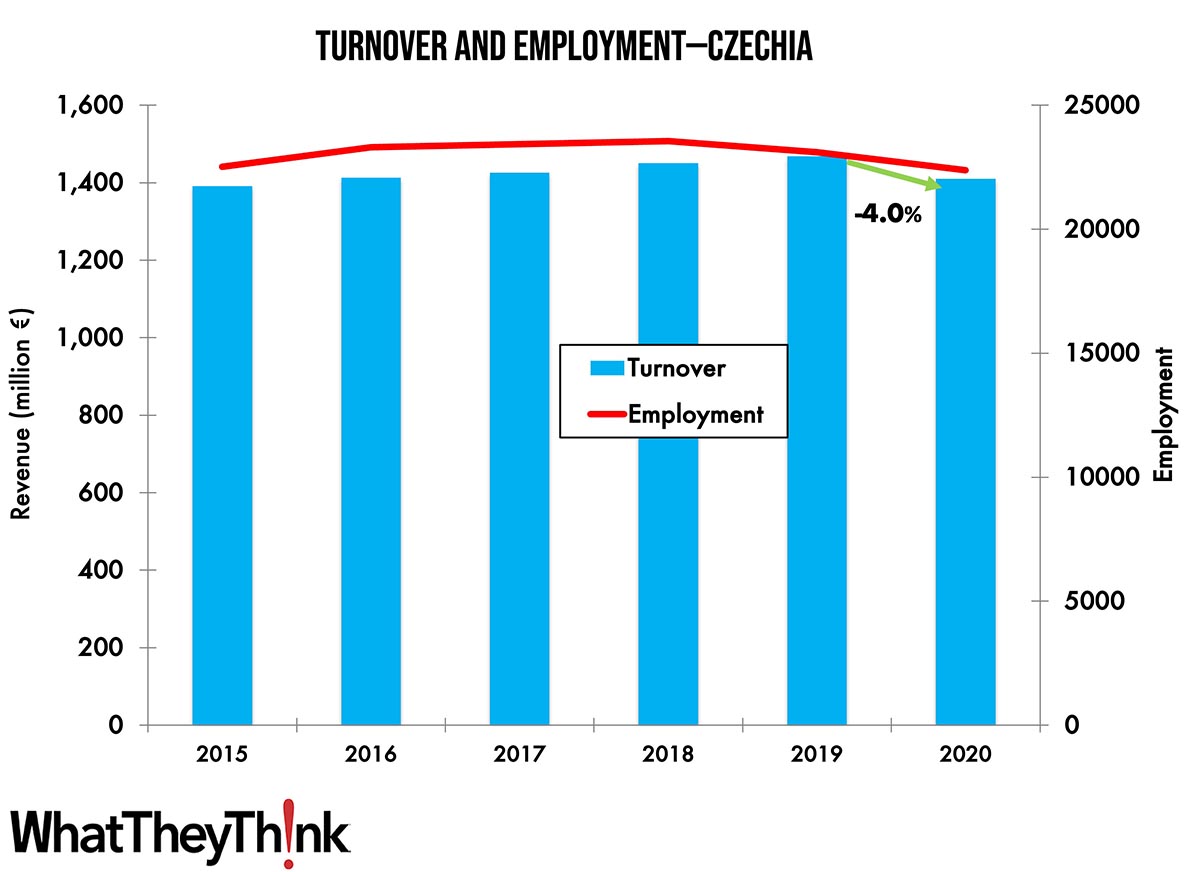

Turnover and Employment in Print in Europe—Czechia

Published: June 14, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Czechia (also called Czech Republic), the eleventh-largest printing industry by turnover in Europe and the second largest in Central and Eastern Europe. Full Analysis

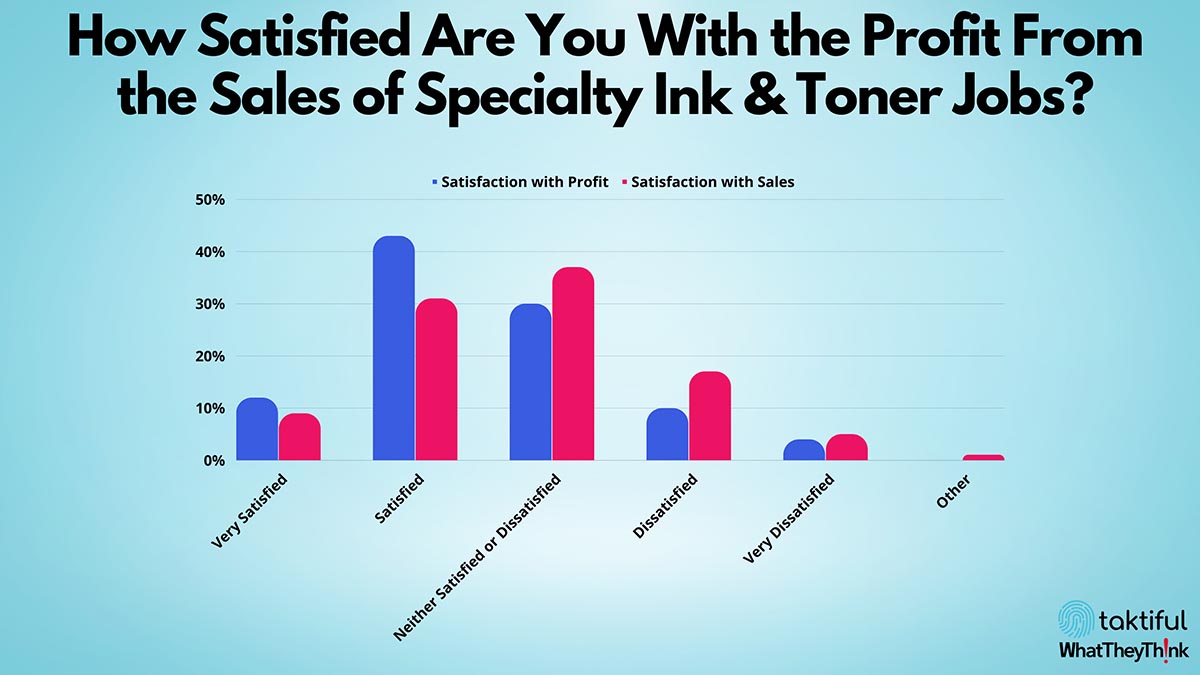

Printing Pulse: Embellishment Edition

Published: June 9, 2023

This edition of our Friday data series offers a preliminary “sneak peek” at the results of the Taktiful and WhatTheyThink 2023 Specialty Digital Ink and Toner Embellishment Study. This study takes a deep dive into how current users of digital ink and toner embellishment technologies are utilizing them, what the response from customers has been, how satisfied print providers have been with the sales and profitability of these jobs, where the challenges lie, and their general feelings about the future of digital ink and toner embellishment technologies. Full Analysis

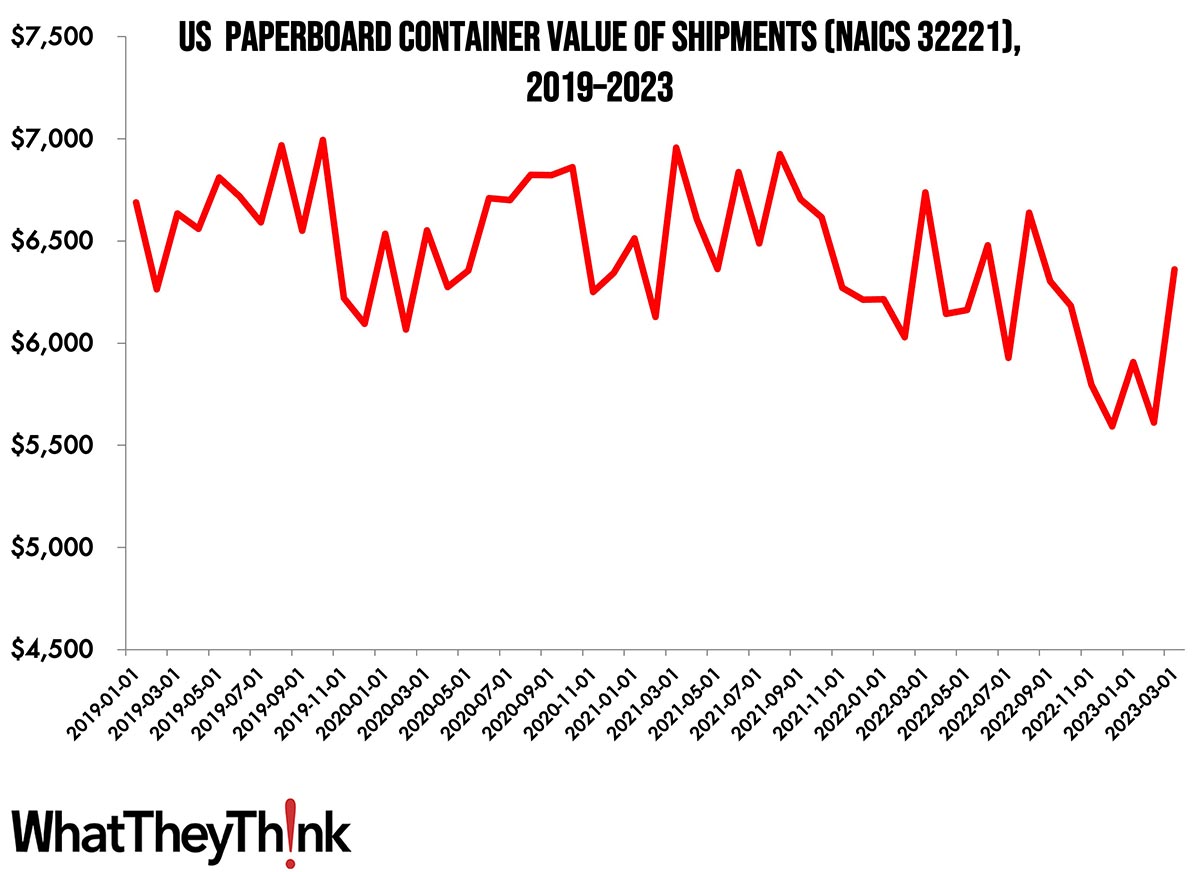

Paperboard Container Shipments Back up to Pandemic Levels

Published: June 2, 2023

In March 2023, the value of shipments of paperboard containers was $6.361 billion, the highest it has been since August 2022. Full Analysis

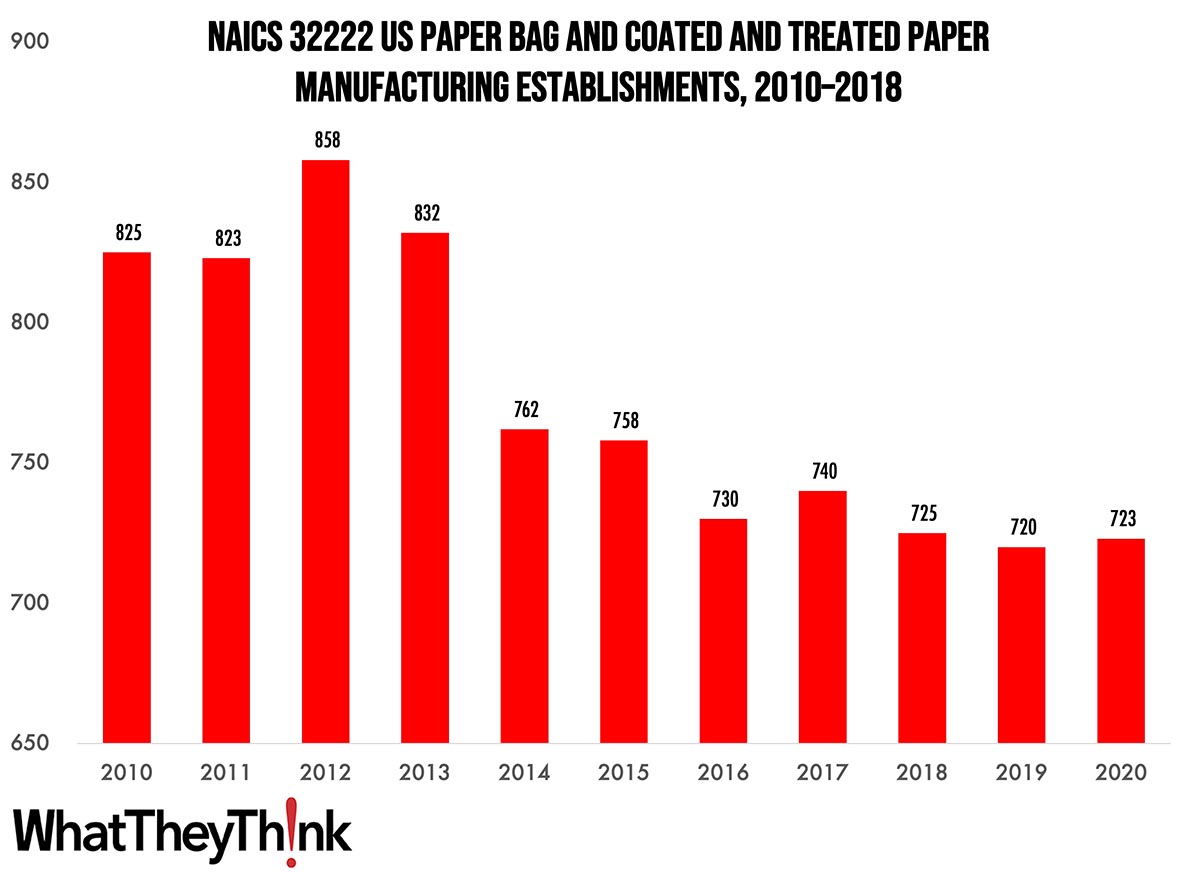

Paper Bag and Coated and Treated Paper Manufacturing Establishments—2010–2020

Published: May 26, 2023

According to County Business Patterns, in 2020 there were 723 establishments in NAICS 32222 (Paper Bag and Coated and Treated Paper Manufacturing). This category saw a net decrease in establishments of -12% since 2010. In macro news, the Architecture Billings Index suggests a recovery from the slowdown in the construction industry. Full Analysis

April Printing Production Employment Down Slightly, Non-Production Up

Published: May 19, 2023

Overall printing employment in April 2023 was down -0.2% from March. Production employment was down -0.8% while non-production employment was up 1.1%. Full Analysis

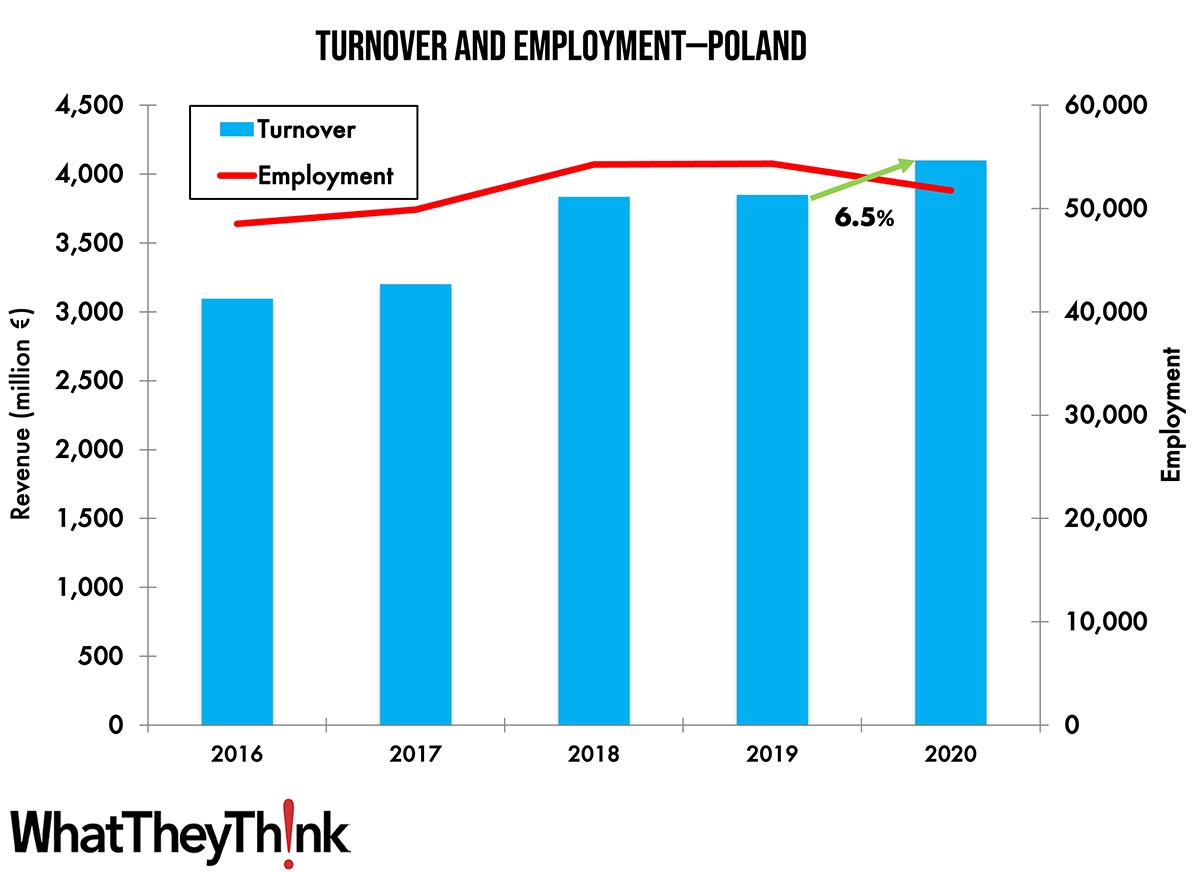

Turnover and Employment in Print in Europe—Poland

Published: May 15, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Poland, the sixth-largest printing industry by turnover in Europe and the largest in Central and Eastern Europe. Full Analysis

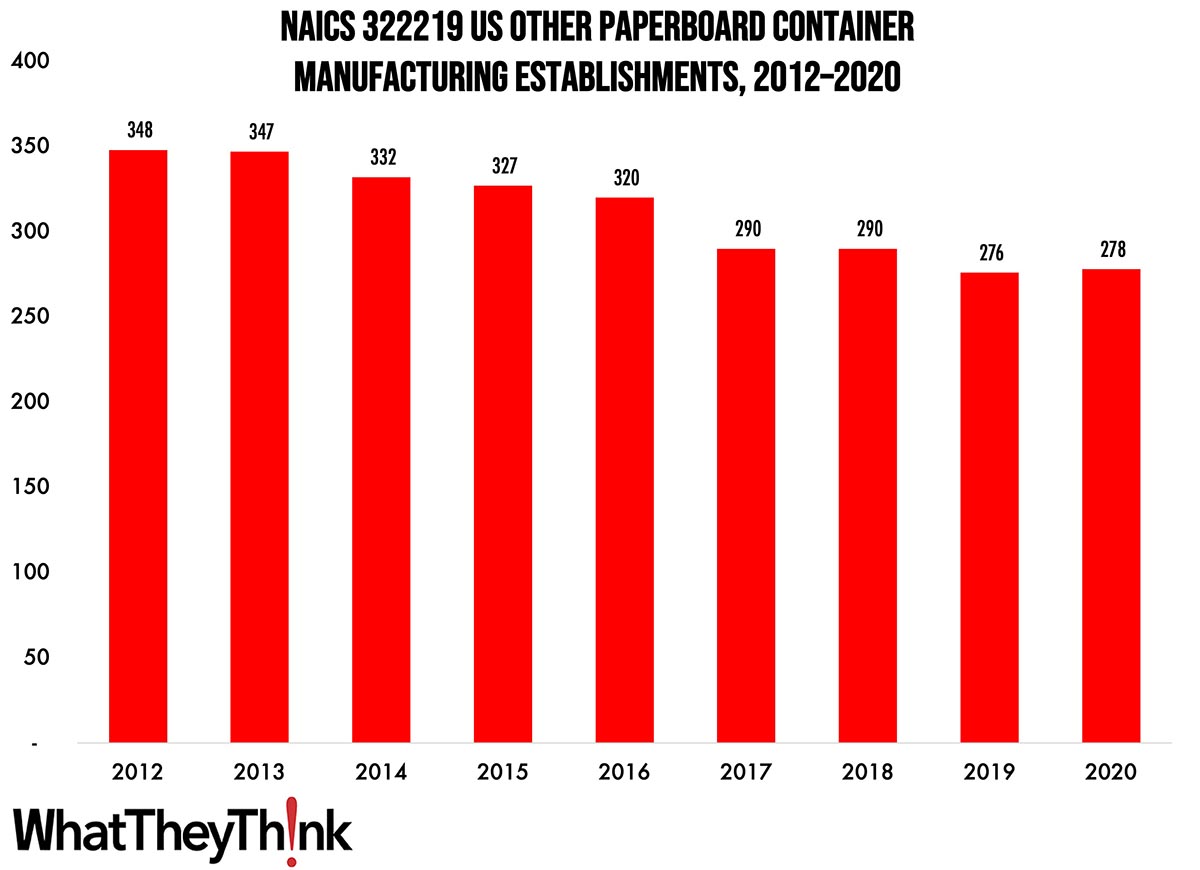

Other Paperboard Container Manufacturing Establishments—2010–2020

Published: May 12, 2023

According to County Business Patterns, in 2020 there were 278 establishments in NAICS 322219 (Other Paperboard Container Manufacturing). This category saw a net decrease in establishments of -20% since 2010. In macro news, inflation is slowing but still high. Full Analysis

March Shipments Maintain Seasonality—Make of That What You Will

Published: May 5, 2023

March 2023 printing shipments came in at $7.18 billion, up from February’s $6.46 billion and in line with annual seasonality—even if it is below the previous two Marches. Full Analysis

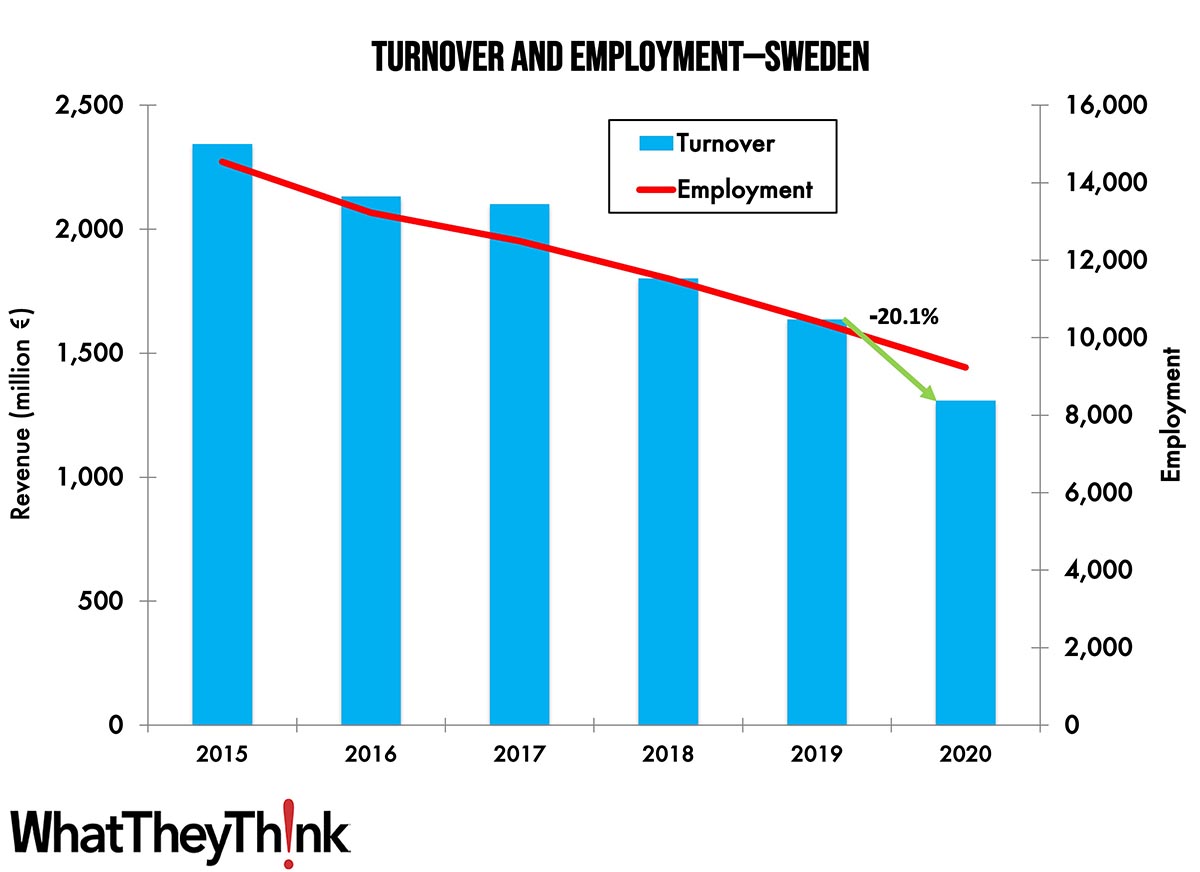

Turnover and Employment in Print in Europe—Sweden

Published: May 1, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Sweden, the 12th-largest printing industry by turnover in Europe. Full Analysis

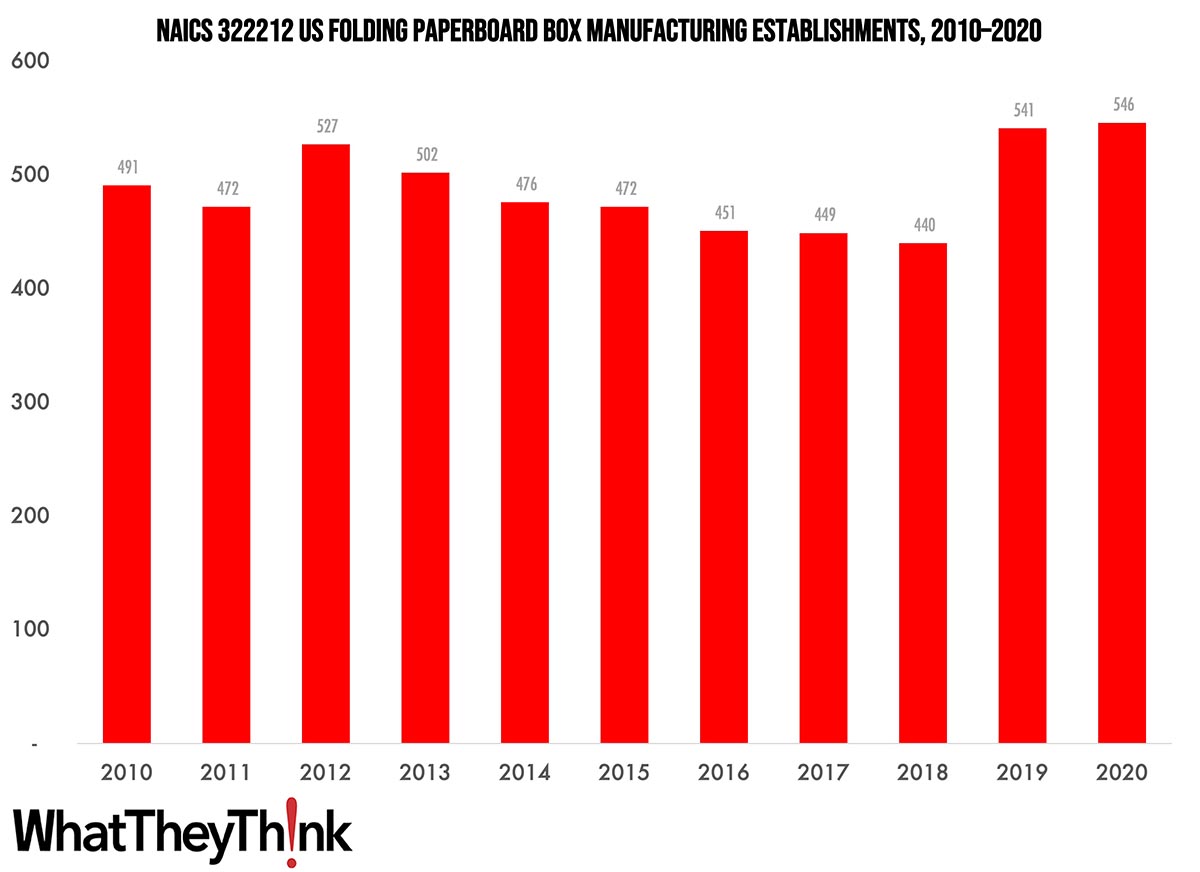

Folding Paperboard Box Manufacturing Establishments—2010–2020

Published: April 28, 2023

According to County Business Patterns, in 2020 there were 546 establishments in NAICS 322212 (Folded Paperboard Box Manufacturing). This category saw a net increase in establishments of 11% since 2010. In macro news, Q1 2023 GDP shows third straight quarter of growth. Full Analysis

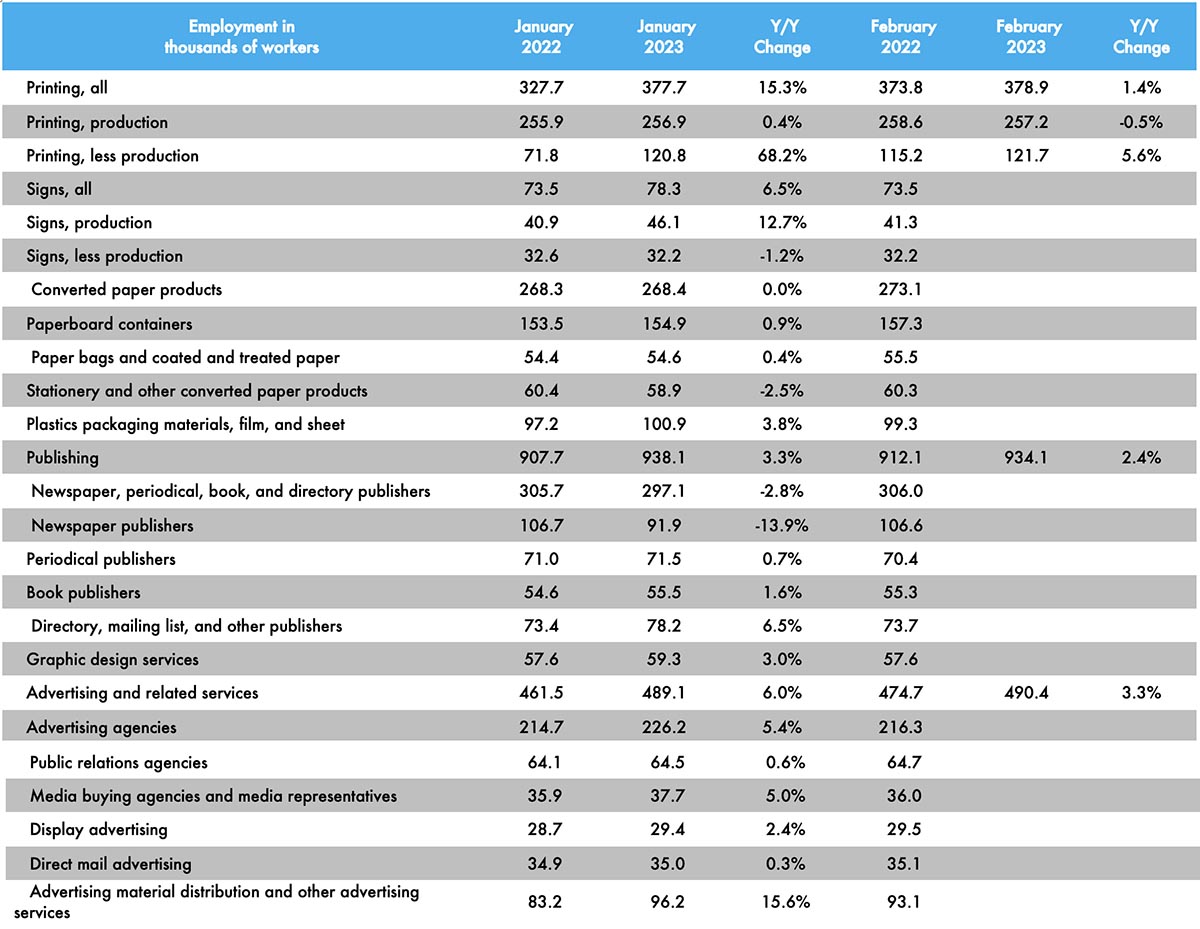

February Printing Employment Essentially Flat

Published: April 21, 2023

Overall printing employment in February 2023 was up 0.3% from January. Production employment was up 0.1% while non-production employment was up 0.7%. Full Analysis

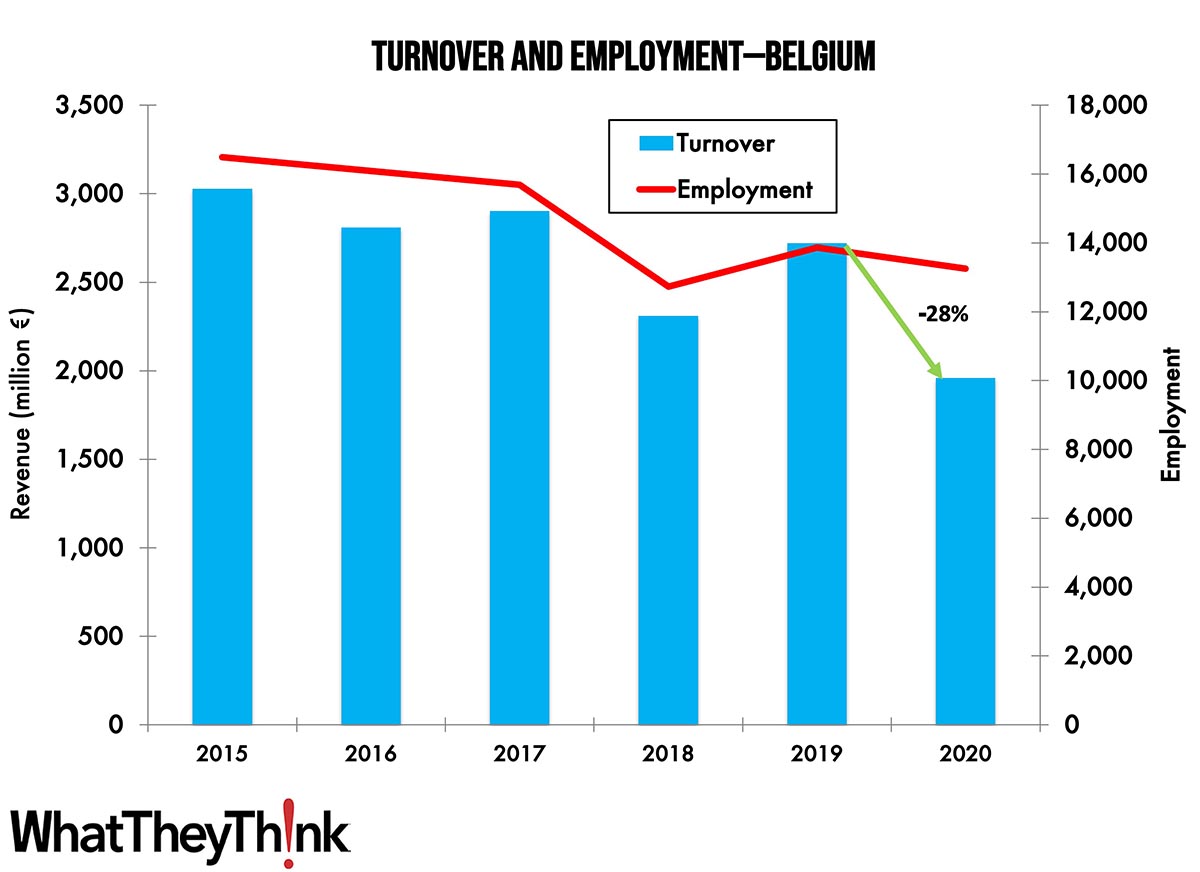

Turnover and Employment in Print in Europe—Belgium

Published: April 17, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Belgium, the ninth-largest printing industry by turnover in Europe. Full Analysis

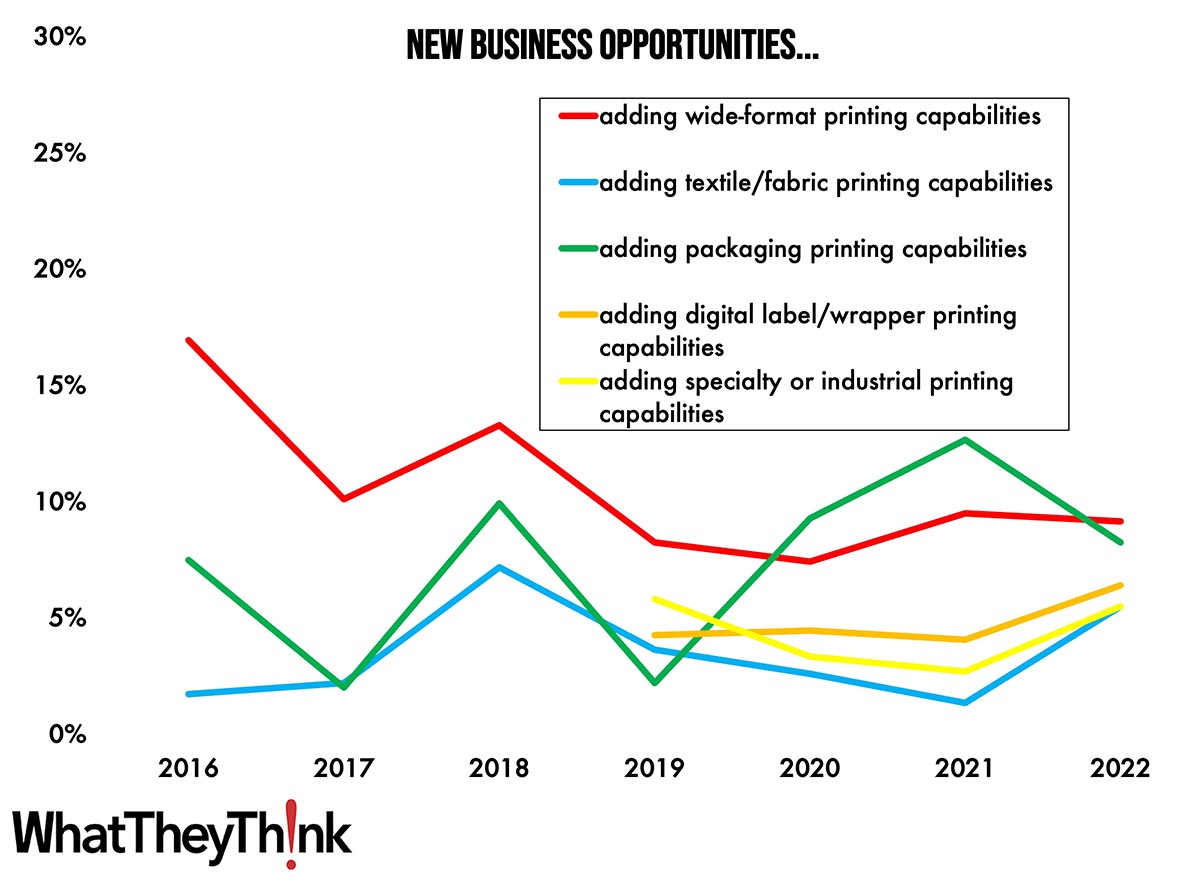

Tales from the Database: Beyond Commercial

Published: April 14, 2023

The latest installment in our “Tales from the Database” series looks at historical opportunities and investments related to adding not only things like wide-format printing and textile printing capabilities, but also packaging as well as other types of specialty printing. Full Analysis

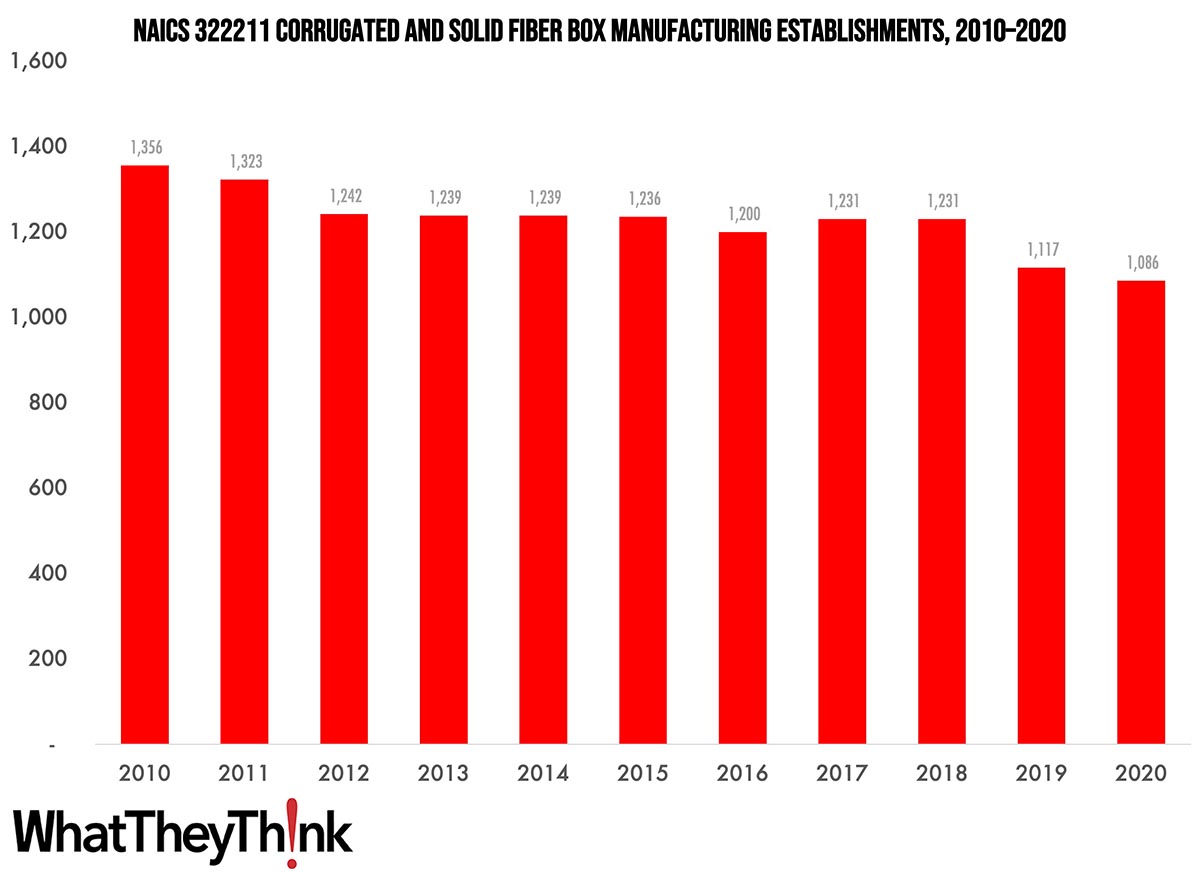

Corrugated and Solid Fiber Box Manufacturing Establishments—2010–2020

Published: March 31, 2023

According to County Business Patterns, in 2020 there were 1,086 establishments in NAICS 322211 (Corrugated and Solid Fiber Box Manufacturing). This category saw a net decrease of 20% since 2010. In macro news, Q4 GDP was revised down. Full Analysis

Kicking Off 2023: Best Shipments Since 2020

Published: March 24, 2023

January 2023 printing shipments came in at $6.67 billion, the best start to a year since 2020. Full Analysis

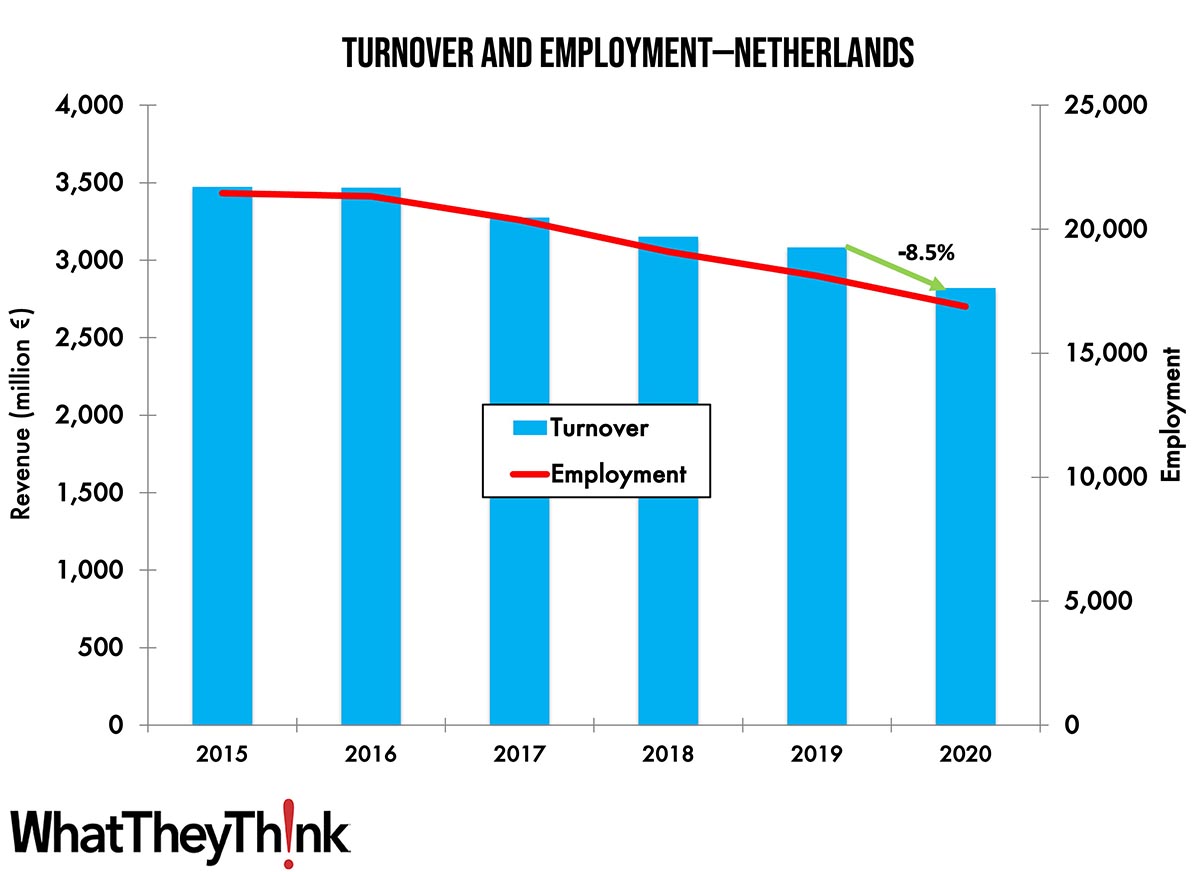

Turnover and Employment in Print in Europe—The Netherlands

Published: March 21, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at the Netherlands, the seventh largest printing industry by turnover in Europe. Full Analysis

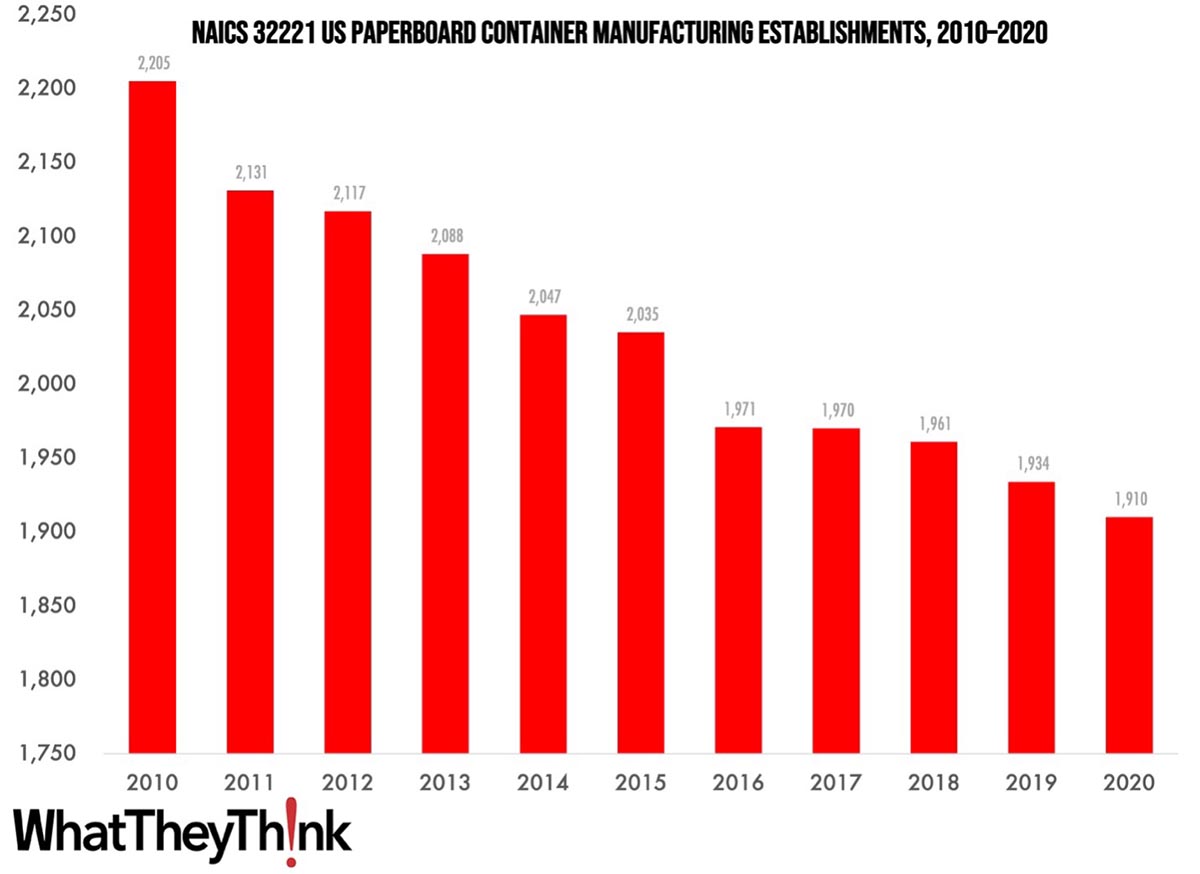

Paperboard Container Manufacturing Establishments—2010–2020

Published: March 17, 2023

According to County Business Patterns, in 2020 there were 1,910 establishments in NAICS 32221 (Paperboard Container Manufacturing). This category saw a net decrease of 13% since 2010. In macro news,inflation is sort of moving sideways. Full Analysis

January Production Employment Down

Published: March 10, 2023

Overall printing employment in January 2023 was down -1.7% from December, due entirely to a -4.2% drop in production employment, as non-production employment was up +4.1%. Full Analysis

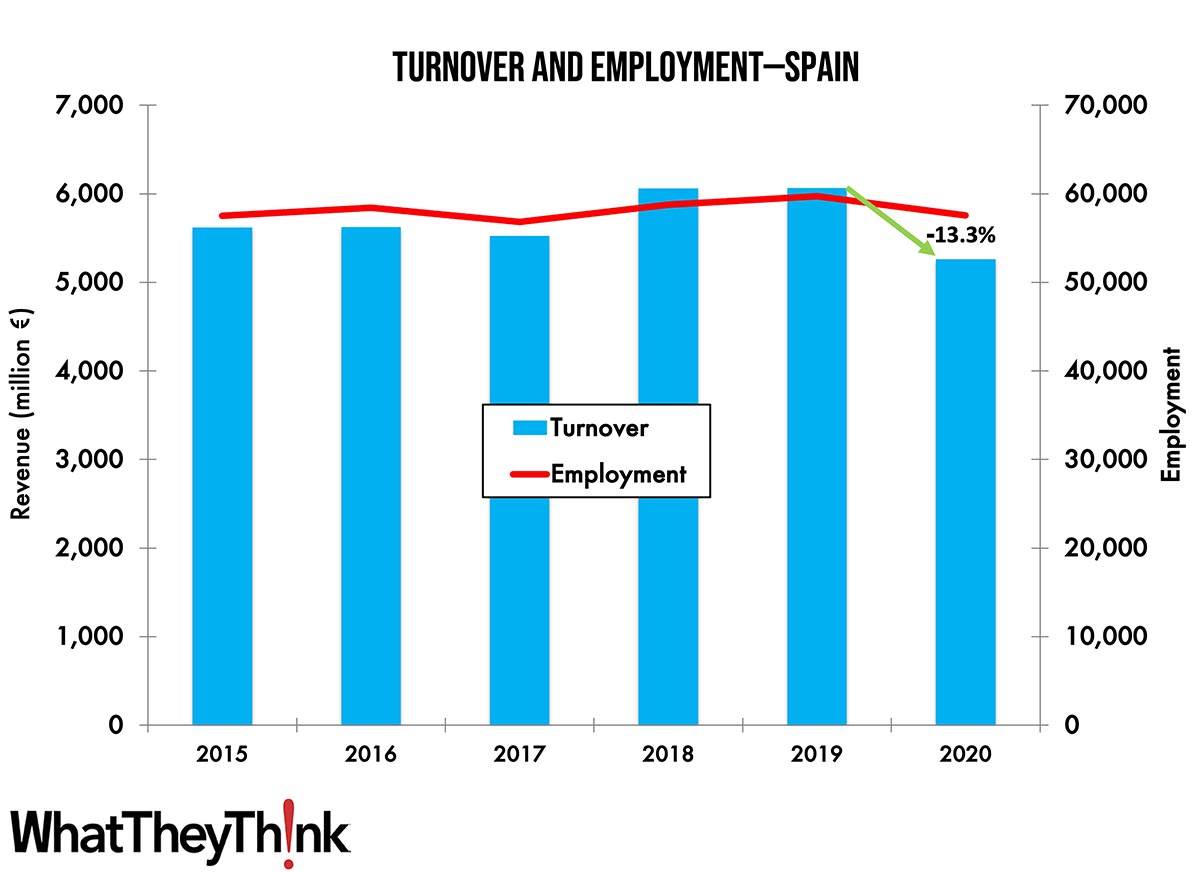

Print Turnover and Employment in Europe—Spain

Published: March 6, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at Spain, the fifth largest printing industry by turnover in Europe. Full Analysis

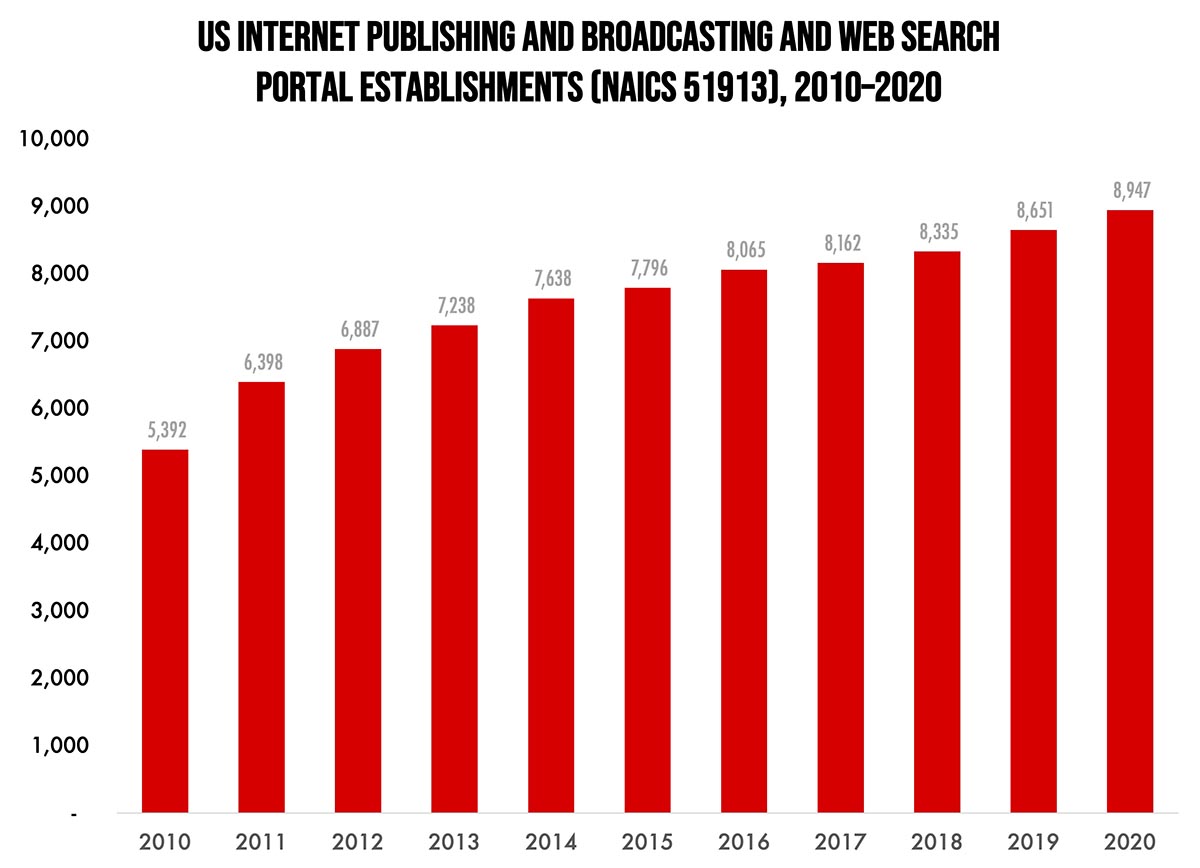

Internet Publishing and Broadcasting and Web Search Portal Establishments—2010–2020

Published: March 3, 2023

According to County Business Patterns, in 2020 there were 8,947 establishments in NAICS 51913 (Internet Publishing and Broadcasting and Web Search Portals). This category saw a net increase of 66% since 2010. In macro news, early forecasts of Q1 GDP are running slightly bearish to slightly bullish. Full Analysis

Hooray! 2022 Shipments Outpaced 2021

Published: February 24, 2023

December 2022 printing shipments came in at $6.97 billion, down from November’s $7.10 billion. But January-to-December shipments for 2022 came in at $83.47 billion, an improvement over 2021’s $82.05 billion. Full Analysis

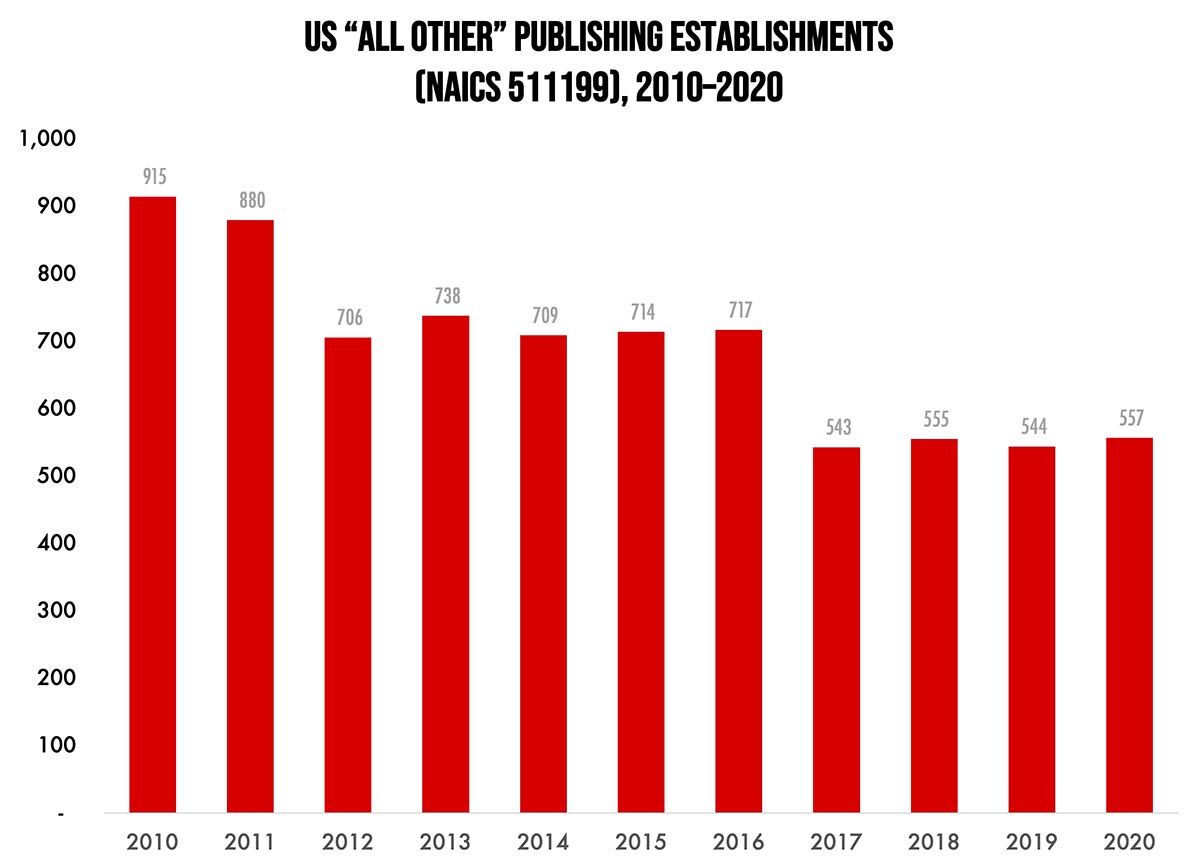

Assorted Publishing Establishments—2010–2020

Published: February 17, 2023

According to County Business Patterns, in 2020 there were 557 establishments in NAICS 511199 (All Other Publishing). This category saw a net decrease of 39% since 2010, , although we’re not talking about a tremendous number of establishments. In macro news, inflation appears to have peaked. Full Analysis

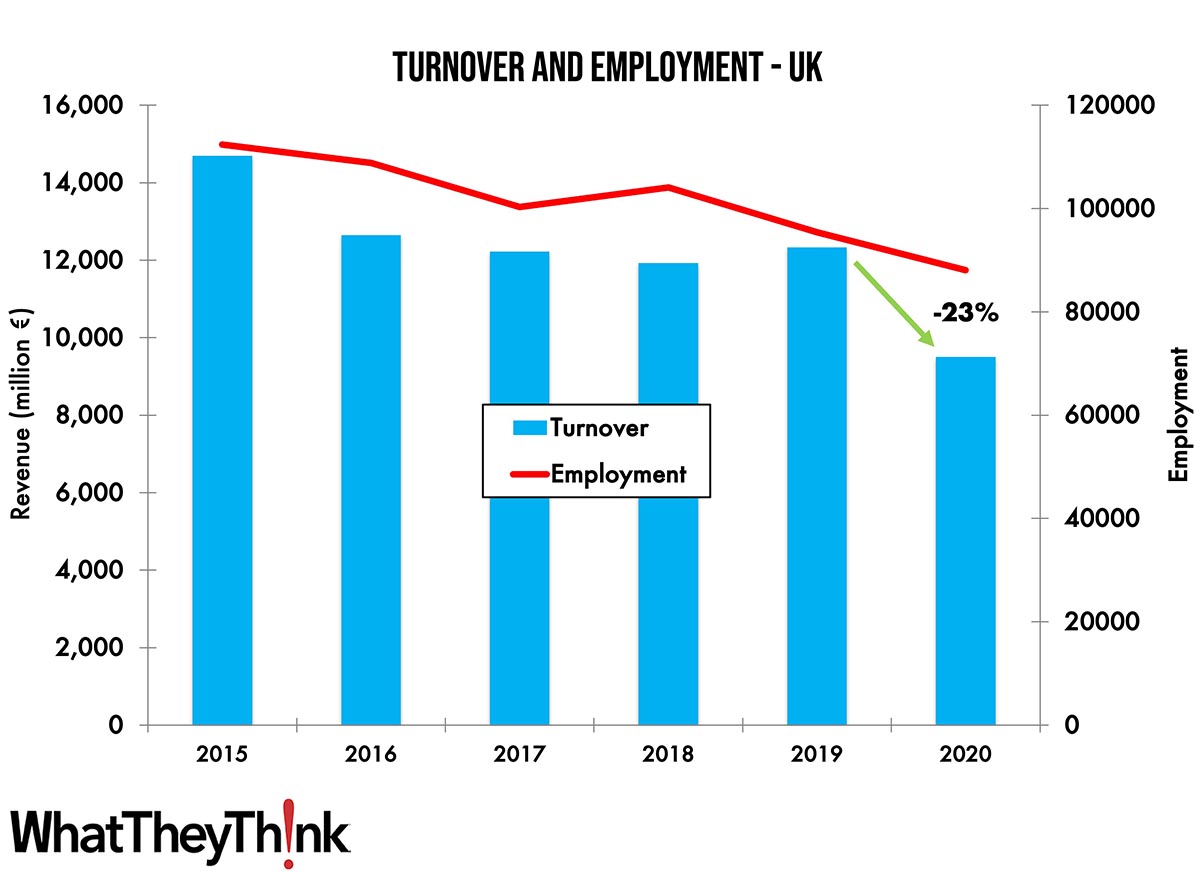

Turnover and Employment in Print in Europe—UK

Published: February 14, 2023

This bi-weekly series of short articles aims at shedding a spotlight on the size of the printing industry in Europe per country and how revenues and employment developed in 2020, when the pandemic impacted businesses. This time we look at the UK, the second-largest printing industry by turnover in Europe. Full Analysis

Tales from the Database: Software

Published: February 10, 2023

In our January/February 2023 print edition, we are launching a new series called “Tales from the Database,” drawing on six years’ worth of Print Business Outlook surveys. In every survey, we ask a broad cross-section of print businesses about business conditions, business challenges, new business opportunities, and planned investments. January/February is the software issue, so we rounded up a few software-related challenges, opportunities, and investments to see what the historical data can tell us. Full Analysis

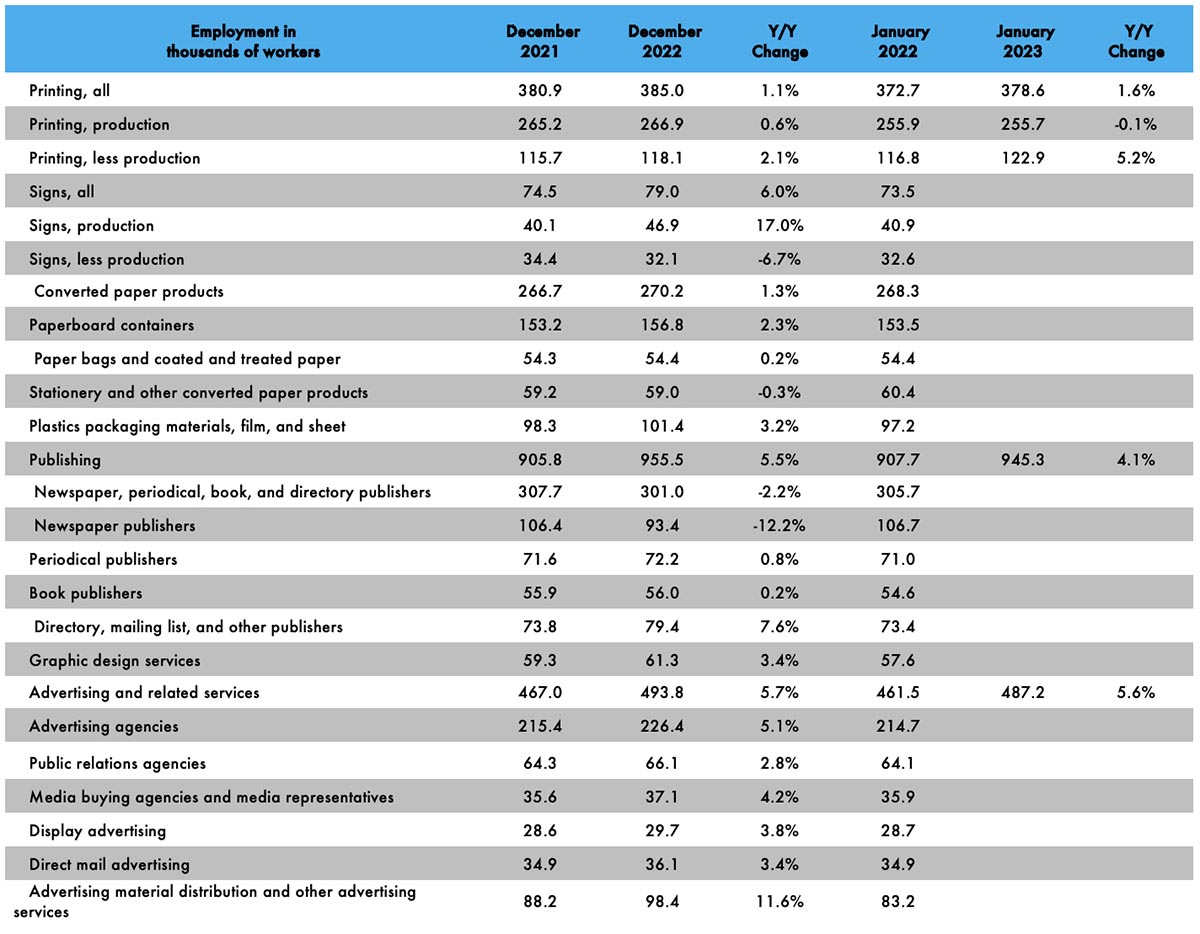

Graphic Arts Employment Flat or Declining in December

Published: February 3, 2023

Overall printing employment was essentially flat in December 2022, being down -0.1% from November, and essentially unchanged from December 2021. Production employment was up +0.4% while non-production employment was down -1.1% from November. Full Analysis

![]()

- KYOCERA NIXKA INKJET SYSTEMS (KNIS) INTRODUCES BELHARRA, THE NEW WAVE OF PHOTO PRINTERS

- New RISO Printing Unit Offers Easy Integration for Package Printing

- March 2024 Inkjet Installation Roundup

- Inkjet Integrator Profiles: Integrity Industrial Inkjet

- Revisiting the Samba printhead

- 2024 Inkjet Shopping Guide for Folding Carton Presses

- The Future of AI In Packaging

- Inkjet Integrator Profiles: DJM

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.