Data Analysis

Two Indicators: Retail Sales and Industrial Production

Published: September 10, 2021

This week’s Friday data dump looks at two macroeconomic indicators that will give us some sense of how we are bouncing back from the pandemic—Retail sales and the Industrial Production Index. Full Analysis

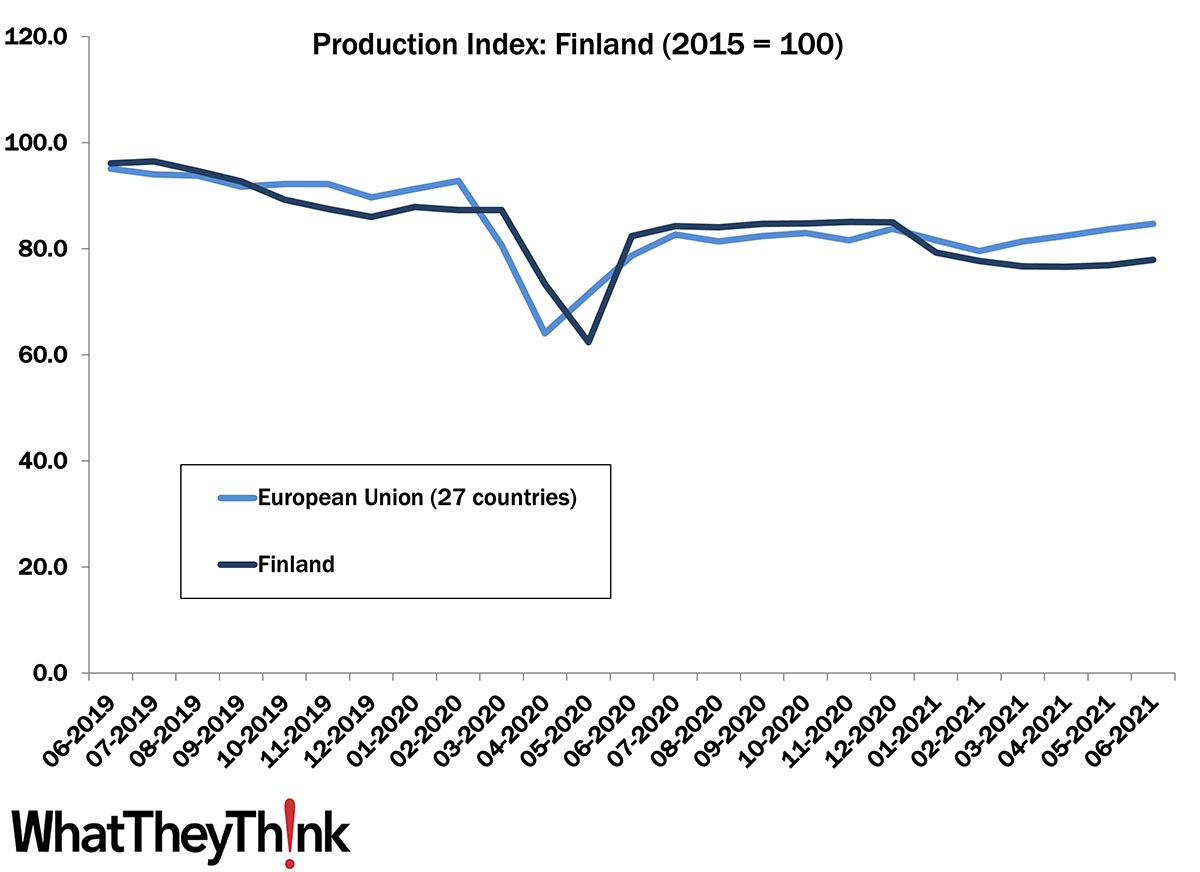

European Print Industry Snapshot: Finland

Published: September 7, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Finland. Full Analysis

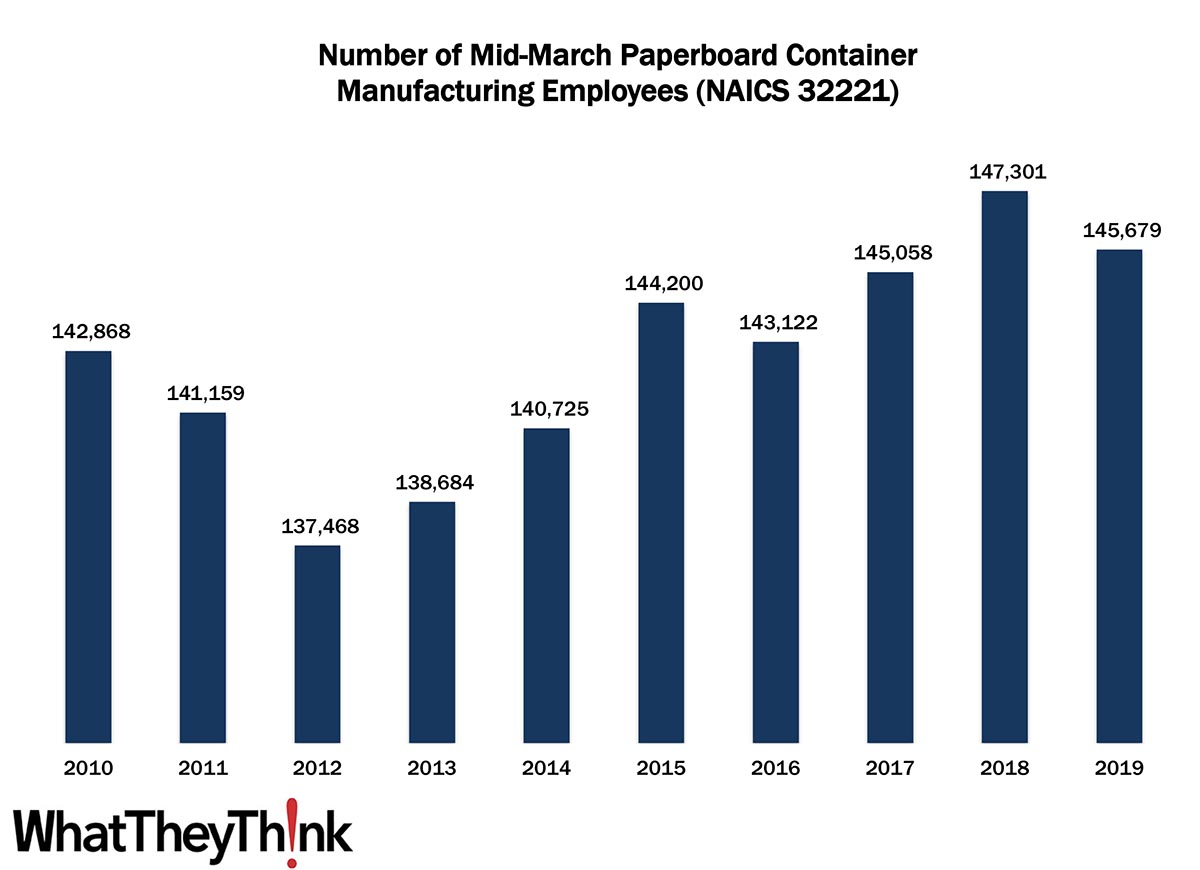

Paperboard Container Manufacturing Employment—2010–2019

Published: September 3, 2021

According to County Business Patterns, in 2010, there were 142,868 employees in NAICS 32221 (Paperboard Container Manufacturing establishments). Employment in this category dropped abruptly in 2011 and 2012, then continued to rise over the course of the decade, peaking in 2018 at 147,301 before dropping a bit in 2019. In macro news, office and mall vacancy rates are at historic highs, the pandemic having accelerated trends that had been well underway beforehand. Full Analysis

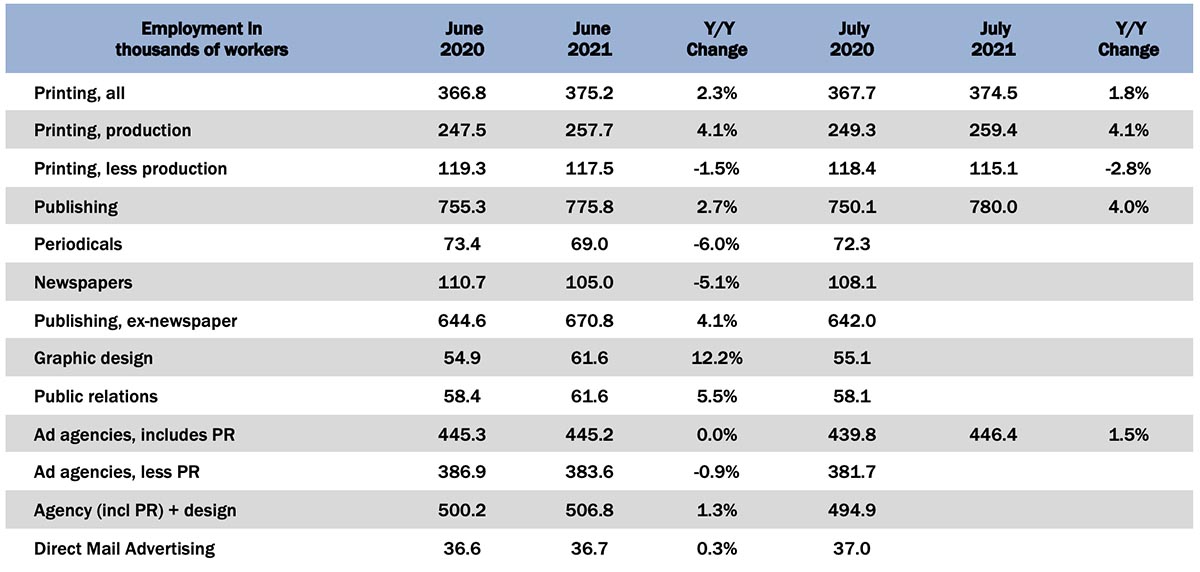

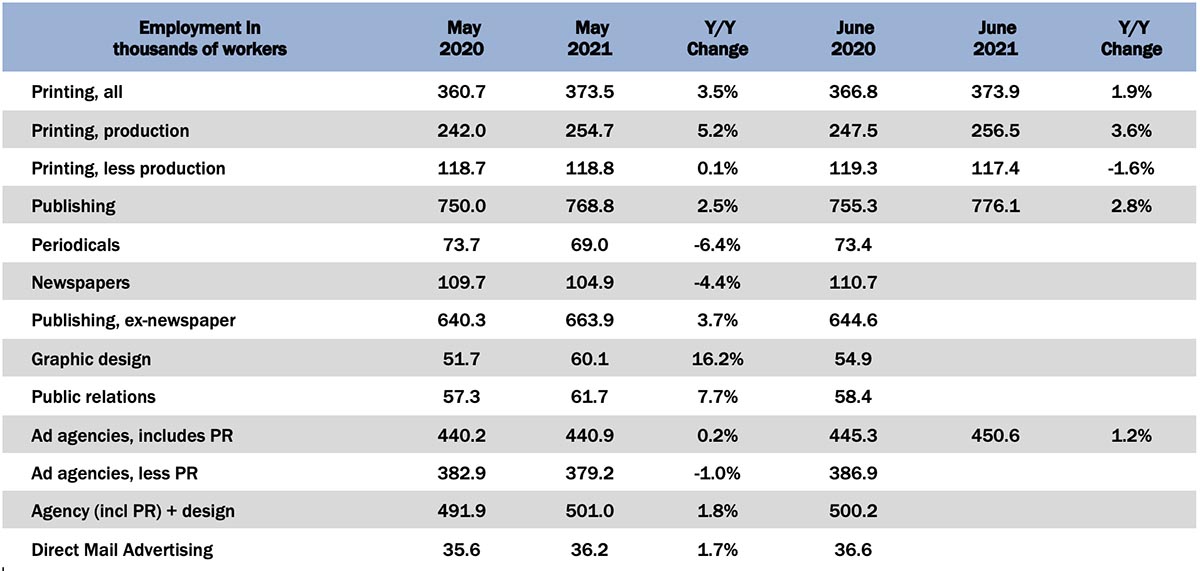

July Graphic Arts Employment—Reaching a Plateau

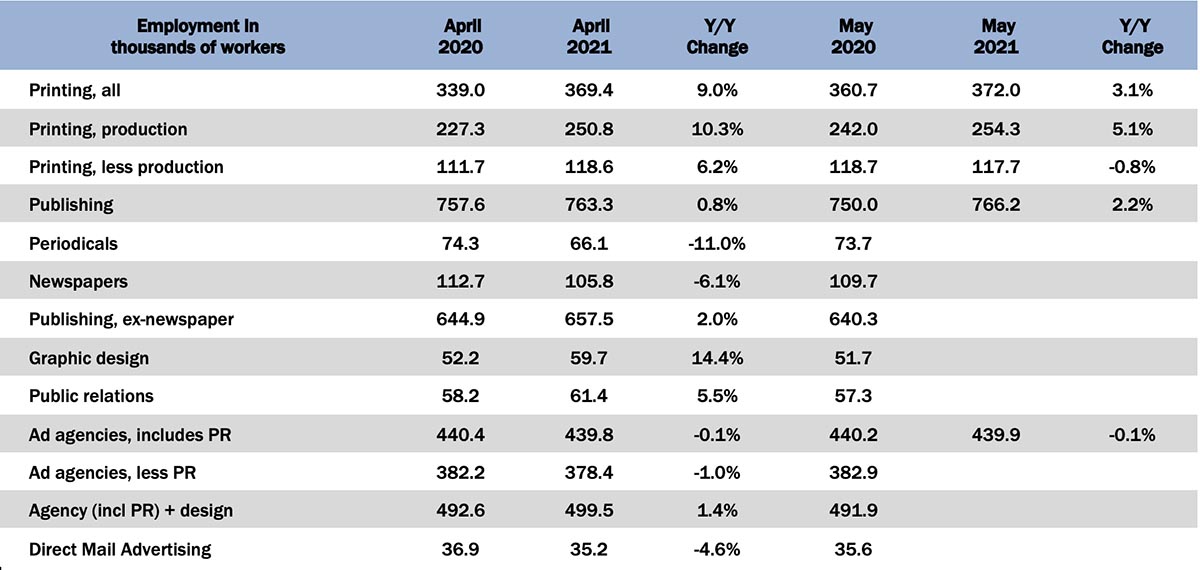

Published: August 27, 2021

In July 2021, all printing employment was down -0.2% from June, production employment up +0.7%, and non-production printing employment down -2.0%. Full Analysis

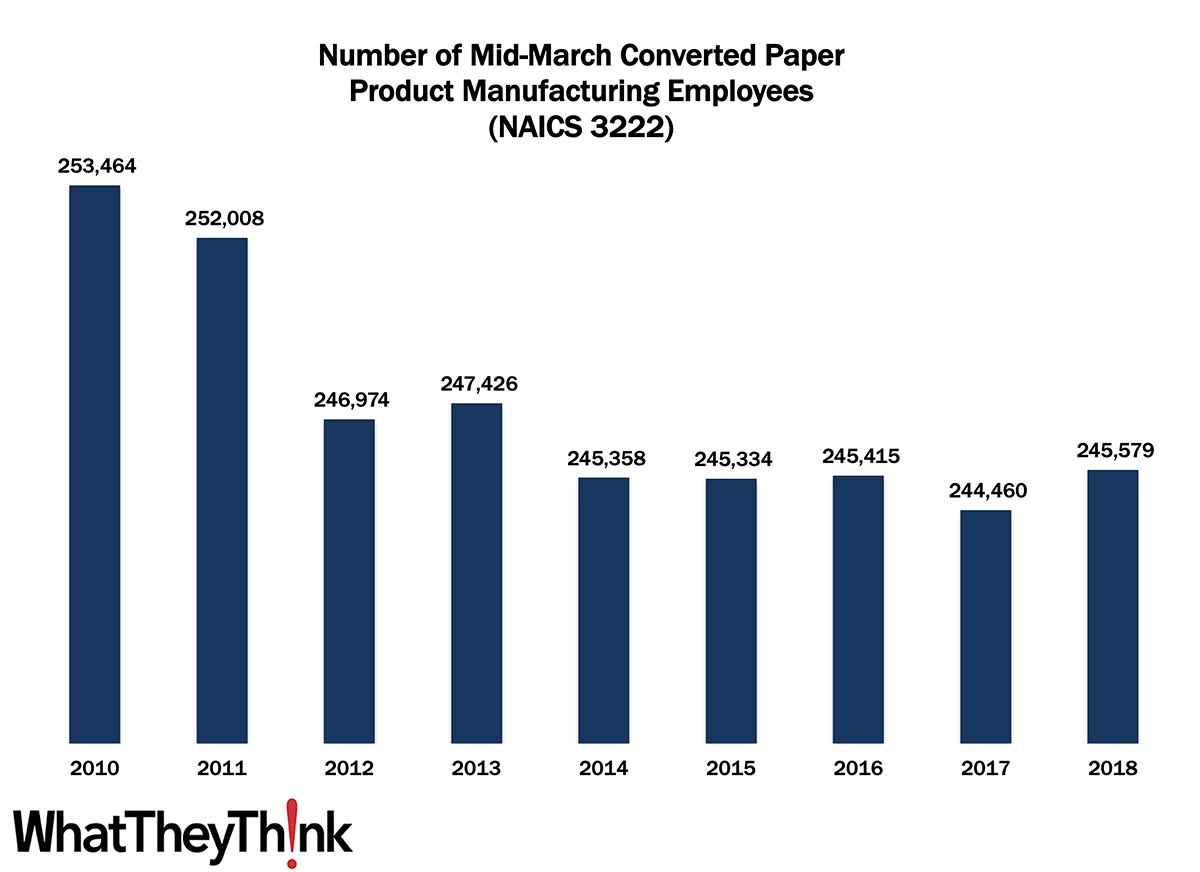

Converted Paper Product Manufacturing Employment—2010–2018

Published: August 20, 2021

According to County Business Patterns, in 2010, there were 253,464 employees in NAICS 3222 (Converted Paper Product Manufacturing establishments). Employment in this category dropped abruptly in 2012, then remained somewhat stable over the course of the decade and reaching 245,579 in 2018. In macro news, the American Institute of Architects (AIA) monthly Architecture Billings Index (ABI) show increased demand for architectural design services, good news for the signage industry. Full Analysis

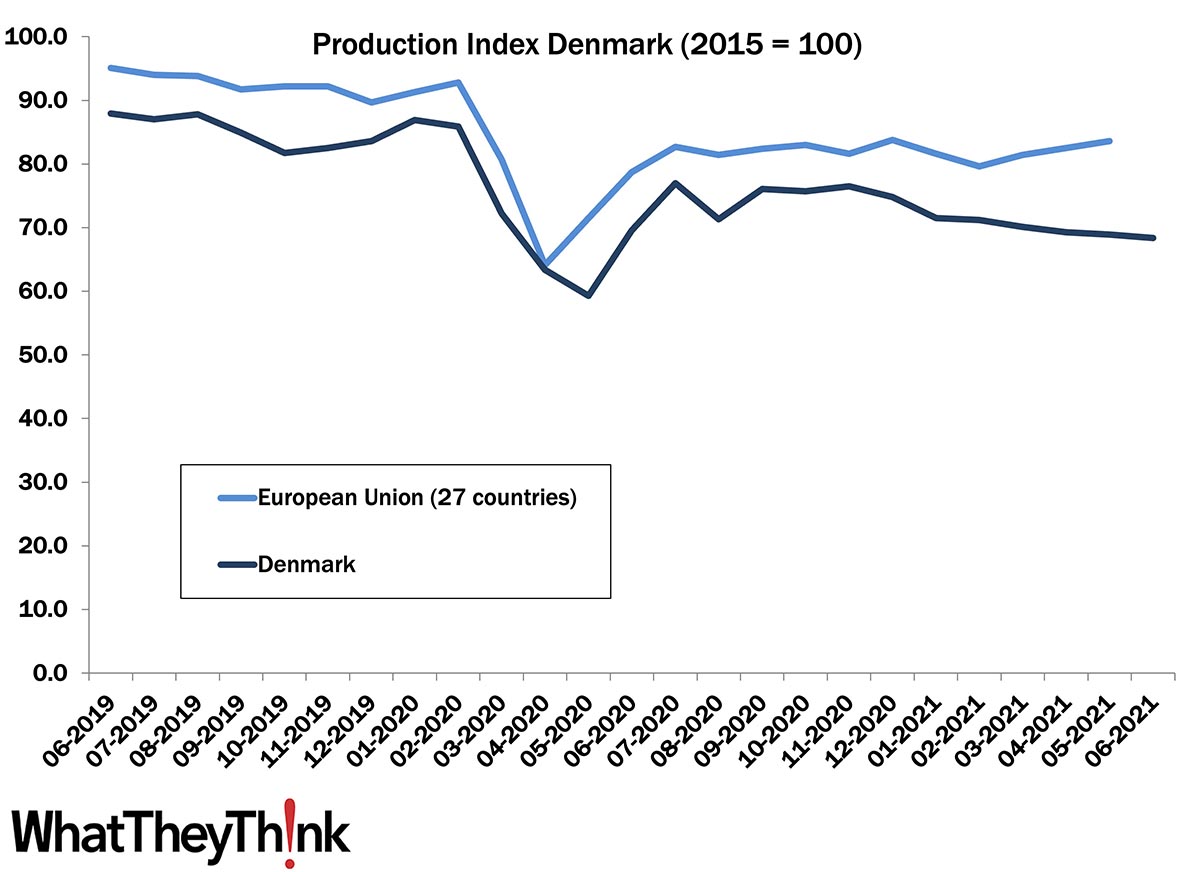

European Print Industry Snapshot: Denmark

Published: August 16, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Denmark. Full Analysis

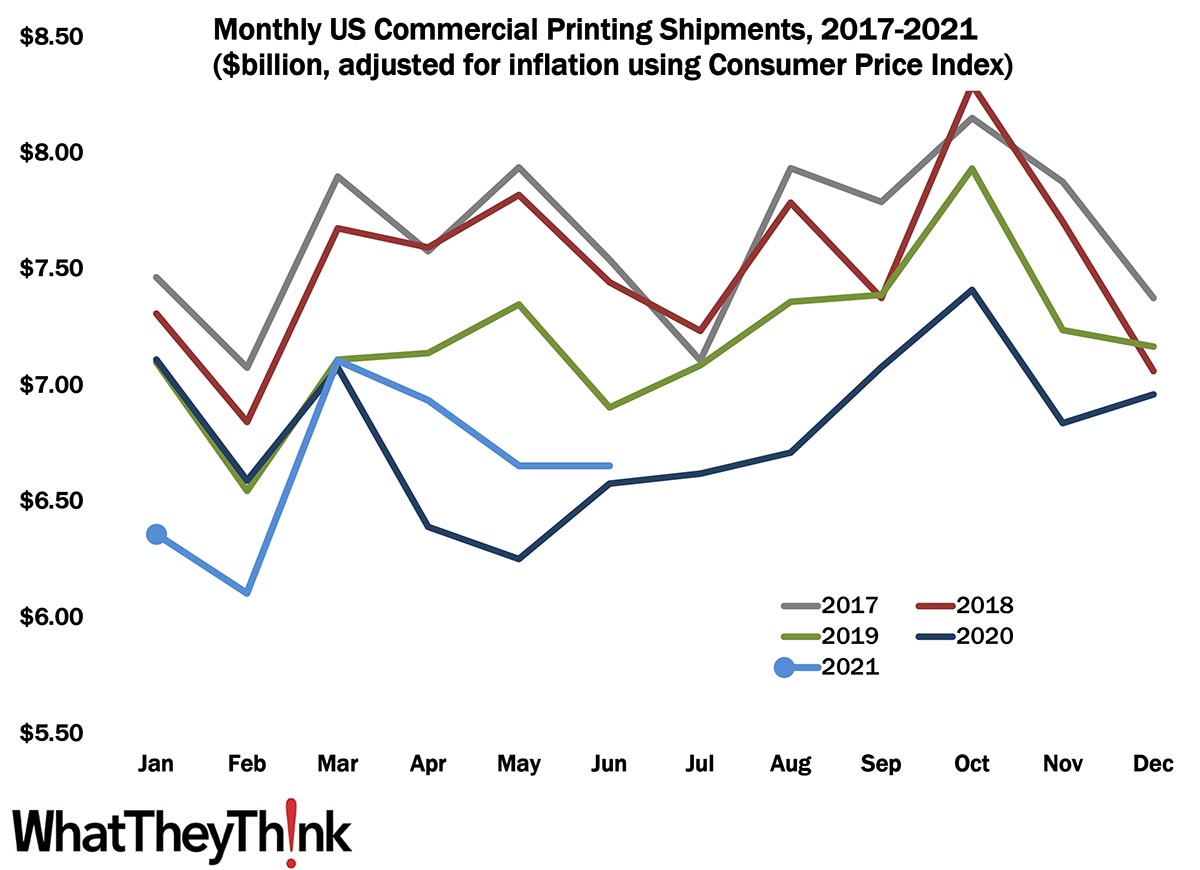

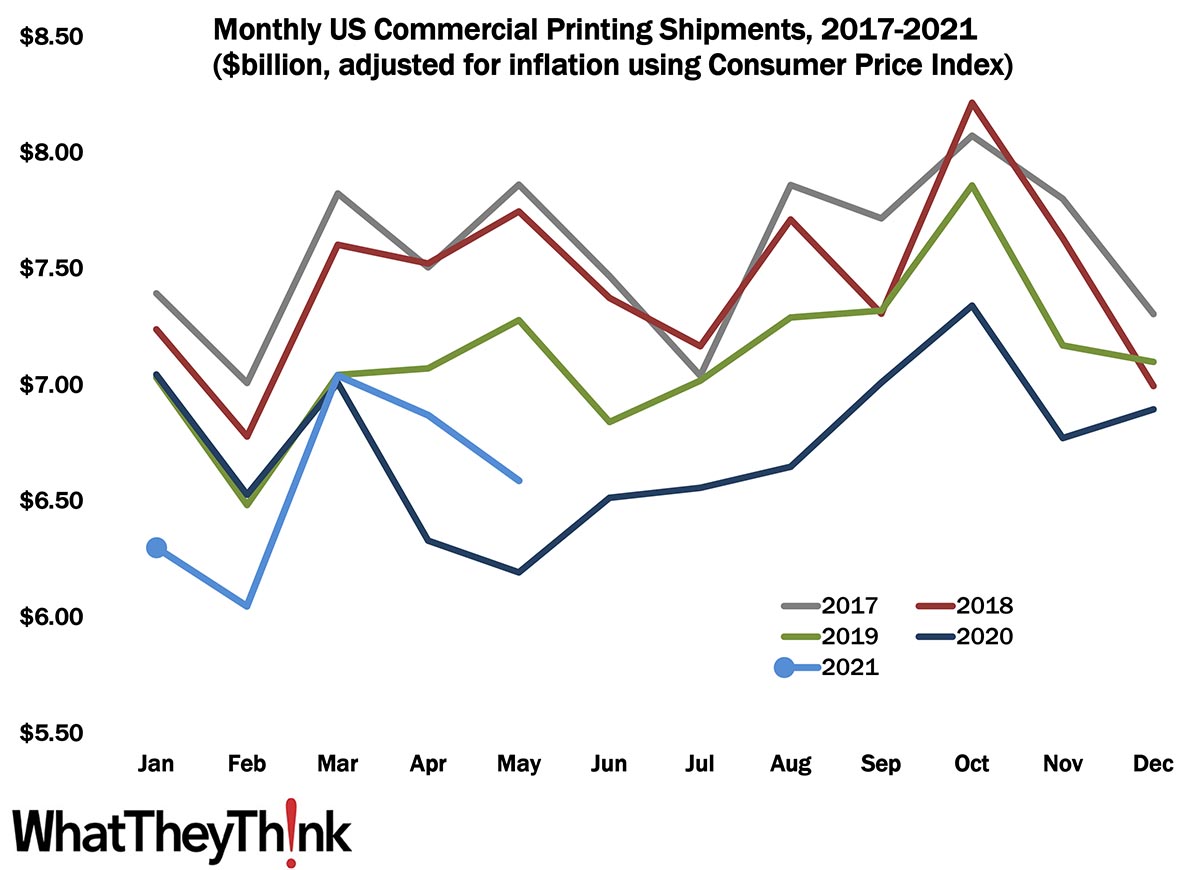

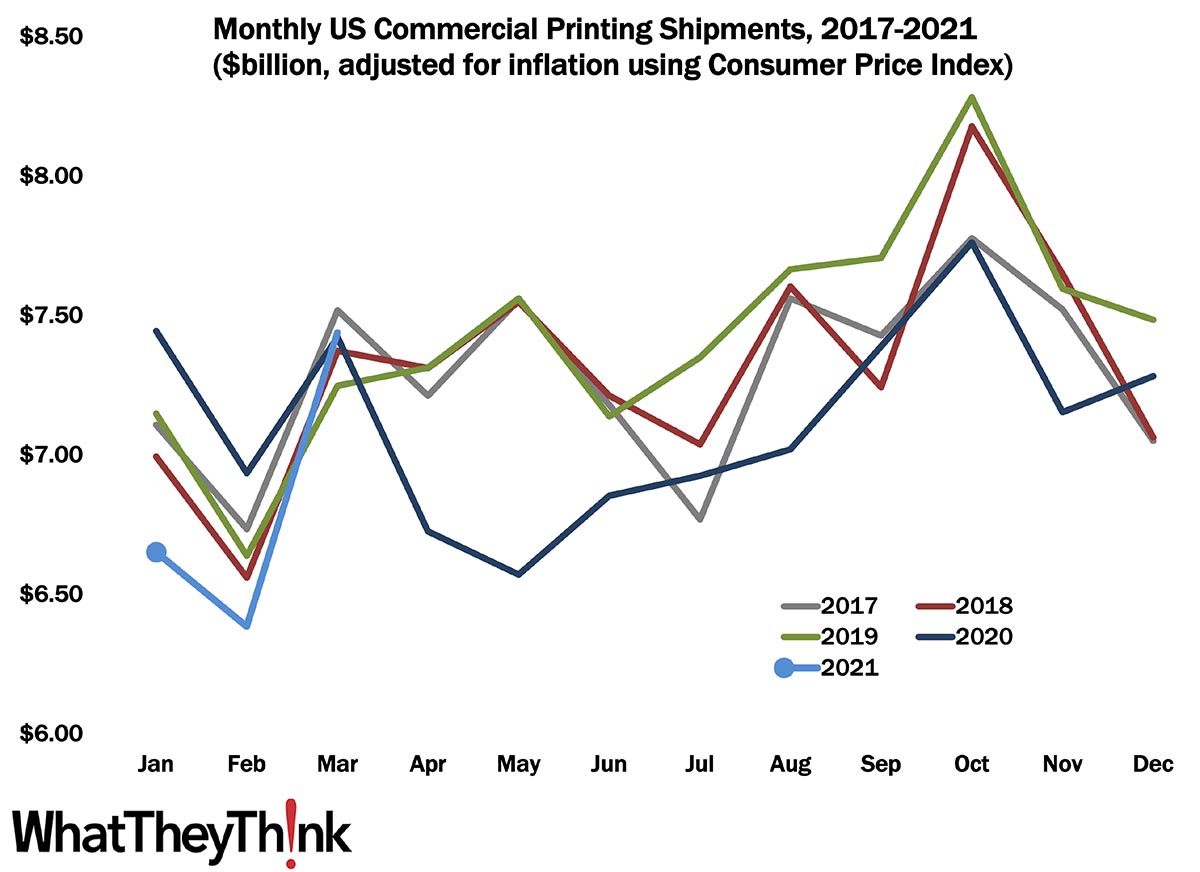

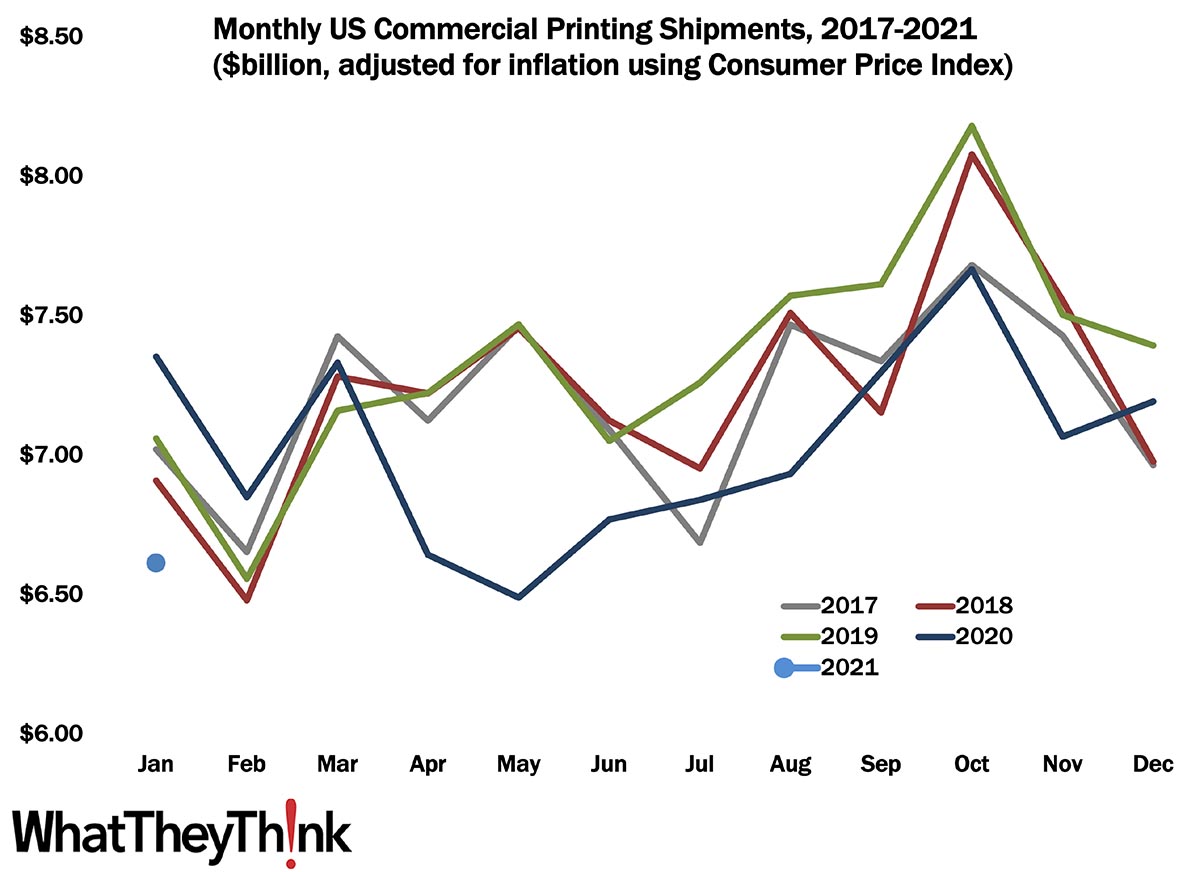

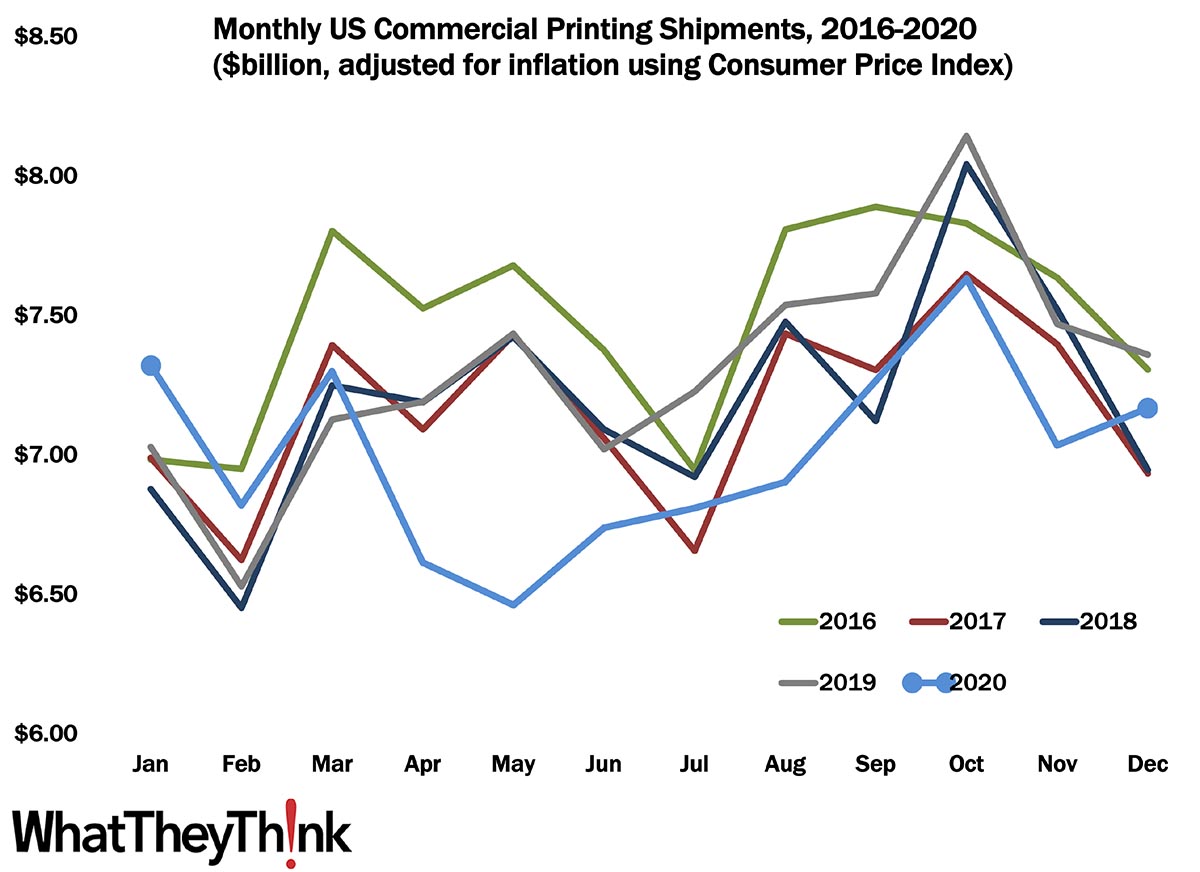

June Shipments: A Lateral Move

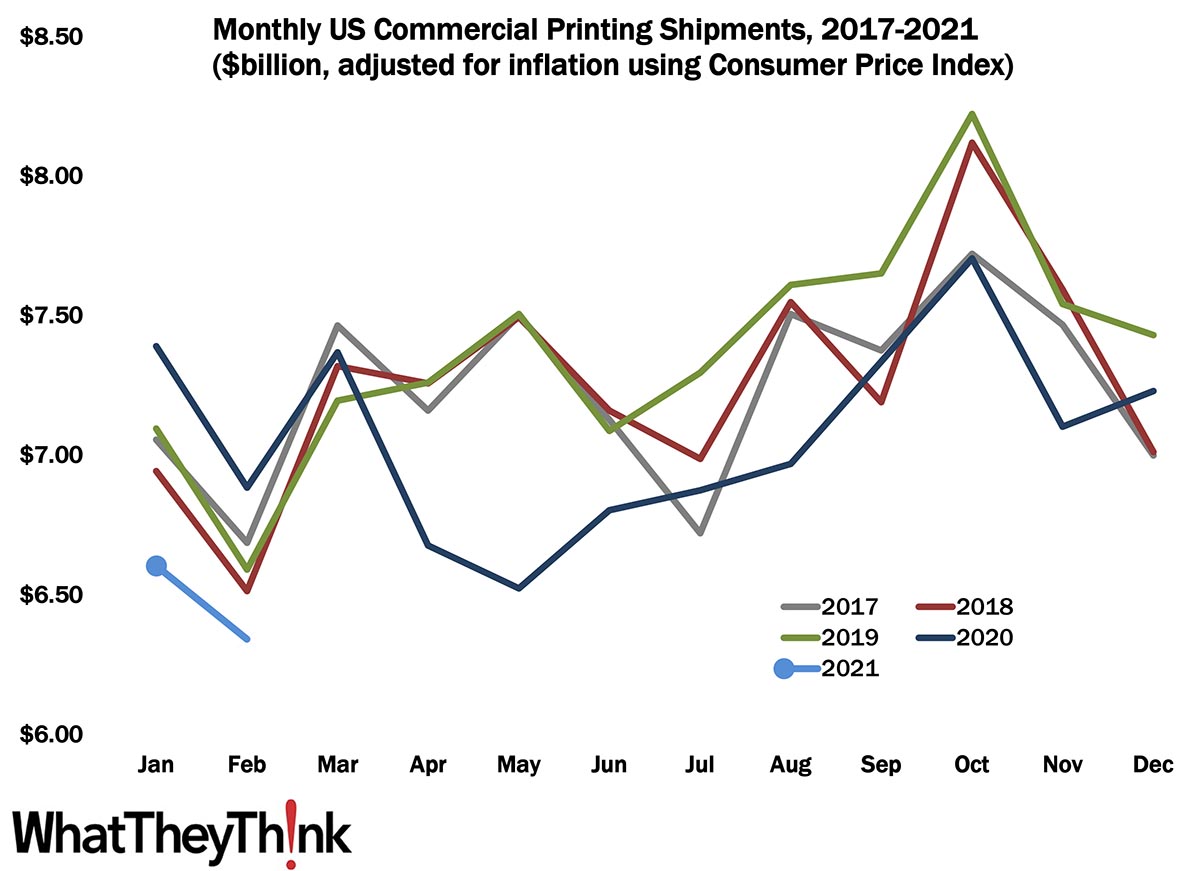

Published: August 13, 2021

June 2021 printing shipments came in at $6.65 billion, unchanged from May. We usually see declines from May to June, but at least the lateral move has halted two months of declining shipments. Full Analysis

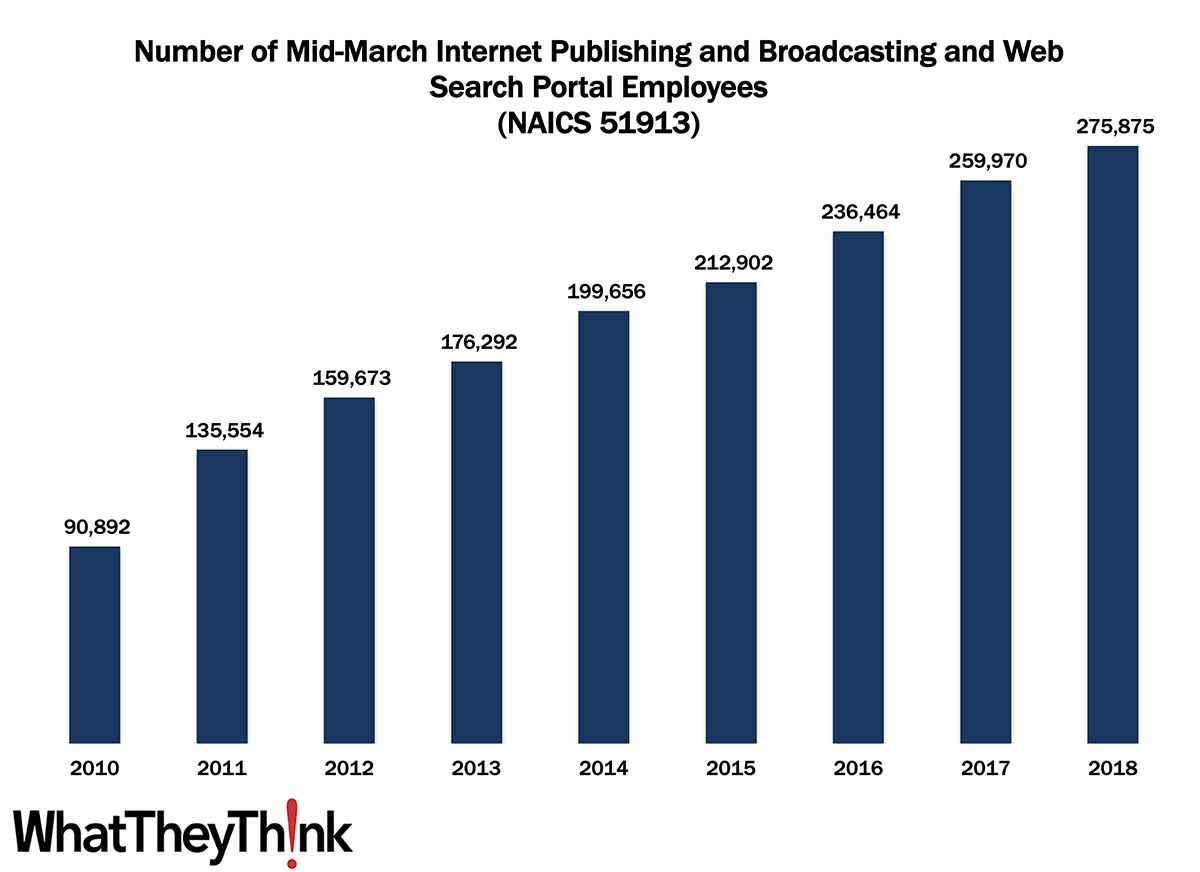

Internet Publishing Employment—2010–2018

Published: August 6, 2021

According to County Business Patterns, in 2010, there were 90,892 employees in NAICS 51913 (Internet Publishing and Broadcasting and Web Search Portals). Over the course of the decade, employment in this category grew steadily to reach 275,875 in 2018. In macro news, real GDP increased at an annual rate of 6.5% in Q2 2021. Full Analysis

June Graphic Arts Employment—Continuing to Get a Little Better

Published: July 30, 2021

In June 2021, all printing employment was up +0.1% from May, production employment up +0.7%, and non-production printing employment down -1.2%. Full Analysis

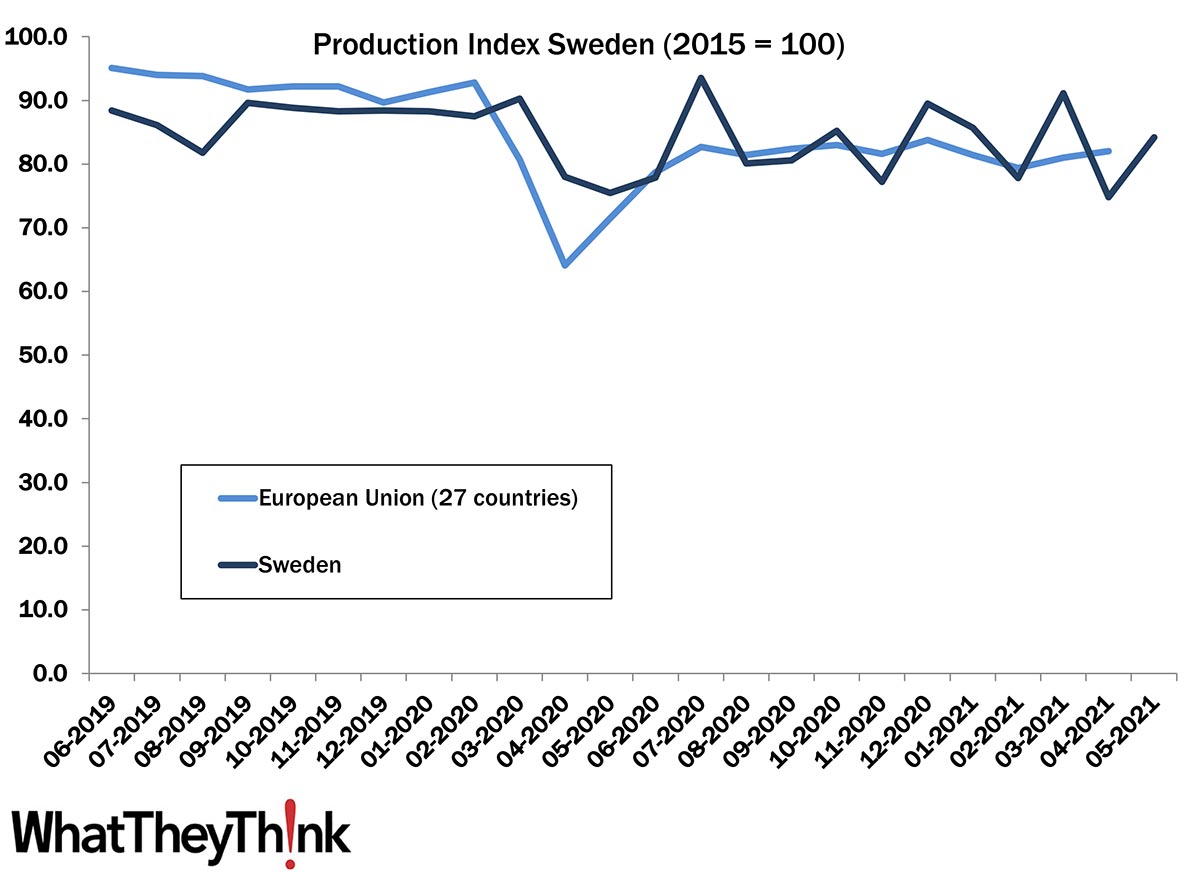

European Print Industry Snapshot: Sweden

Published: July 27, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Sweden. Full Analysis

Assorted Publishing Employment—2010–2018

Published: July 23, 2021

According to County Business Patterns, in 2010, there were 10,166 employees in NAICS 511199 (All Other Publishers). Over the course of the decade, employment in this category steadily declined to bottom out at 4,999 in 2018. In macro news, last year’s “official” COVID recession lasted only two months, according to the NBER. Full Analysis

Shipments: An Evening Out

Published: July 16, 2021

May 2021 printing shipments came in at $6.59 billion, a slight downturn from April’s $6.87 billion, and the second consecutive month of decline, but is consistent with the pattern we have been tracking over the past five years. Full Analysis

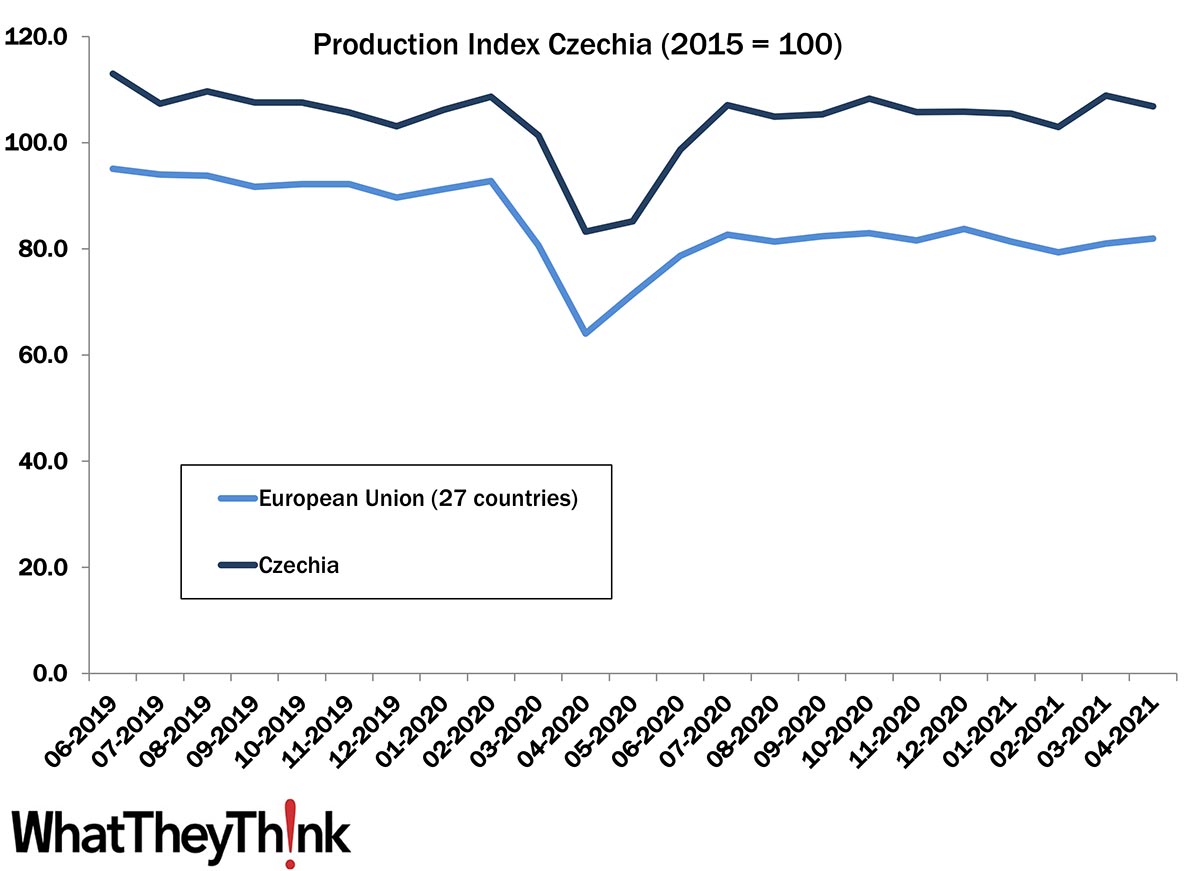

European Print Industry Snapshot: Czech Republic

Published: July 13, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in the Czech Republic. Full Analysis

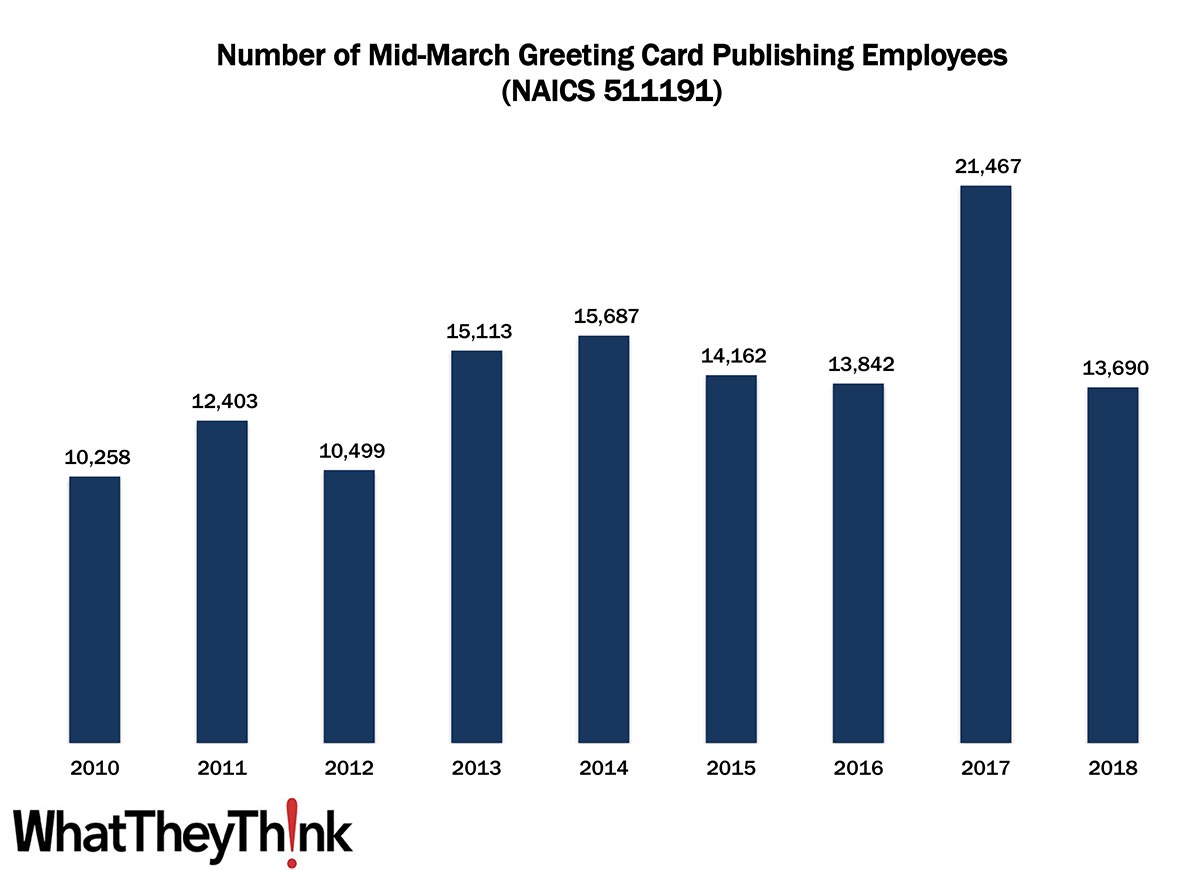

Greeting Card Publishers—2010–2018

Published: July 2, 2021

According to County Business Patterns, in 2010, there were 10,258 employees in NAICS 511191 (Greeting Card Publishers). Over the course of the decade, employment has been up and down, reaching 13,690 in 2018. In sort of macro news, Las Vegas tourism traffic rose substantially in May 2021, as conventions were poised to reopen. Full Analysis

May Graphic Arts Employment—Getting a Little Better

Published: June 25, 2021

In May 2021, all printing employment was up +0.7% from February, production employment up +1.4%, and non-production printing employment down -0.8%. Full Analysis

European Print Industry Snapshot: Poland

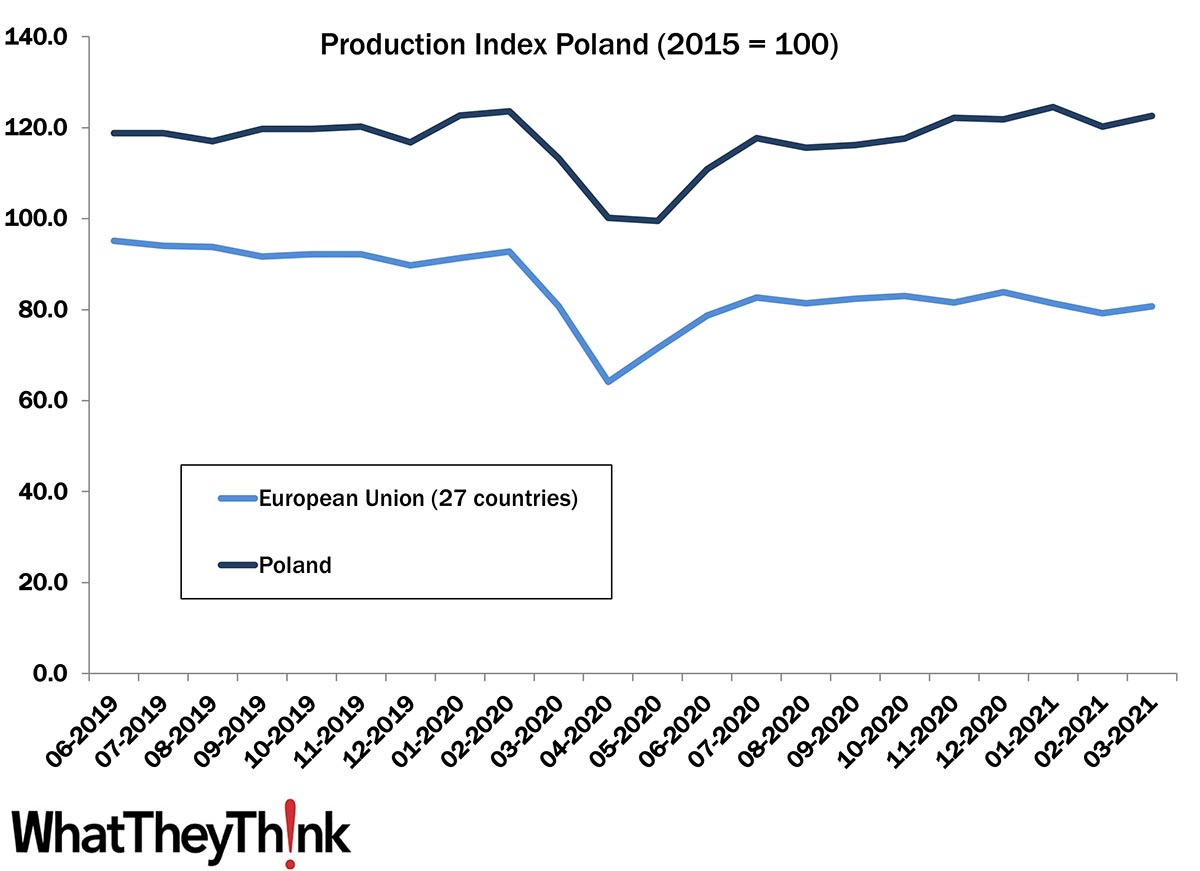

Published: June 22, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Poland. Full Analysis

Directory and Mailing List Publishers—2010–2018

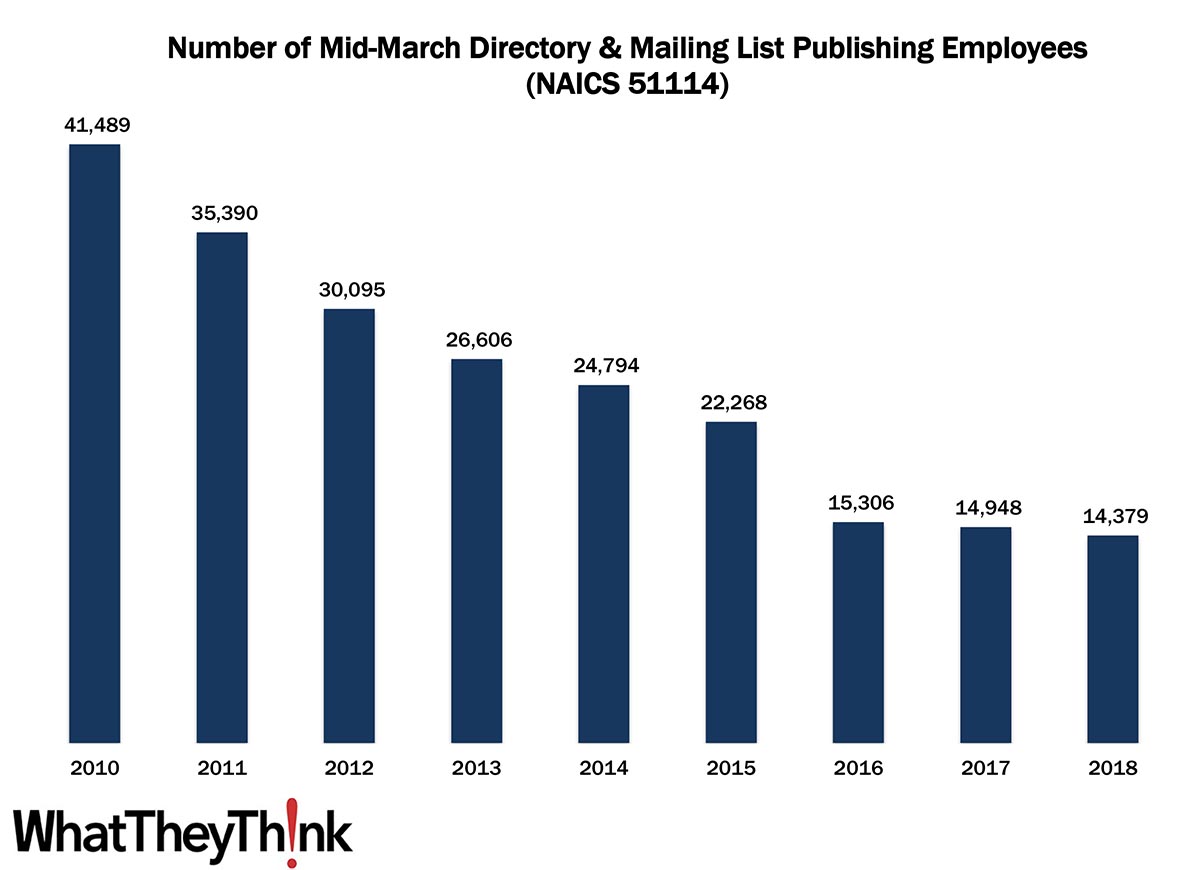

Published: June 18, 2021

According to County Business Patterns, in 2010, there were 41,489 employees in NAICS 51114 (Directory and Mailing List Publishing). Over the course of the decade, employment had plummeted to a low of 14,379. In macro news, new business creation has been at record highs. Full Analysis

Shipments: A New Season?

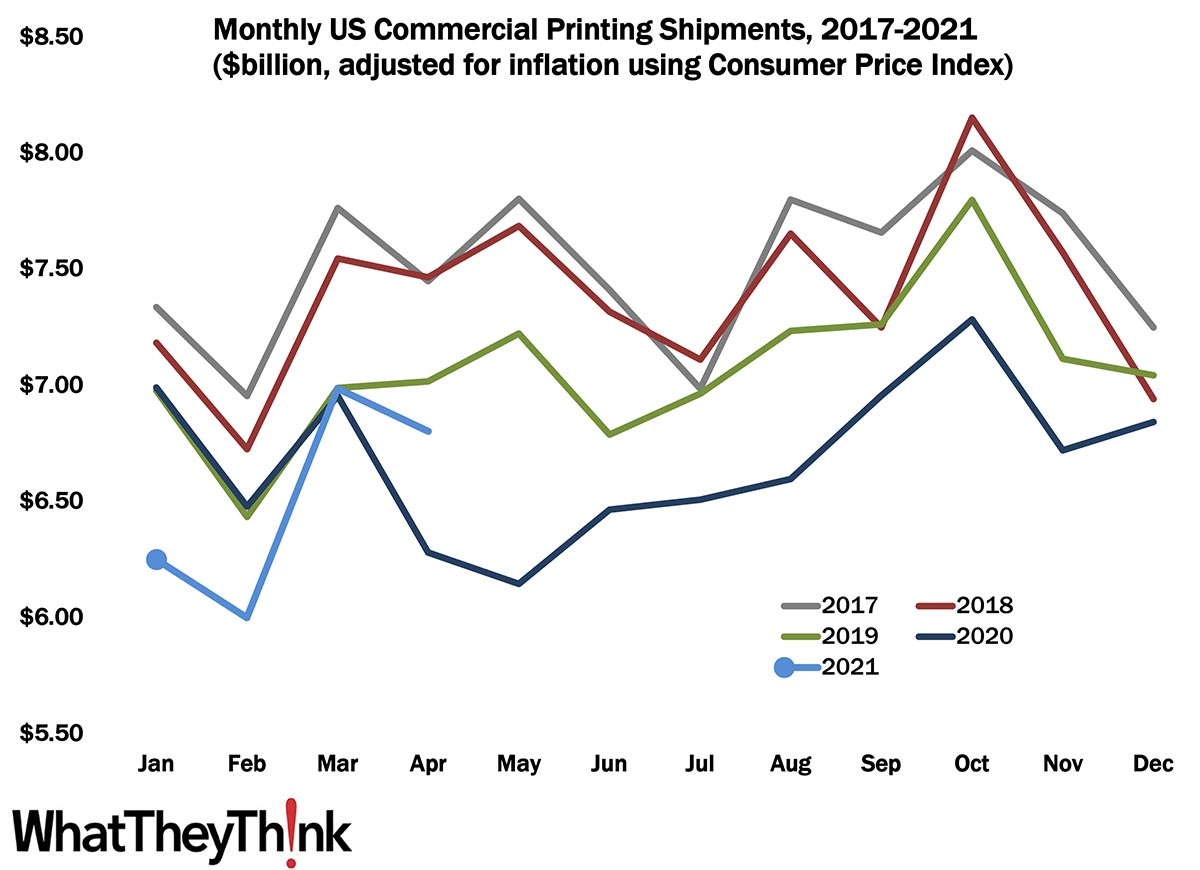

Published: June 11, 2021

April 2021 printing shipments came in at $6.80 billion, a slight downturn from March’s $6.98 billion, but is consistent with the pattern we have been tracking over the past five years. Full Analysis

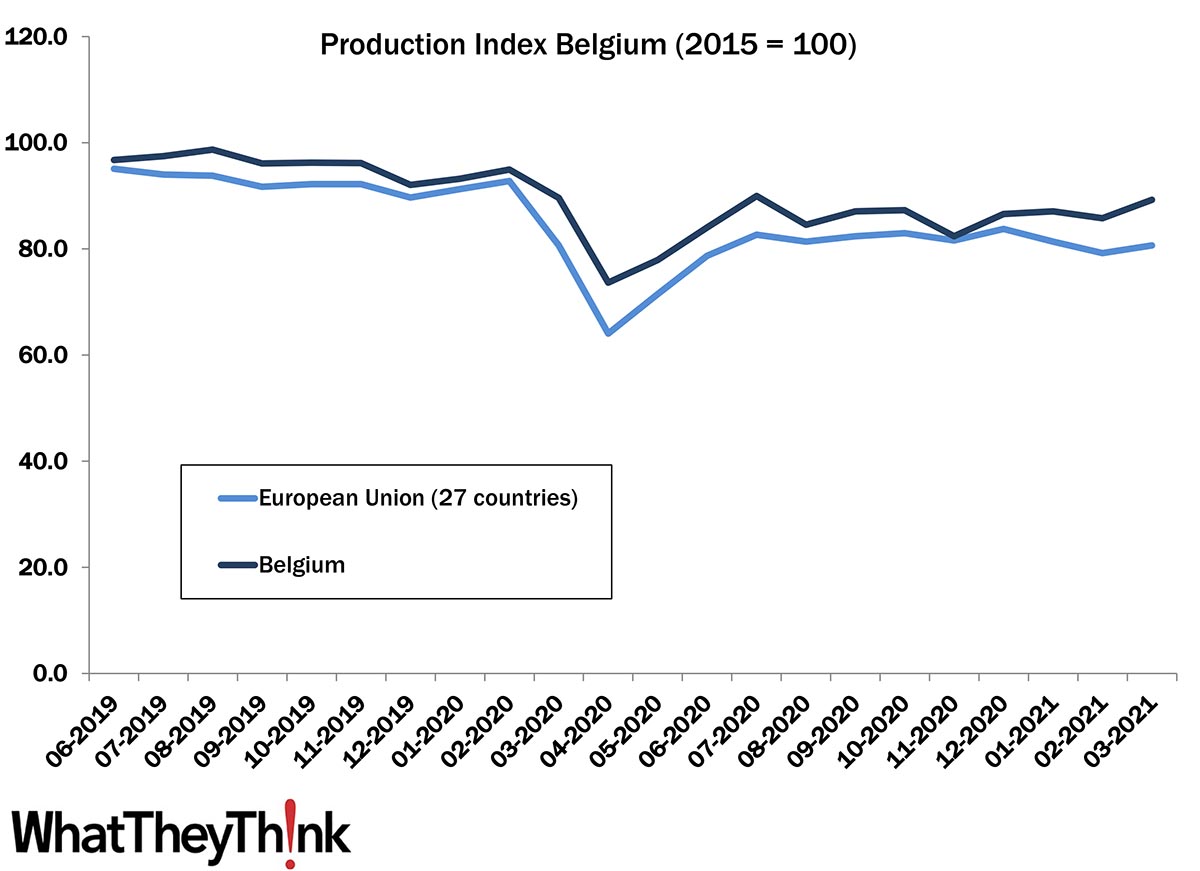

European Print Industry Snapshot: Belgium

Published: June 8, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Belgium Full Analysis

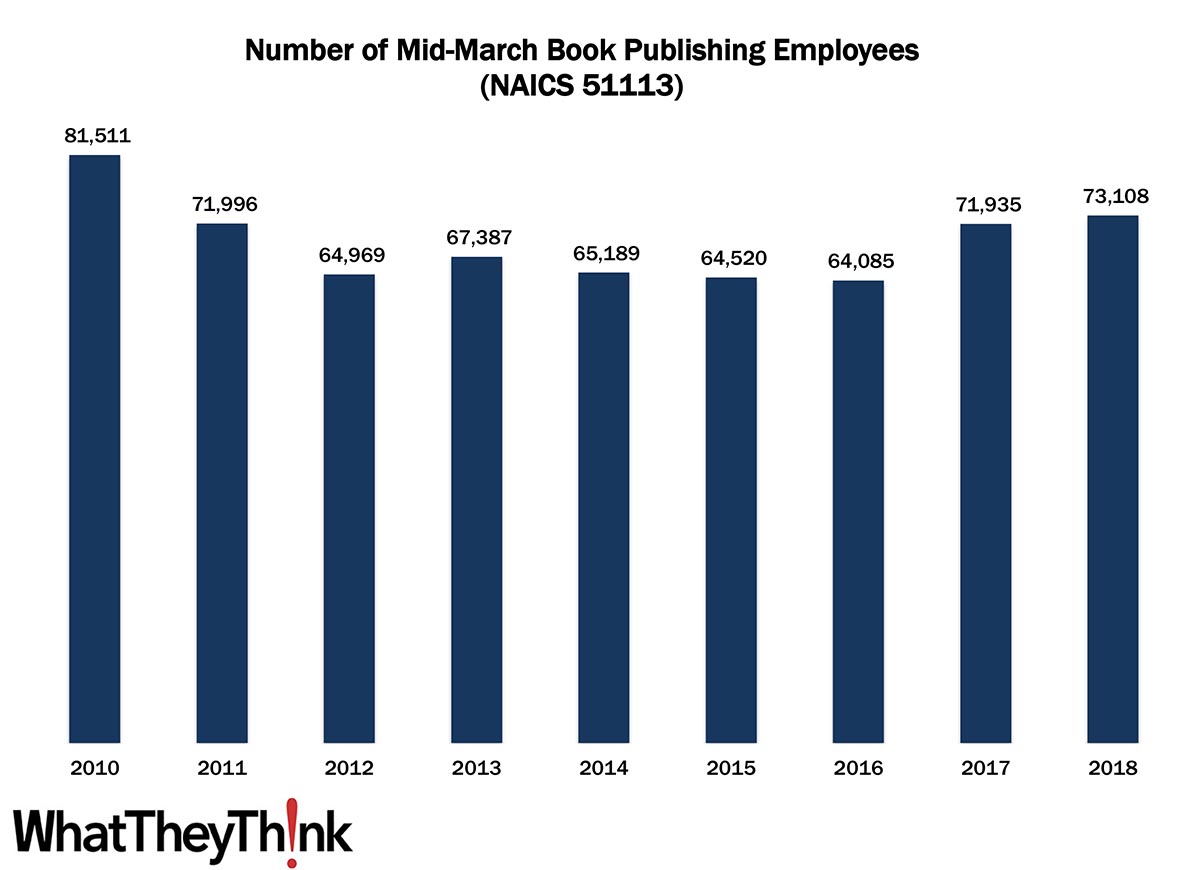

Book Publishing Employees—2010–2018

Published: June 4, 2021

According to County Business Patterns, in 2010, there were 81,511 employees in NAICS 51113 (Book Publishing). Over the course of the decade, employment had dropped to a low of 64,085, but climbed back up to 73,108 in 2018. In macro news, the Great Rebound is underway. Full Analysis

Two Macroeconomic Indicators

Published: May 28, 2021

This week’s Friday data dump looks at two macroeconomic indicators that will give us some sense of how we are bouncing back from the pandemic—the Industrial Production Index, and Retail Sales. Full Analysis

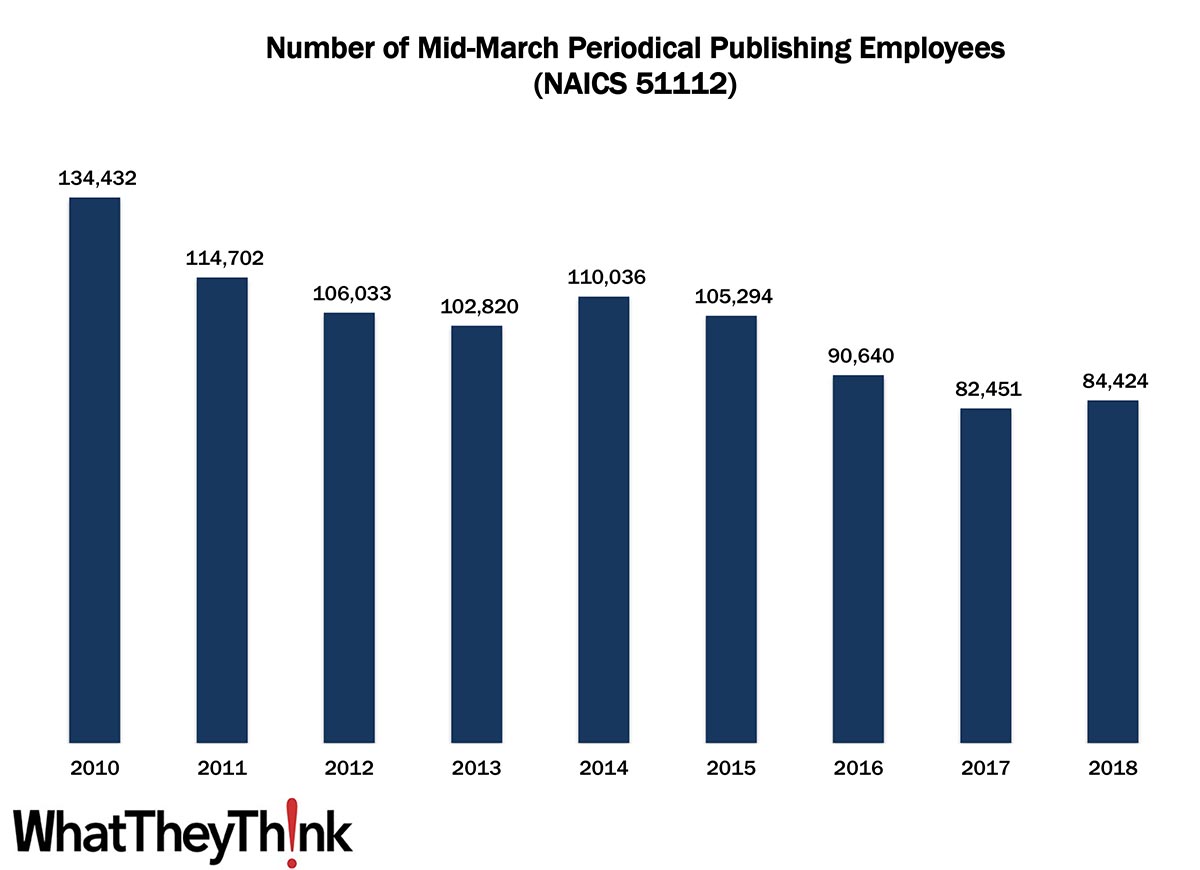

Periodical Publishing Employees—2010–2018

Published: May 21, 2021

According to County Business Patterns, in 2010, there were 134,432 employees in NAICS 51112 (Periodical Publishing). By 2018, employees had decreased to 84,424. In macro news, ecommerce as a percent of retail sales has dropped almost back to its pre-pandemic level. Full Analysis

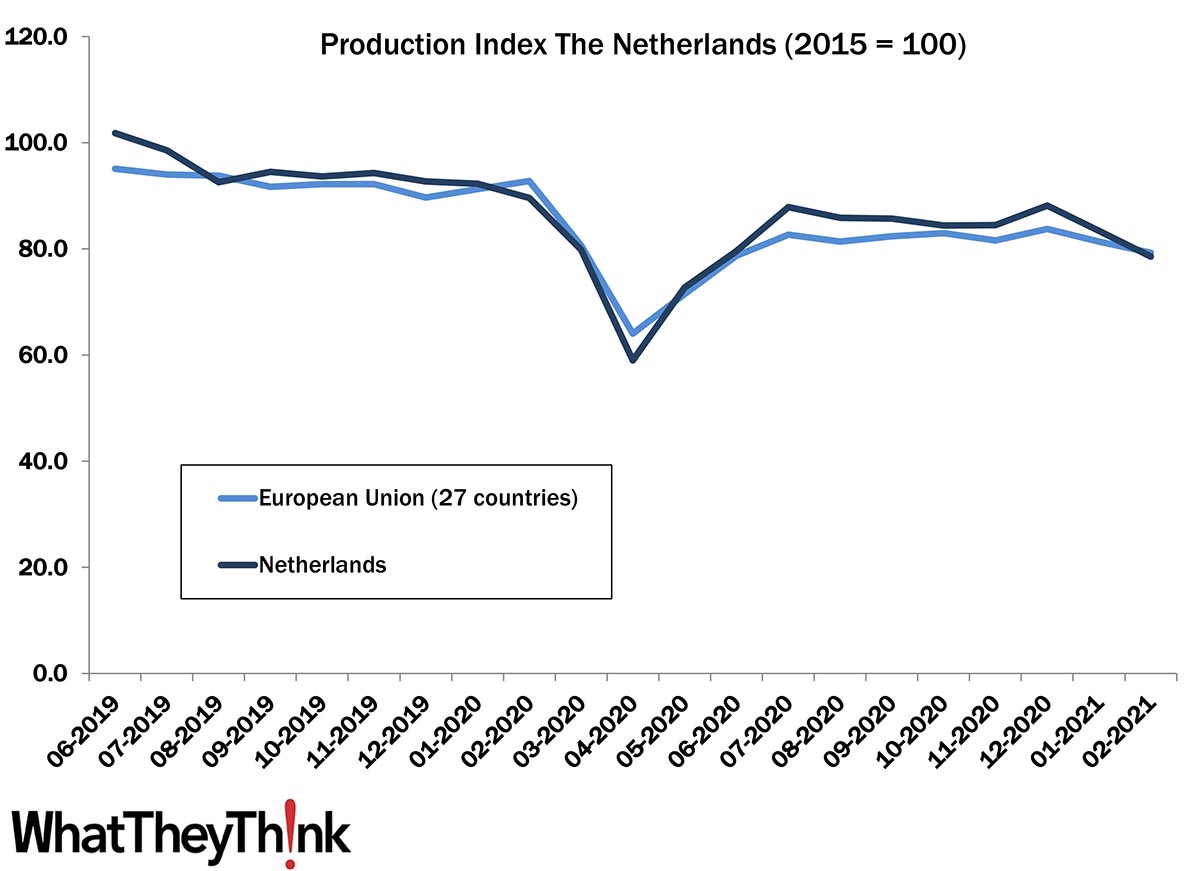

European Print Industry Snapshot: Netherlands

Published: May 18, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in the Netherlands Full Analysis

Shipments: We Told You

Published: May 14, 2021

Last month, we said that “shipments can only get better from here”—and we were right. March shipments roared back from a historical low of $6.39 billion in February to $7.44 billion in March, the second best March in the past five years. Full Analysis

March Graphic Arts Employment—Getting Back to Work

Published: May 7, 2021

In March 2021, all printing employment was up +1.5% from February, production employment up +1.1%, and non-production printing employment up +2.2%. Full Analysis

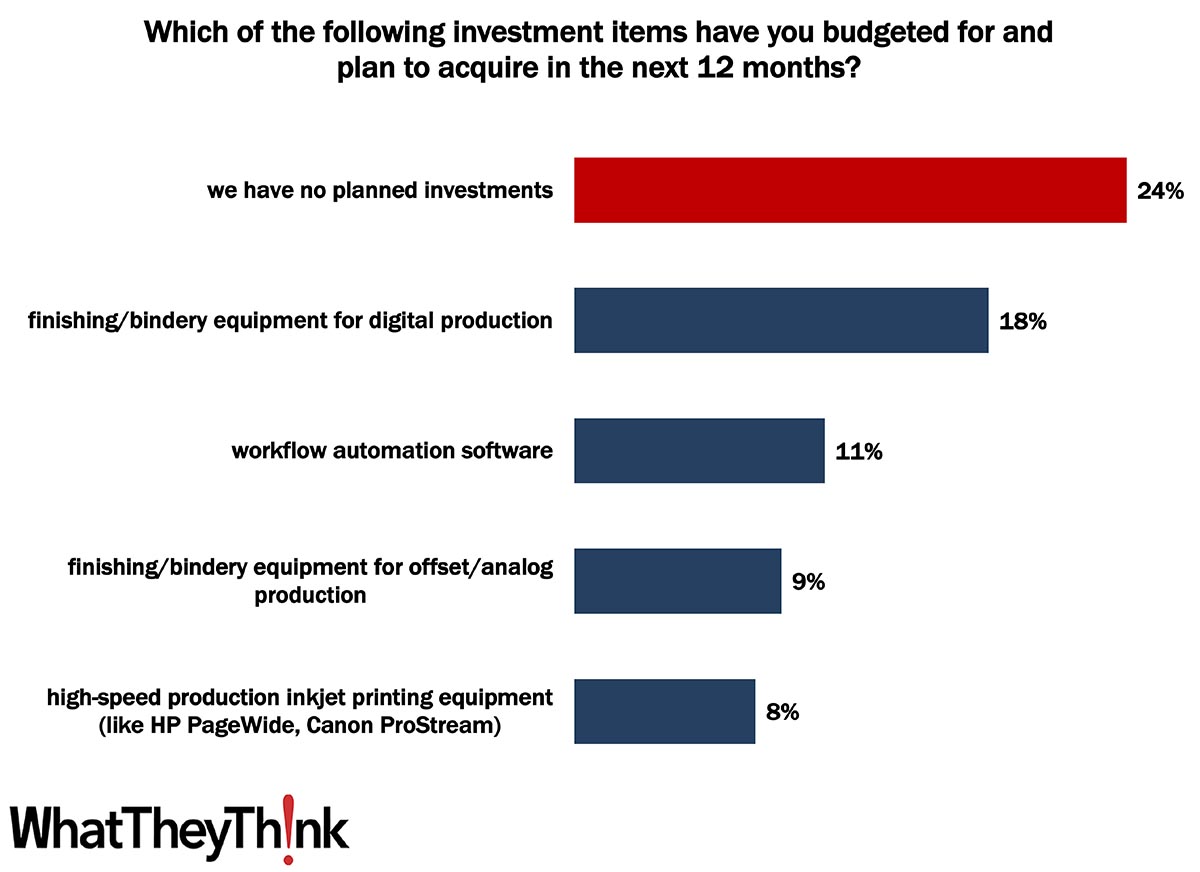

Printing 2021 Quick Look: Top Investments

Published: May 5, 2021

According to data from our recently published Printing Outlook 2021 special report, one-fourth of print businesses have no major investment plans for 2021. Full Analysis

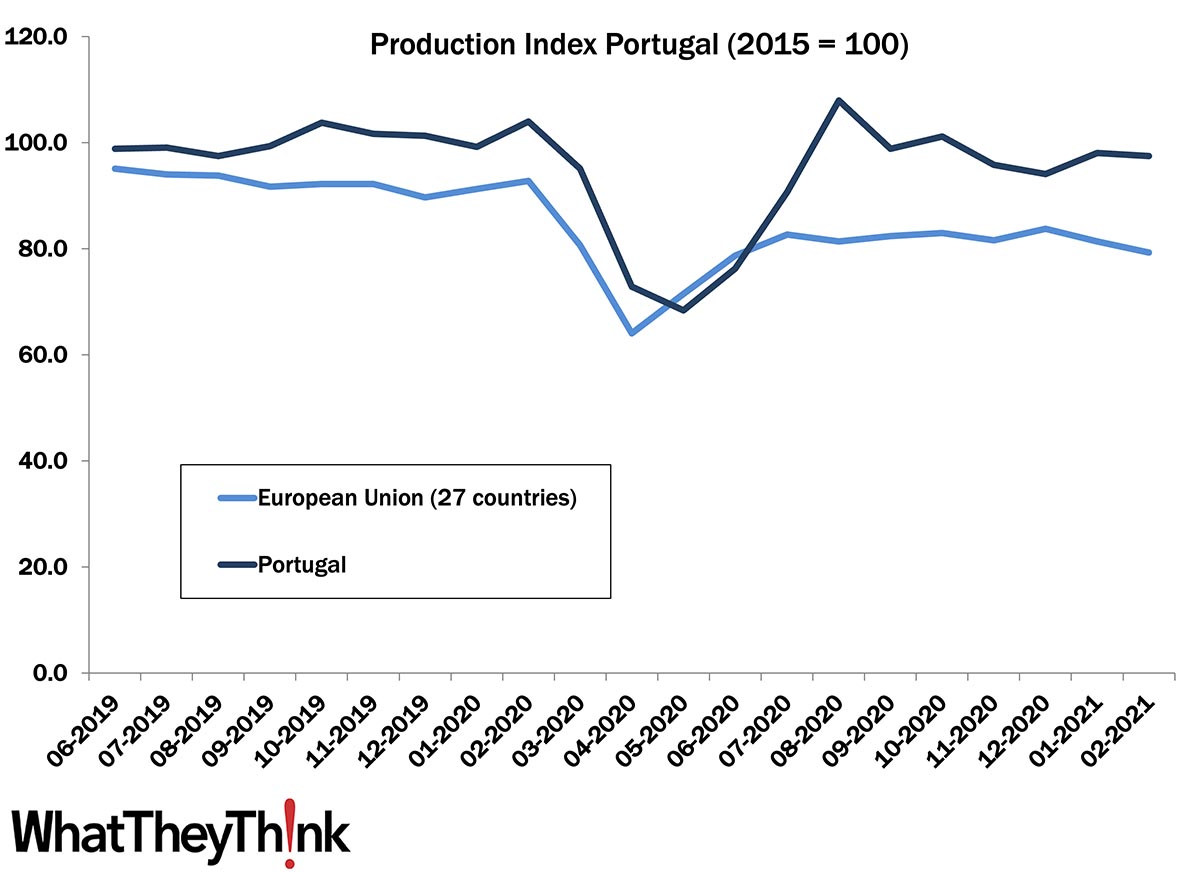

European Print Industry Snapshot: Portugal

Published: May 4, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Portugal. Full Analysis

Newspaper Publishing Employees—2010–2018

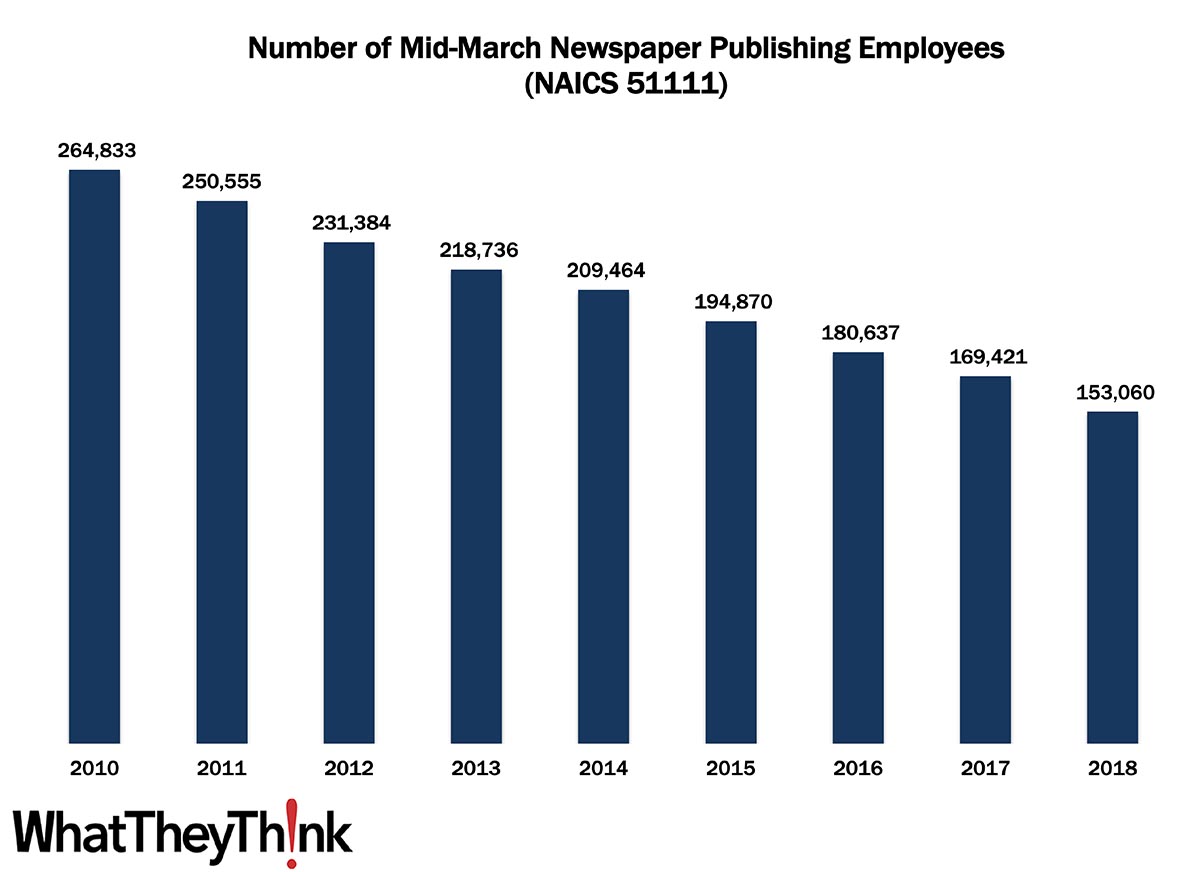

Published: April 30, 2021

According to County Business Patterns, in 2010, there were 264,833 employees in NAICS 51111 (Newspaper Publishing). By 2018, employees had decreased to 153,060. In macro news, Q1 GDP was up 6.4%. Full Analysis

Shipments: They Can Only Get Better from Here

Published: April 23, 2021

We didn’t kick off 2021 very auspiciously, with January printing shipments coming in at $6.57 billion, down from December 2020’s $7.17 billion, and then a further drop in February to $6.34 billion. Full Analysis

Printing 2021 Quick Look: Top Challenges

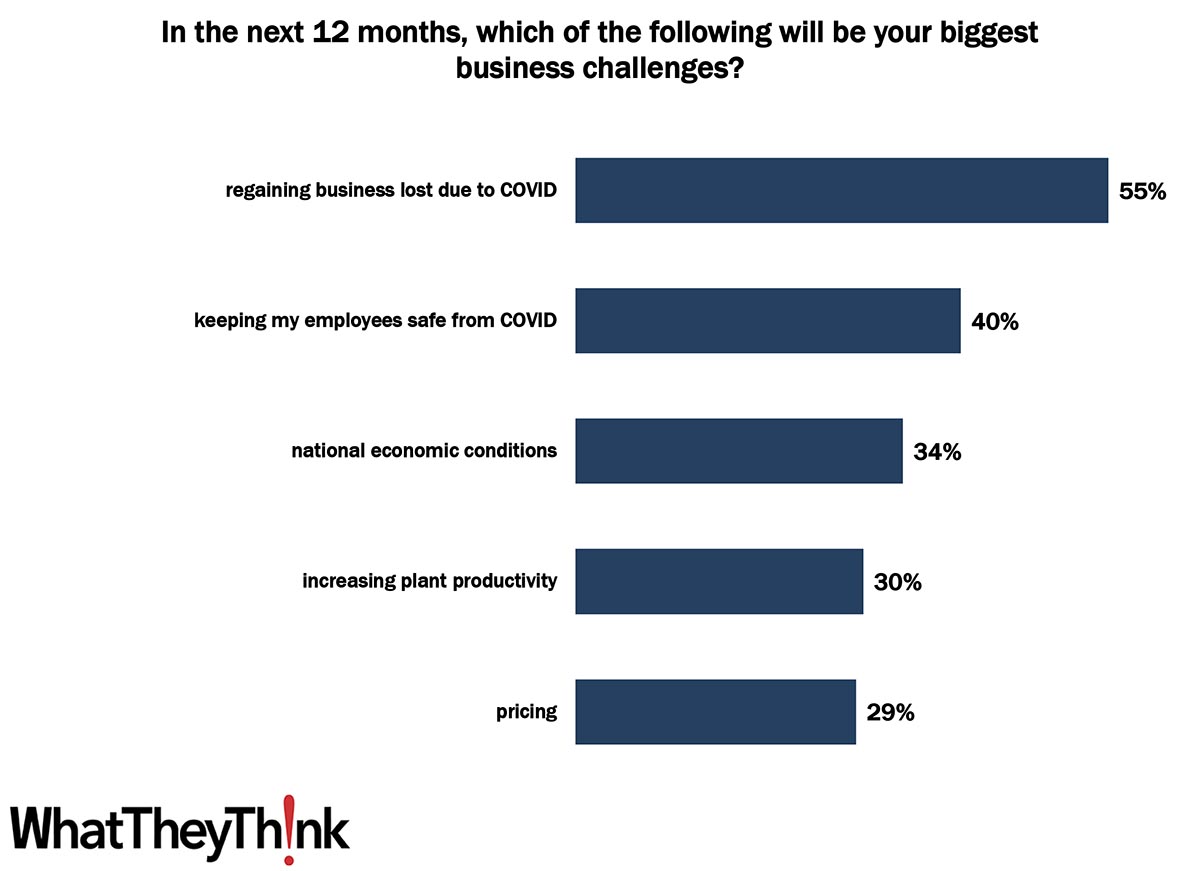

Published: April 21, 2021

According to data from our recently published Printing Outlook 2021 special report, recovering business lost to COVID and national economic conditions dominated printers’ top challenges—but traditional challenges will gain prominence post-COVID. Full Analysis

European Print Industry Snapshot: Spain

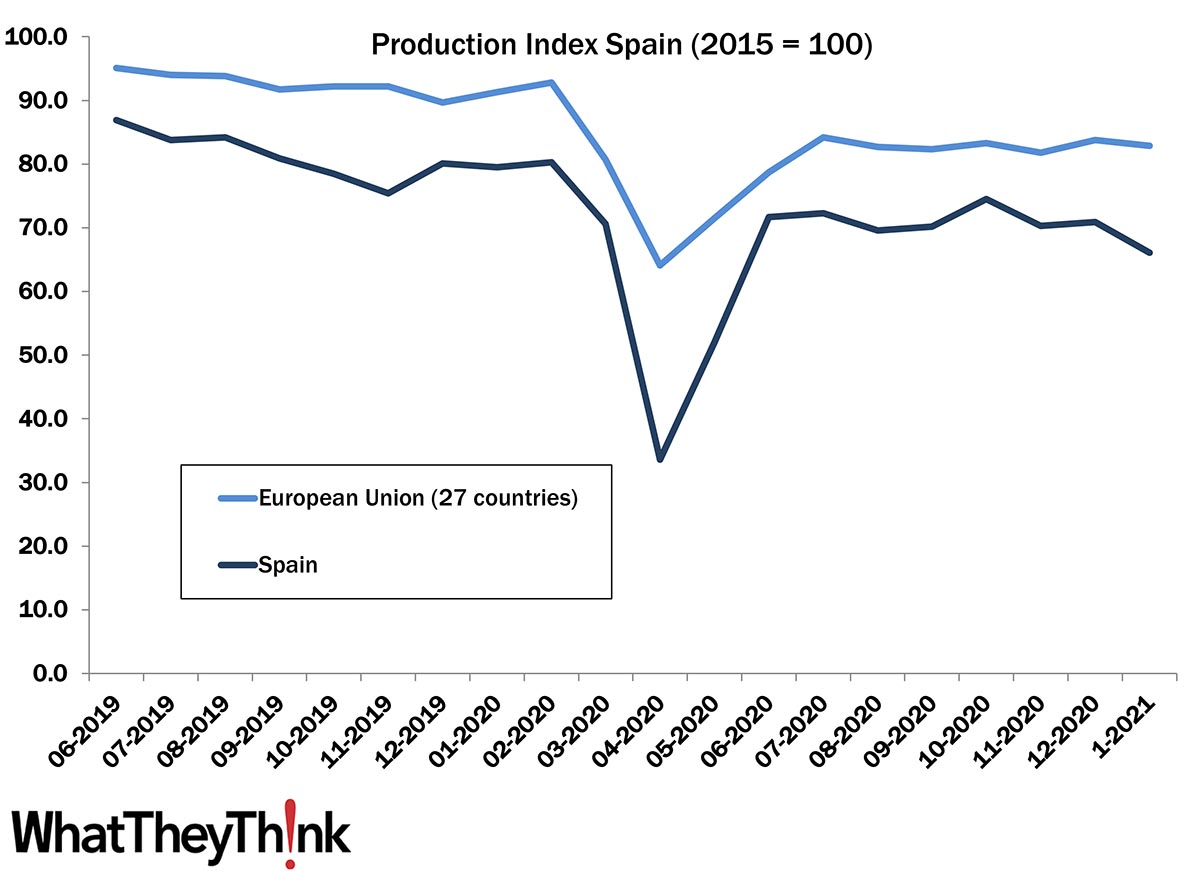

Published: April 20, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Spain. Full Analysis

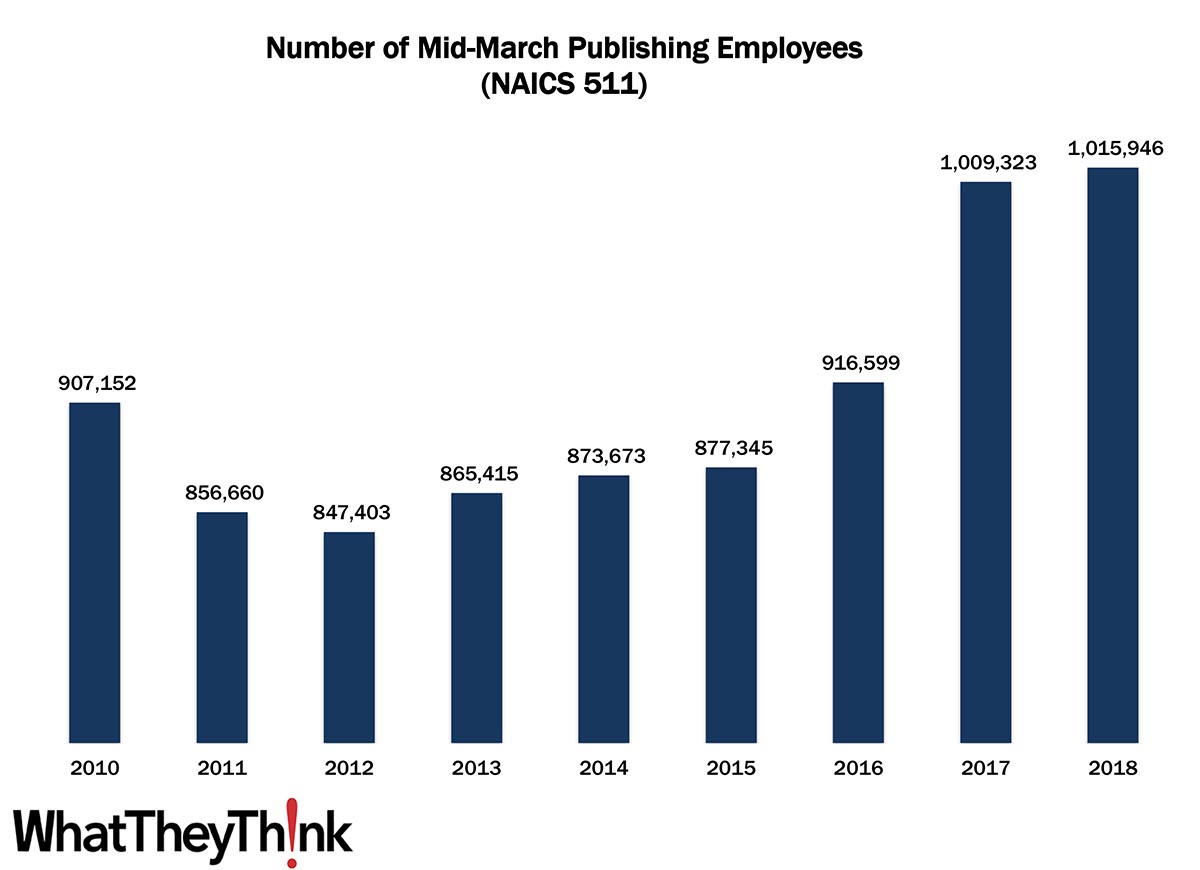

Publishing Employees—2010–2018

Published: April 16, 2021

According to County Business Patterns, in 2010, there were 907,152 employees in NAICS 511 (Publishing Industries—except Internet). By 2018, employees had increased to 1,015,946. In macro news, retail sales were up 9.8% in March. Full Analysis

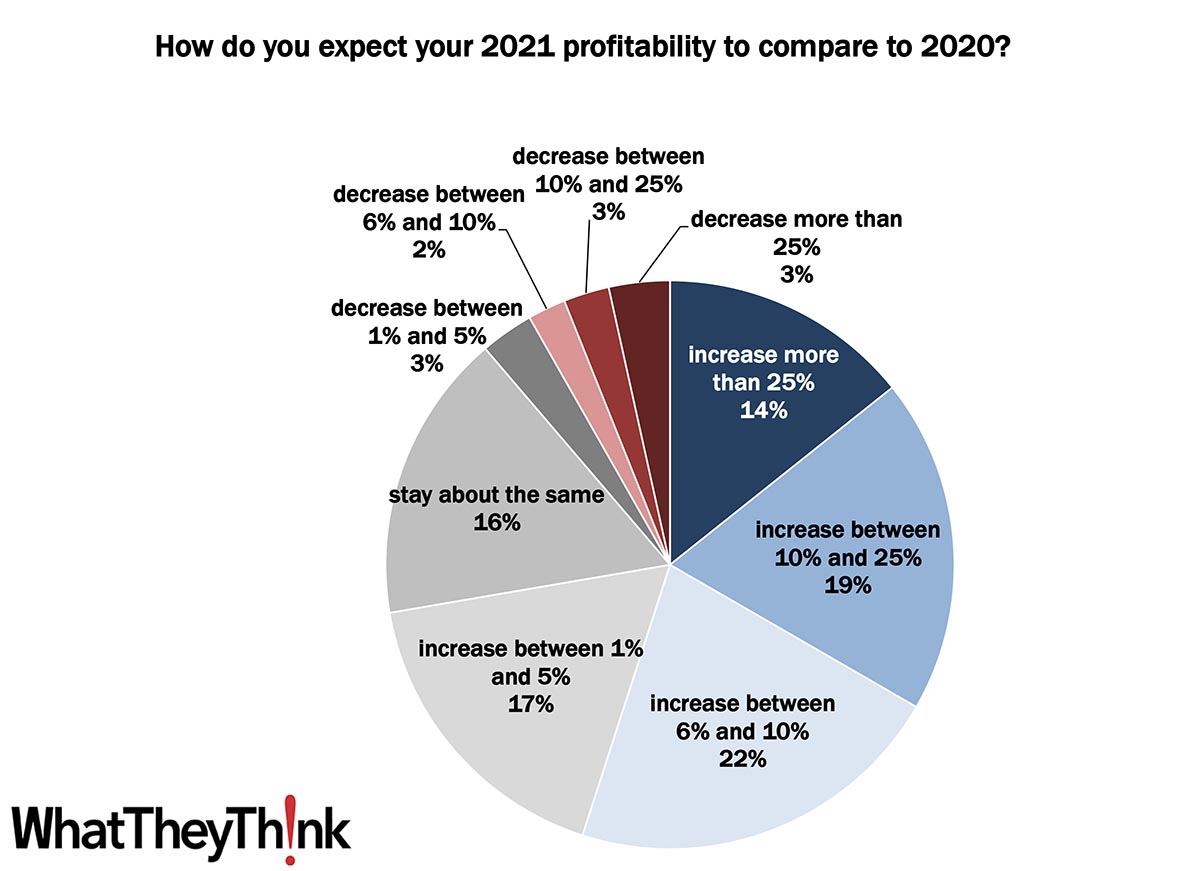

Printing 2021 Quick Look: 2021 Profits

Published: April 14, 2021

According to data from our recently published Printing Outlook 2021 special report, print businesses expect a +8.1% increase in profits from 2020 to 2021. Full Analysis

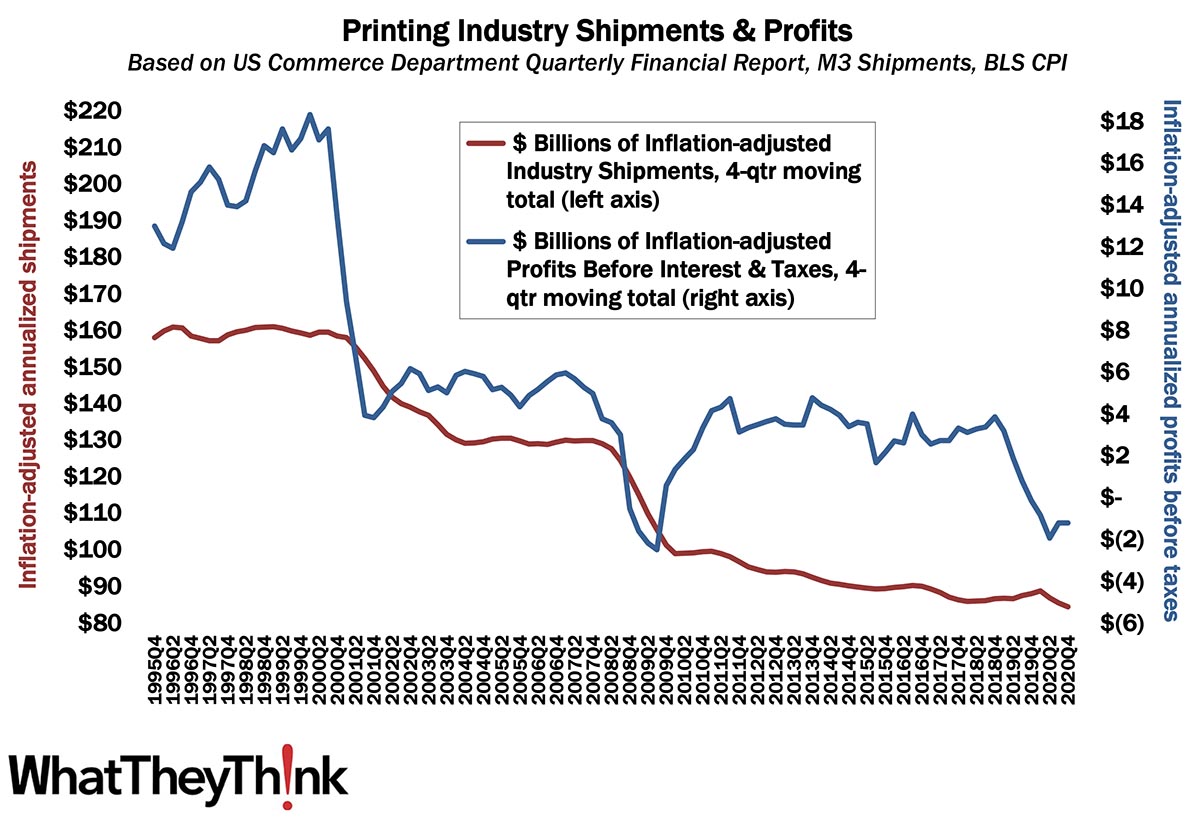

Profits: Back to the Tale of Two Cities

Published: April 9, 2021

We’ve long been calling it “a tale of two cities”—large printers and small/mid-size printers and the profitability gap between them. The pandemic interrupted this ongoing narrative temporarily, but back in Q3 2020, we started to return to normal, at least in terms of industry profits trends, which continued into Q4. Full Analysis

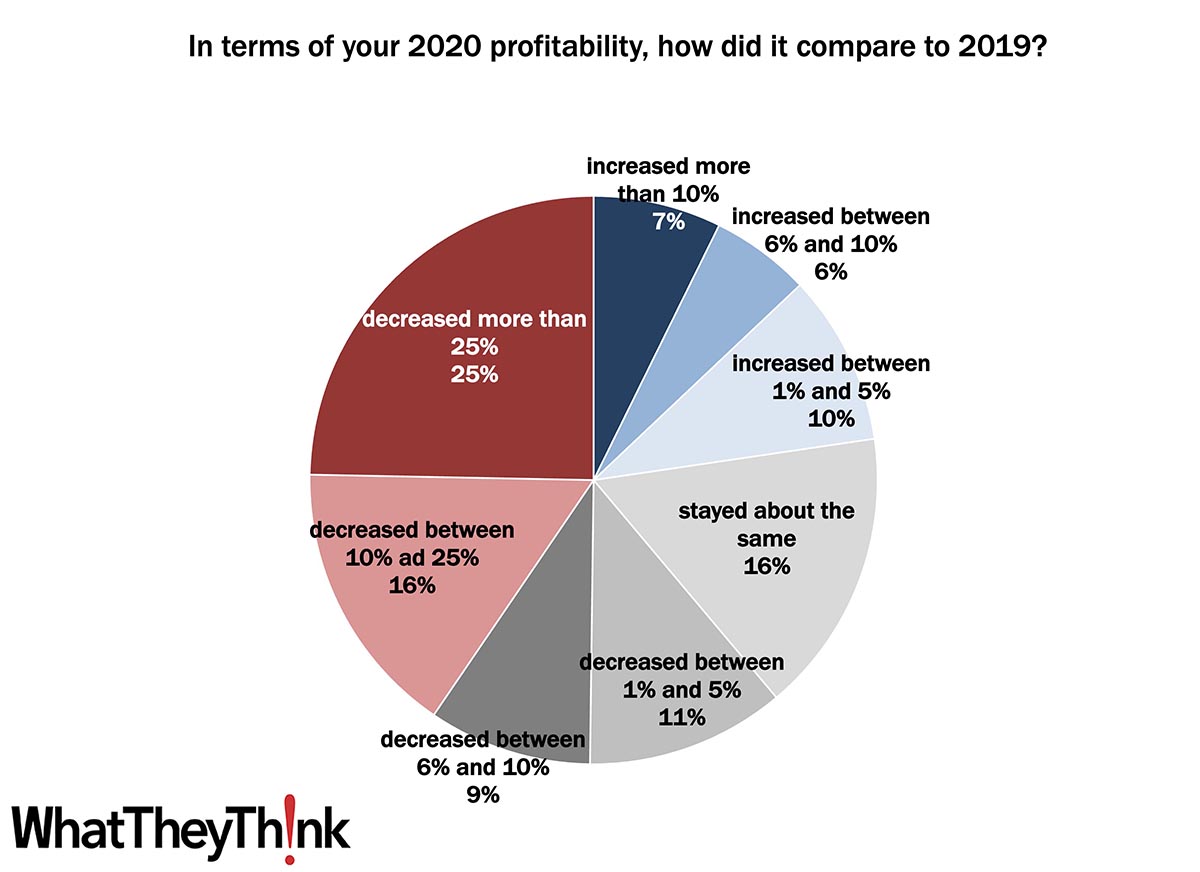

Printing 2021 Quick Look: 2020 Profits

Published: April 7, 2021

According to data from our recently published Printing Outlook 2021 special report, print businesses reported a -9.1% decline in profits from 2019 to 2020. Full Analysis

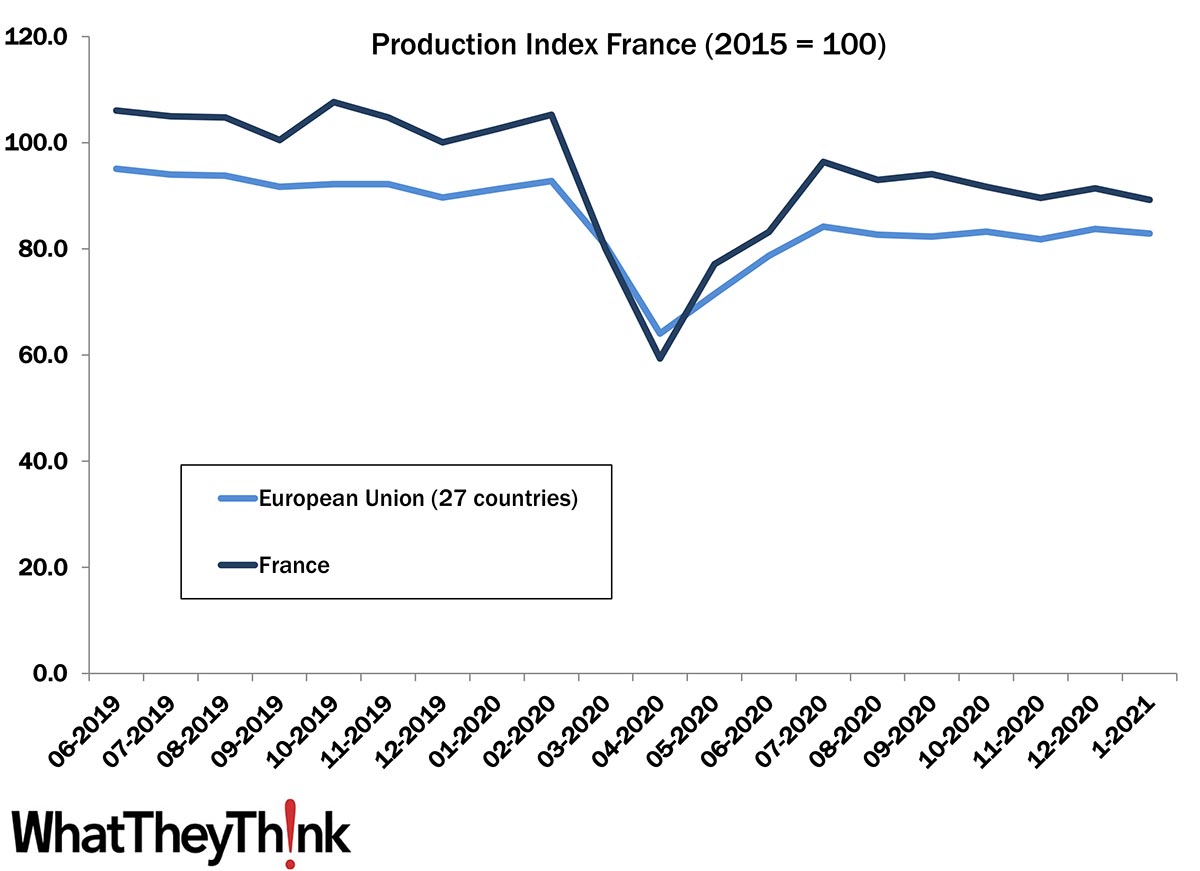

European Print Industry Snapshot: France

Published: April 5, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in France. Full Analysis

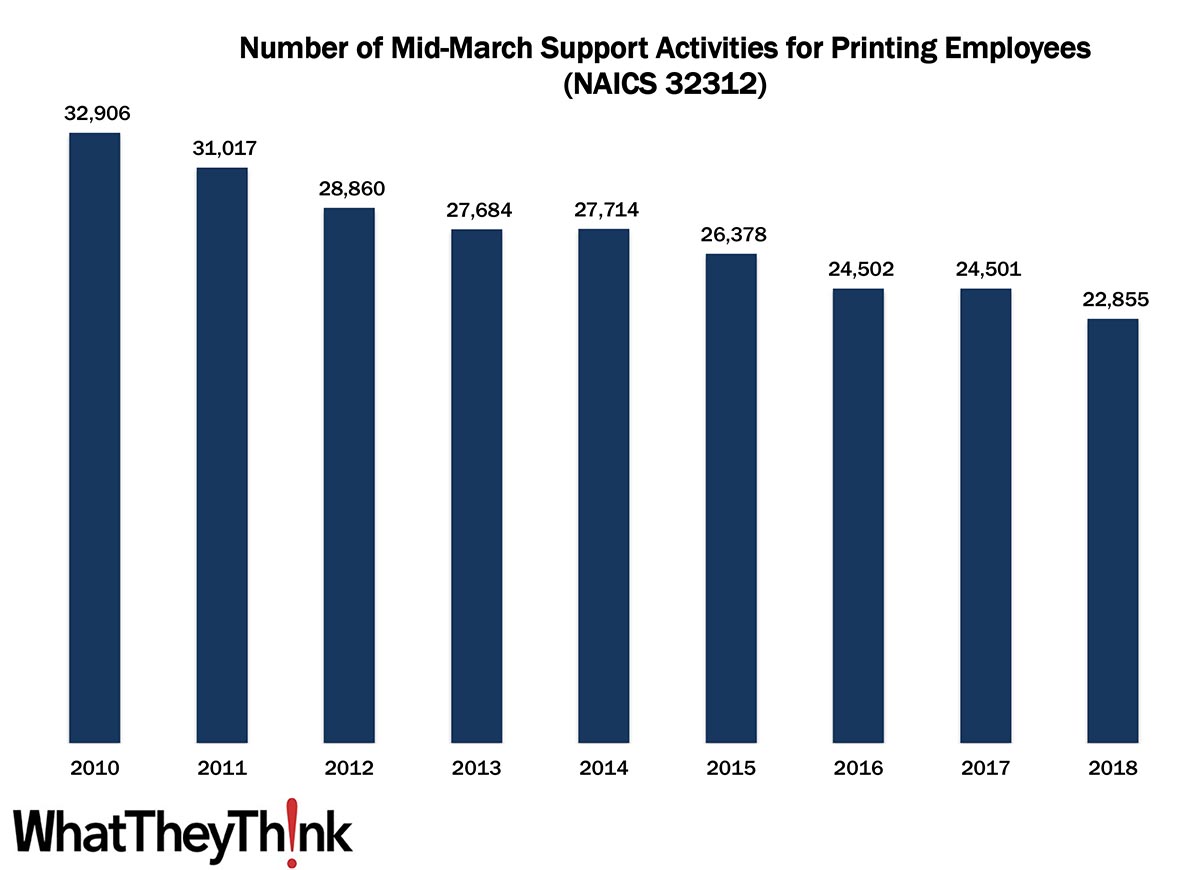

Pre- and Postpress Employees—2010–2018

Published: March 26, 2021

According to County Business Patterns, in 2010, there were 32,906 employees in NAICS 32312 (Support Activities for Printing). By 2018, employees had declined to 22,855. In macro news, Q4 2020 GDP was revised up. Full Analysis

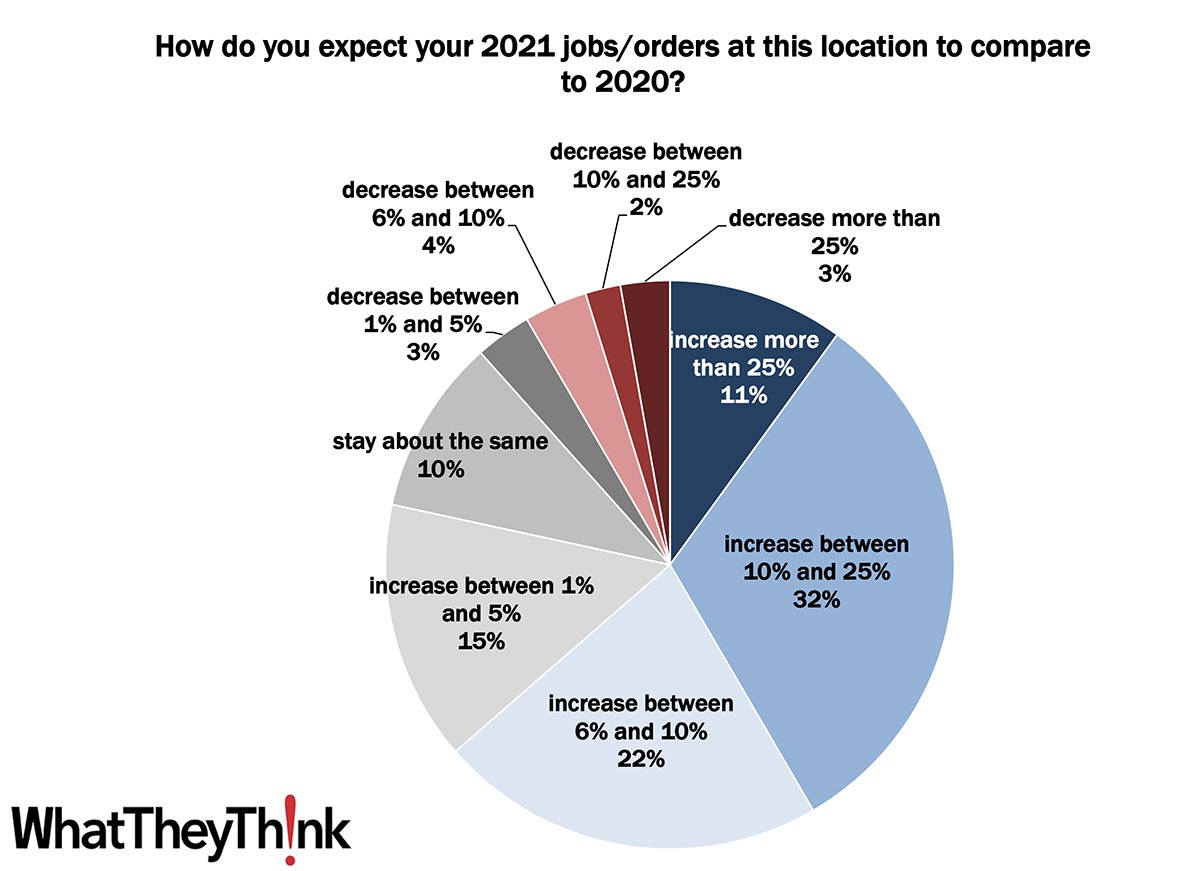

Printing 2021 Quick Look: Anticipated 2021 Jobs/Orders

Published: March 24, 2021

According to data from our recently published Printing Outlook 2021 special report, print businesses expect print industry jobs/orders to rebound +9.0% from 2020 to 2021. Full Analysis

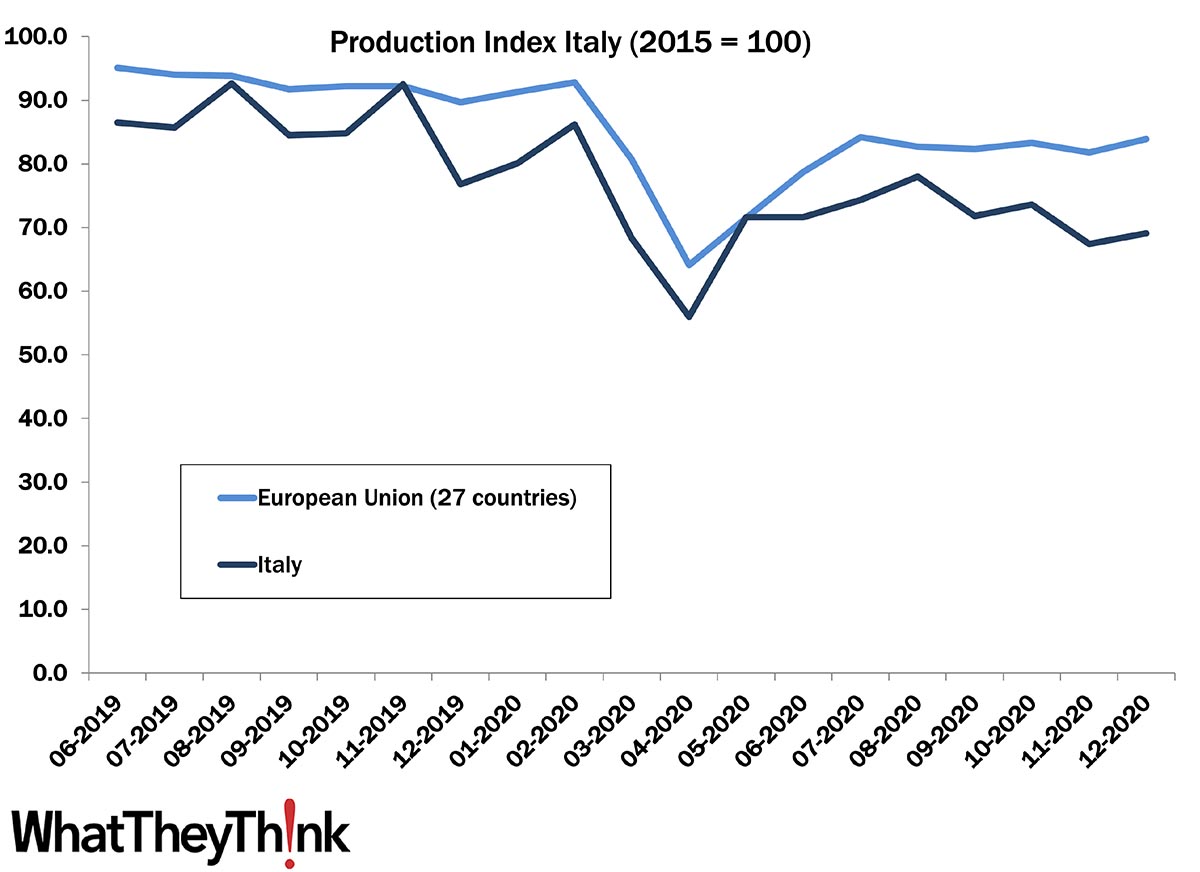

European Print Industry Snapshot: Italy

Published: March 23, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Italy. Full Analysis

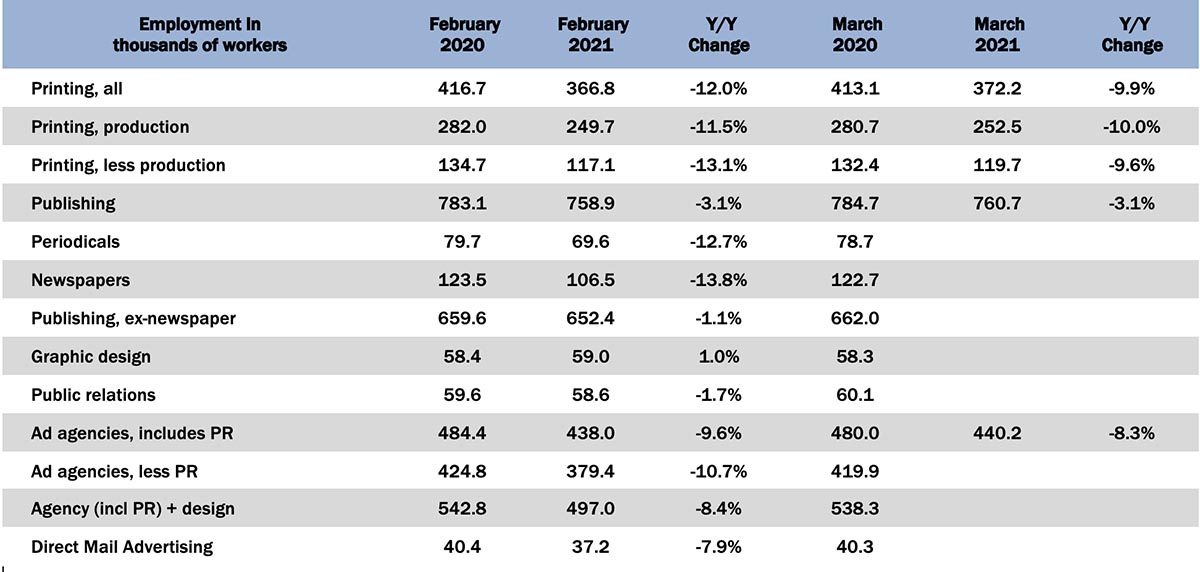

Graphic Arts Employment—February 2021

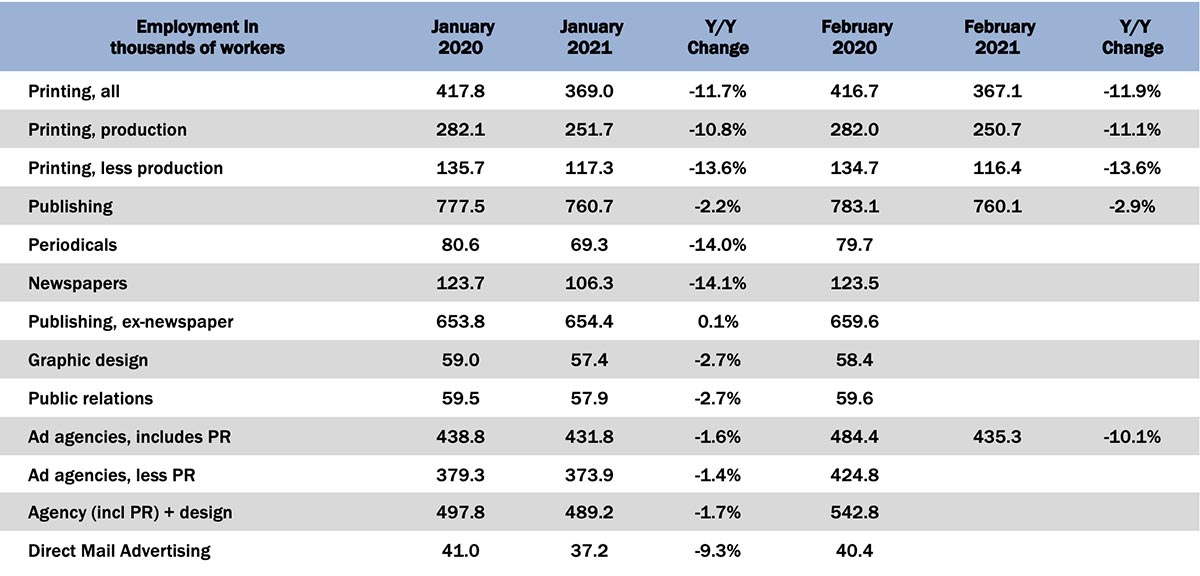

Published: March 19, 2021

In February 2021, all printing employment is down -0.5% from January, production employment down -0.4%, and non-production printing employment down -0.8%. Full Analysis

Printing 2021 Quick Look: 2020 Jobs/Orders

Published: March 17, 2021

According to data from our recently published Printing Outlook 2021 special report, the average number of jobs decreased -10.8% from 2019 to 2020. Full Analysis

Book Printing Employees—2010–2018

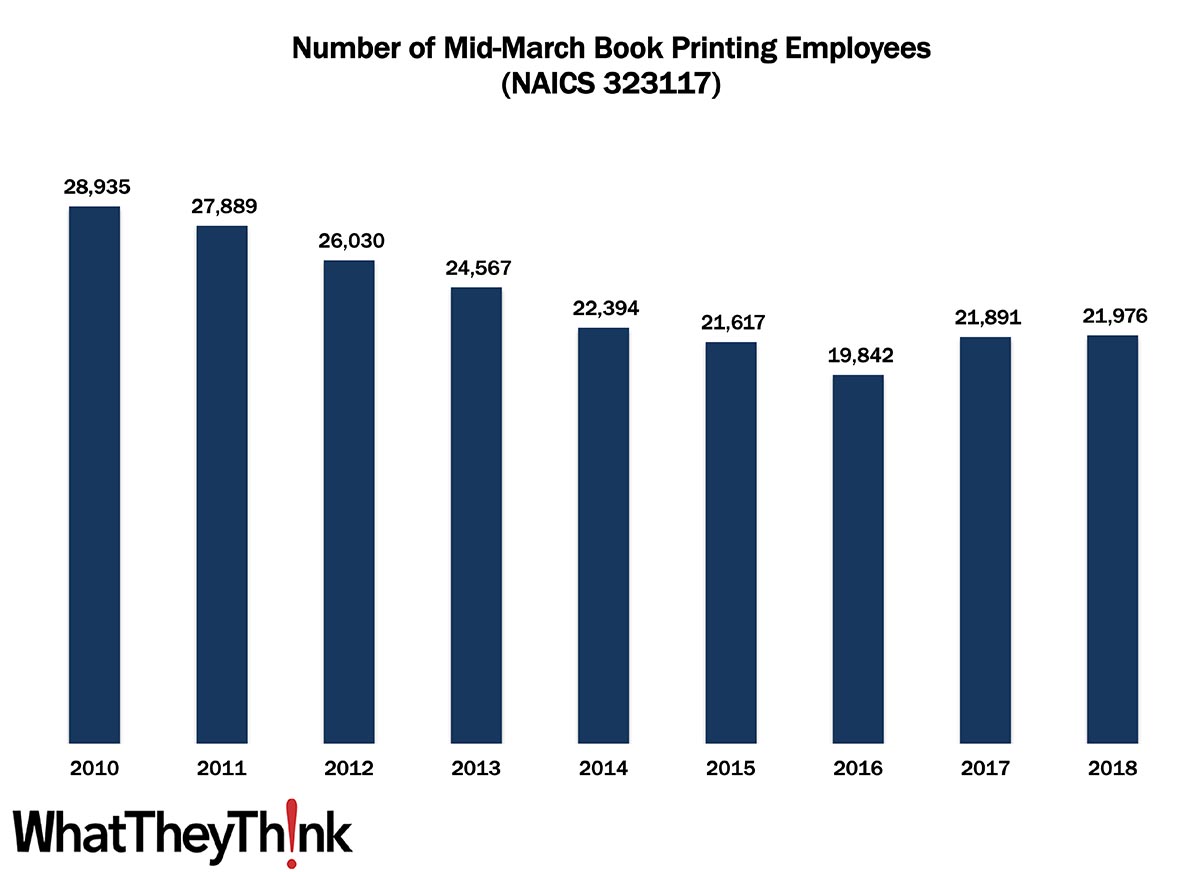

Published: March 12, 2021

According to County Business Patterns, in 2010, there were 28,935 employees in NAICS 323117 (Book Printing Establishments). By 2018, employees had declined to 21,976. In macro news, inflation was soft in February. Full Analysis

Printing 2021 Quick Look: Anticipated 2021 Revenues

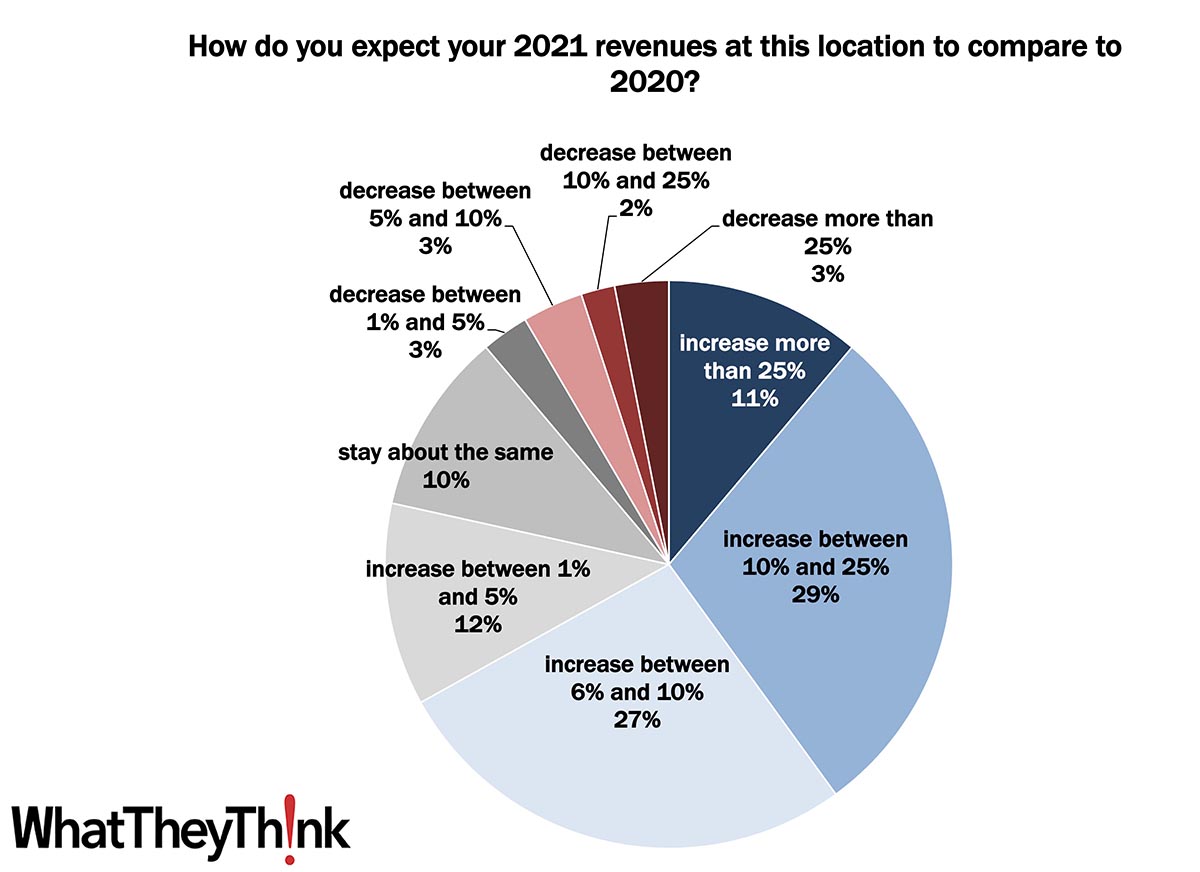

Published: March 10, 2021

According to data from our recently published Printing Outlook 2021 special report, print businesses expect print industry revenues to rebound +9.1% from 2020 to 2021. Full Analysis

January Printing Shipments—They Can Only Get Better from Here

Published: March 5, 2021

We kicked off 2021 inauspiciously with January printing shipments coming in at $6.61 billion, down from 2020’s $7.17 billion. It's the worst January in at least the last five years, but already things are boding well for the rest of 2021. Full Analysis

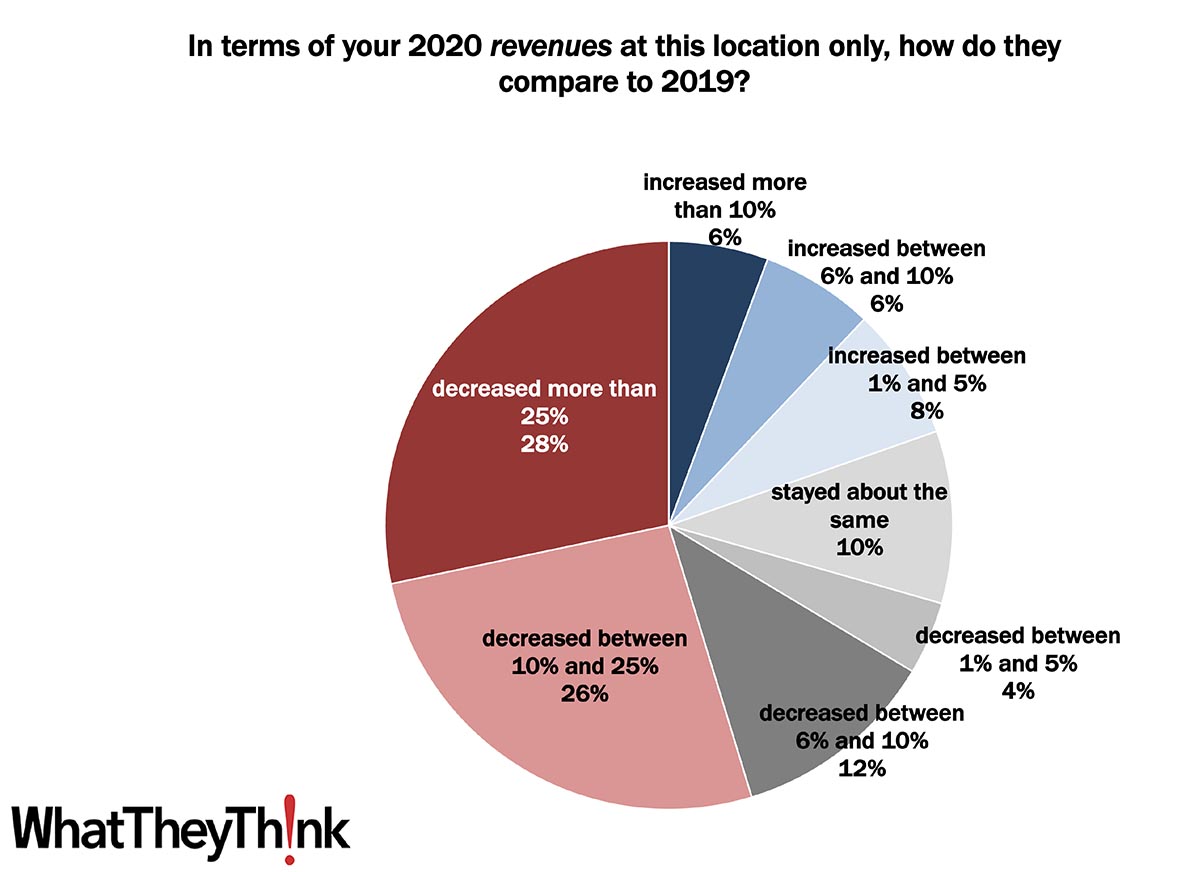

Printing Outlook 2021 Quick Look: 2020 Revenues

Published: March 3, 2021

According to data from our recently published Printing Outlook 2021 special report, print industry revenues dropped -12.6% from 2019 to 2020, compared to +4.1% from 2018 to 2019. Full Analysis

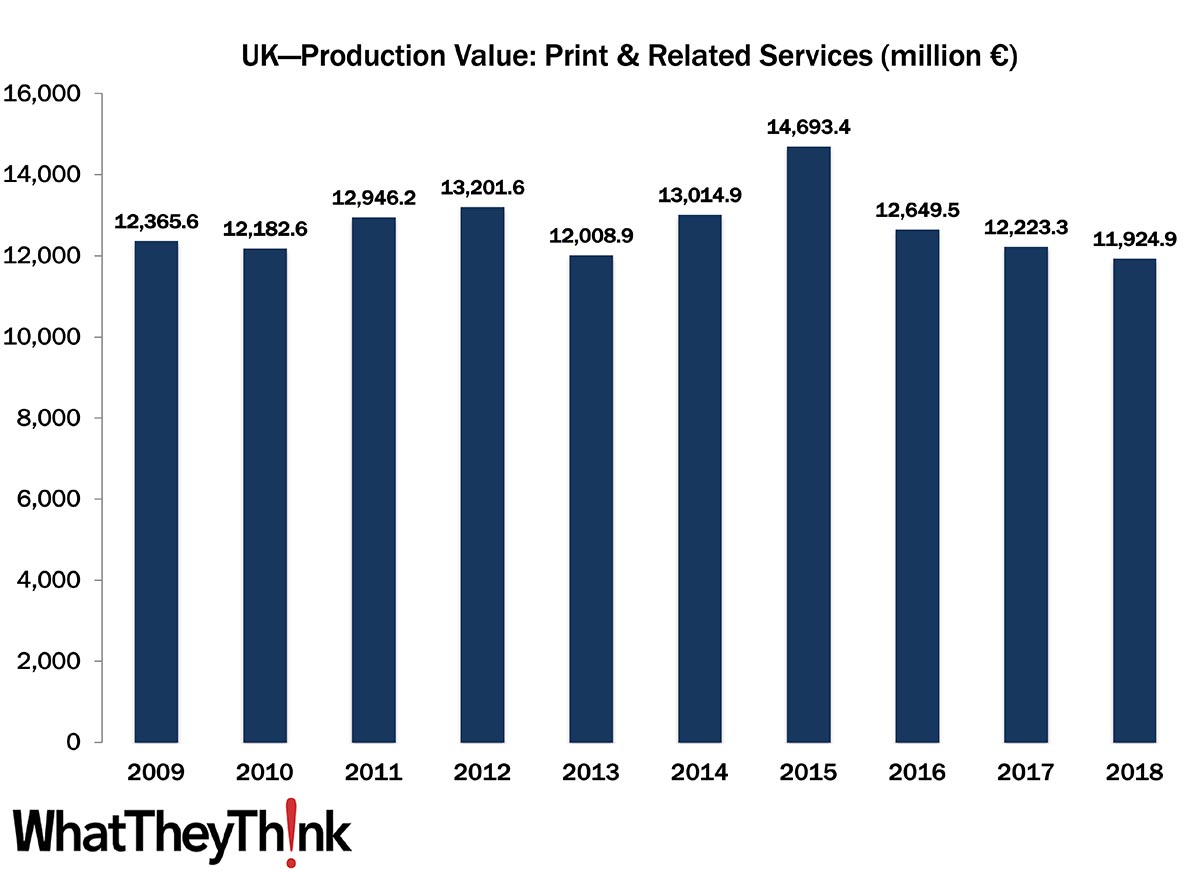

European Print Industry Snapshot: United Kingdom

Published: March 2, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in the United Kingdom. Full Analysis

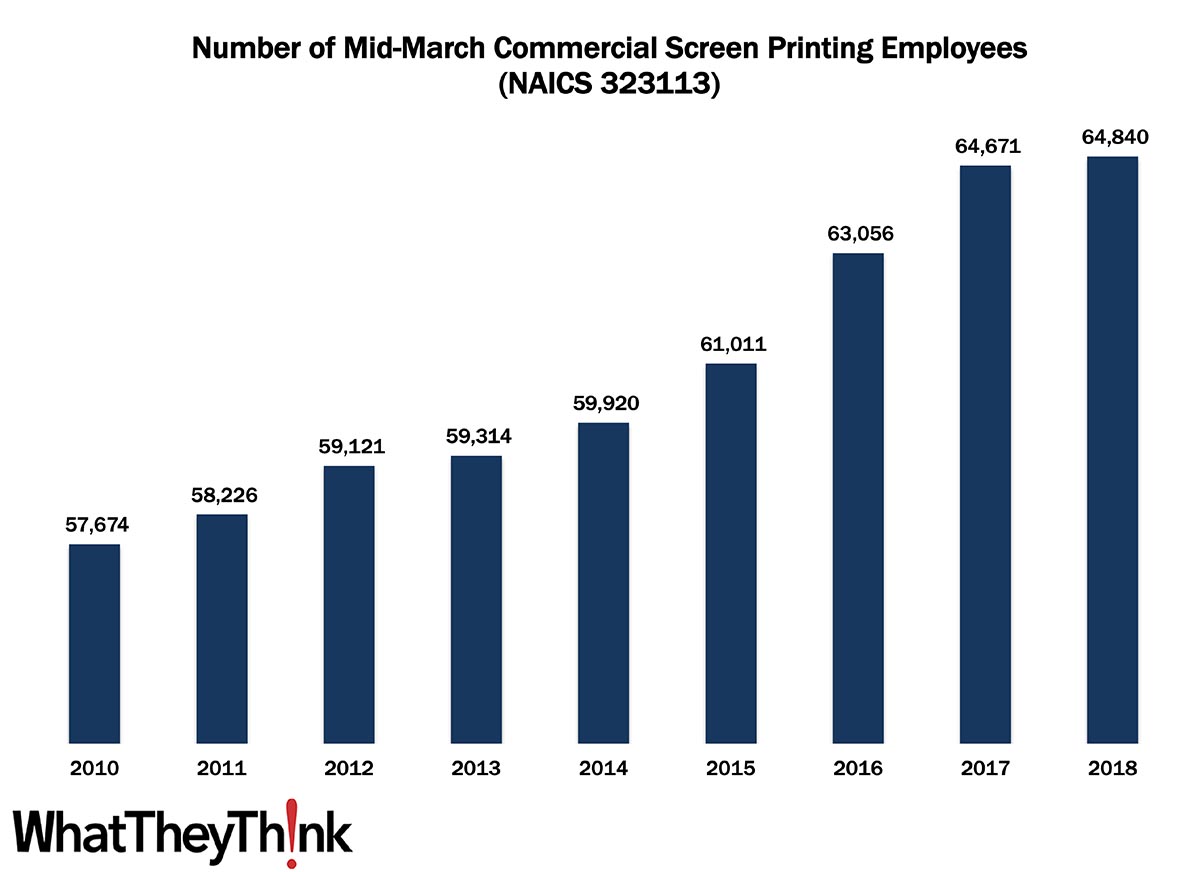

Commercial Screen Printing Employees—2010–2018

Published: February 26, 2021

In 2010, there were 57,674 employees working in US screen printing establishments (NAICS 323113). By 2018, that number had increased +12.4% to 64,840. In macro news, seven “recovery indicators” for parts of the economy most acutely impacted by the pandemic. Full Analysis

December Printing Shipments—One Last Unexpected Twist for 2020

Published: February 19, 2021

In December 2020, in one last, end-of-the-year rally, printing shipments grew from $7.0 billion to $7.17 billion. Full Analysis

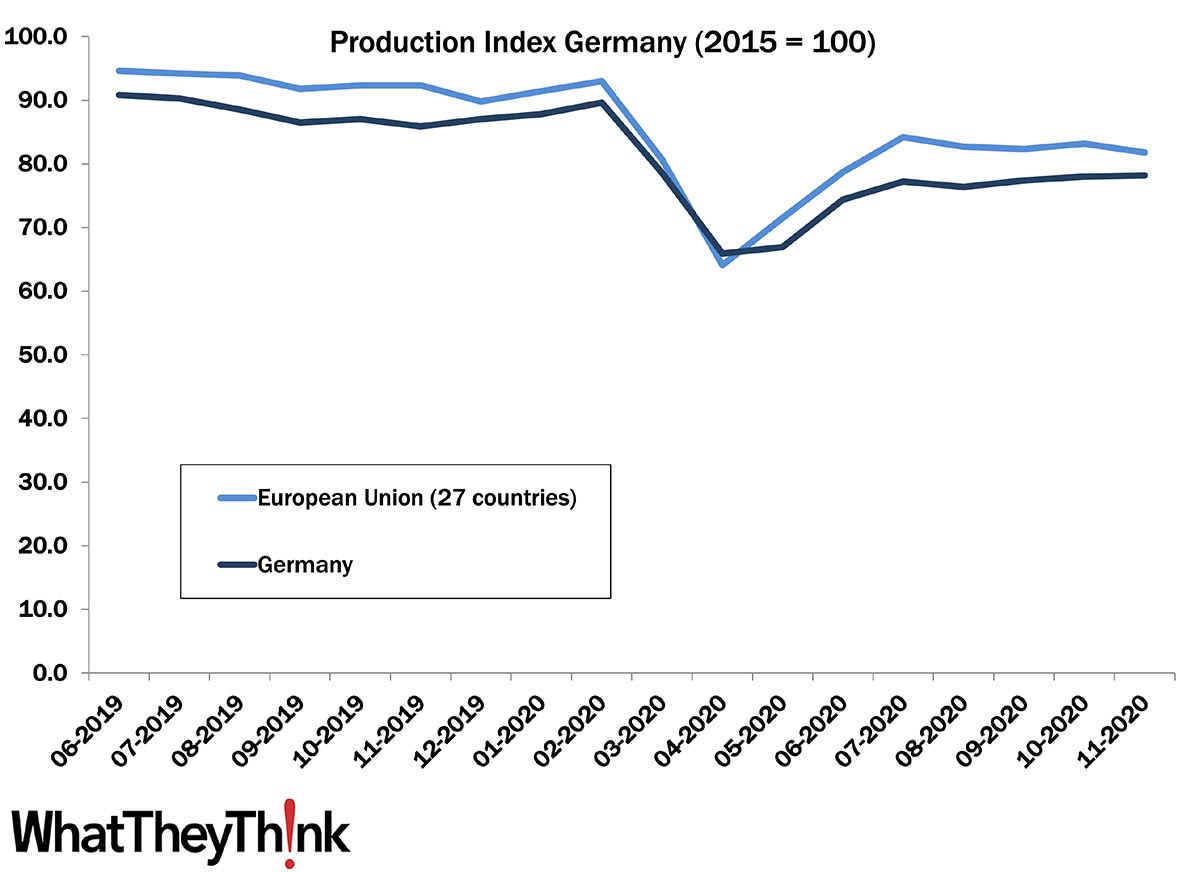

European Print Industry Snapshot: Germany

Published: February 15, 2021

In this bimonthly series, WhatTheyThink is presenting the state of the printing industry in different European countries based on the latest monthly production numbers. This week, we take a look at the printing industry in Germany. Full Analysis

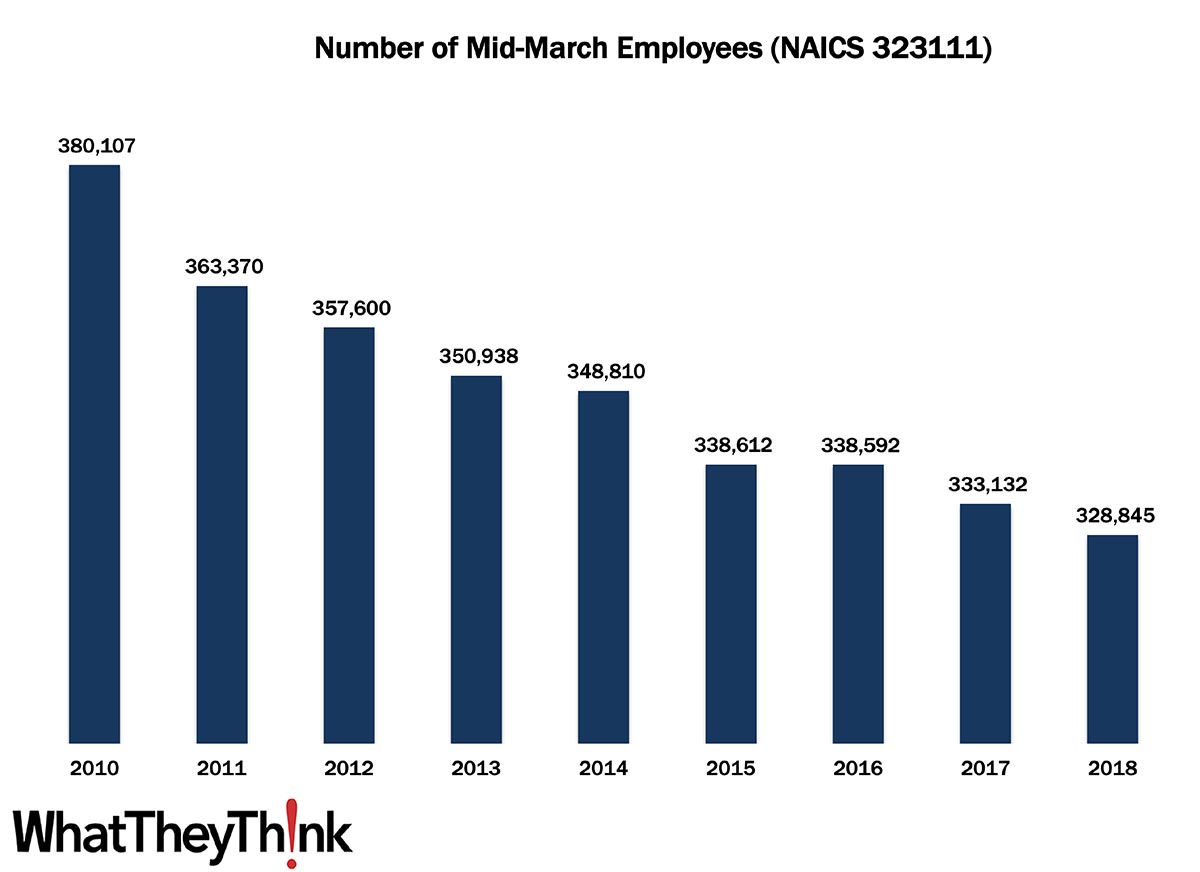

Commercial Printing Employees (Less Screen and Books)—2010–2018

Published: February 12, 2021

In 2010, there were 380,107 employees working in US establishments in NAICS 323111 (Commercial Printing–Except Screen and Books). By 2018, that number had declined -13.5% to 328,845. In macro news, the Consumer Price Index (CPI) increased 0.3% in January, or 1.4% over the last 12 months. Full Analysis

![]()

- KYOCERA NIXKA INKJET SYSTEMS (KNIS) INTRODUCES BELHARRA, THE NEW WAVE OF PHOTO PRINTERS

- New RISO Printing Unit Offers Easy Integration for Package Printing

- March 2024 Inkjet Installation Roundup

- Inkjet Integrator Profiles: Integrity Industrial Inkjet

- Revisiting the Samba printhead

- 2024 Inkjet Shopping Guide for Folding Carton Presses

- The Future of AI In Packaging

- Inkjet Integrator Profiles: DJM

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.