By Jon Harper Smith

The inkjet printing industry is in one of its most consequential periods of transformation, with the graphic and packaging market now valued at over $101 billion and output growing at nearly 9.4% CAGR. To make sense of what is driving that growth and where the market is heading, Smithers analyst Jon Harper Smith—author of the newly published report The Future of Inkjet Printing to 2031 and a print industry veteran with more than 40 years of experience—sets out the forces reshaping the competitive landscape.

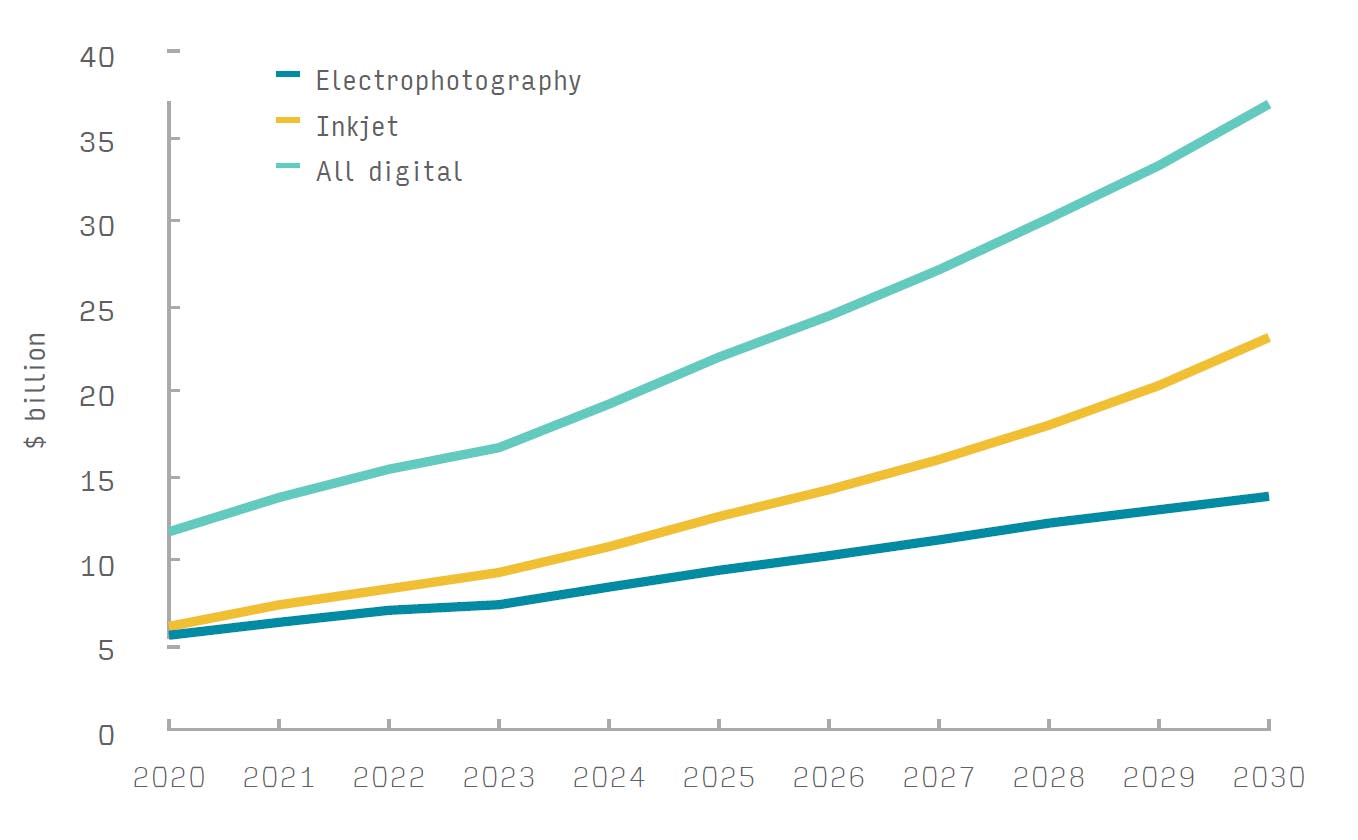

The numbers alone tell a striking story. The graphic and packaging inkjet market is now valued at over $101 billion, with output growing at nearly 9.4% CAGR. The functional and industrial side is smaller at around $29 billion, but by 2031 the graphic and packaging segment alone is forecast to reach $134 billion.

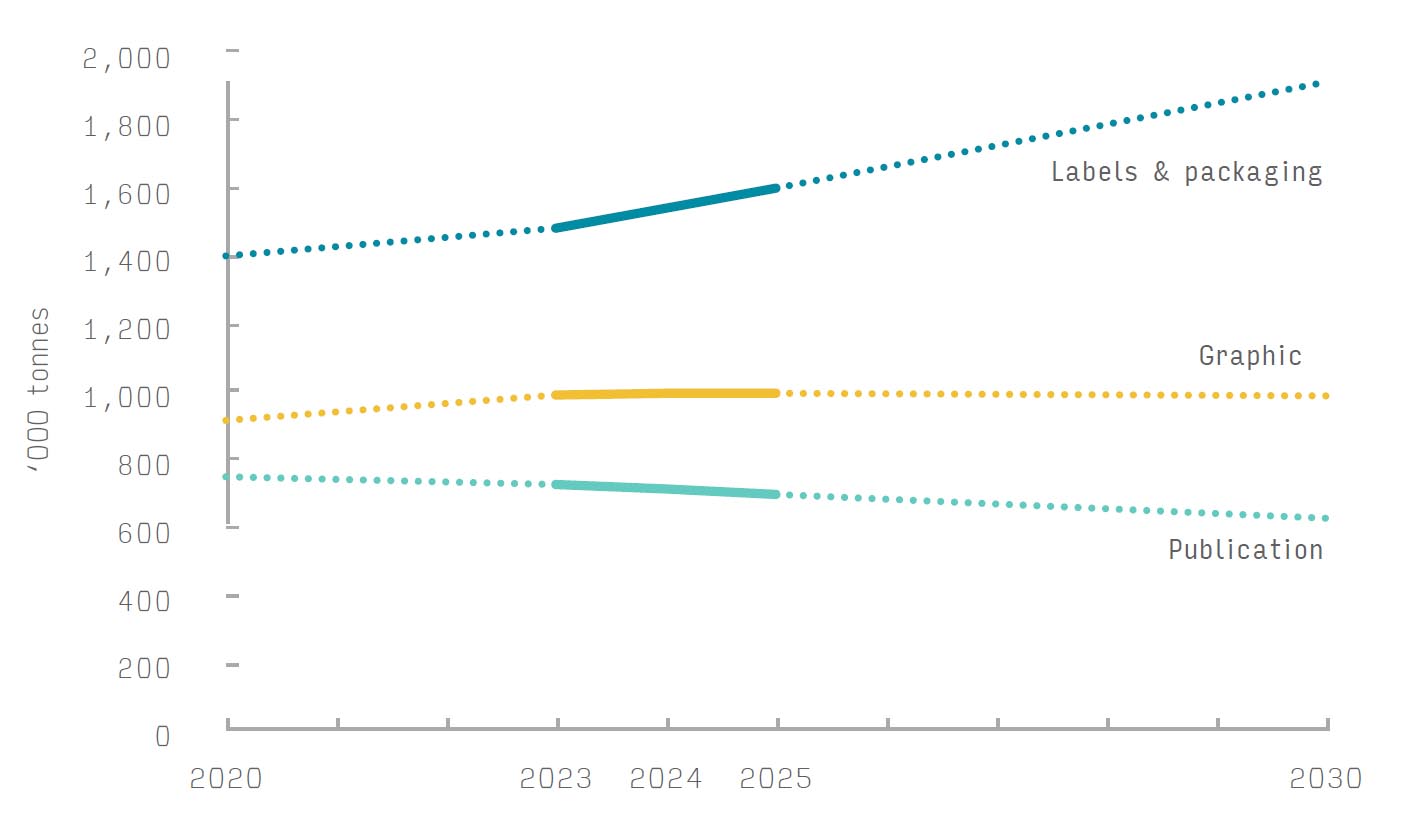

Several forces are converging to produce that growth. Covid proved to be a more significant catalyst than many appreciate even now, accelerating the shift away from physical print in publication, pushing consumers online, and giving e-commerce an enormous boost. Web-to-print portals took off as people started buying custom printed products from home. Packaging and labels, meanwhile, proved remarkably resilient throughout the disruption because those are essential goods. People still need things wrapped and labelled regardless of what is happening in the world.

Sustainability has become another significant driver. Print-on-demand is a powerful tool for managing inventory and reducing overproduction, which matters enormously in packaging markets. Regulations are pushing the packaging sector towards recyclable and recycled materials, and textiles are coming under increasing scrutiny too. Water-based inks are central to this shift, becoming far more common because of their sustainability credentials, their safe handling properties, and their suitability where food migration is a concern.

The ink market itself is worth nearly $10 billion in 2026 and is forecast to grow to $13.3 billion by 2031, with volumes reaching over 315,000 tonnes. Beyond the headline numbers, a notable technical shift is under way. The move towards water-based inks is spreading across more segments, while the transition from UV to LED UV in radiation-cured inks has been gathering real pace. Solvent-based inks are in decline, and that trend is expected only to continue.

On the hardware side, the picture is more nuanced. Fewer presses are actually being sold each year, but their productivity is so much higher that the overall value of the market is still growing at around 3.4% CAGR. One of the most significant shifts is a move towards machines designed and optimised for very specific applications rather than general-purpose devices. Manufacturers are carefully balancing print quality, productivity, and cost for particular market niches, producing results that Harper Smith describes as genuinely impressive.

In wide format graphics, for instance, multiple older and slower machines are being replaced by fewer but far higher-output printers. Single-pass printing is delivering exceptional productivity in segments like corrugated pre-print, cartons, labels, flexible packaging, and textiles. The installed base has not entirely caught up yet, but it is moving in that direction.

A parallel strategic development is the trend of manufacturers developing their own print heads. HP, Epson, Konica Minolta, Ricoh, Kodak, Domino under Brother, and now Canon are all in that camp. Controlling your own print head technology confers a real competitive advantage, and Harper Smith expects the trend to continue.

Artificial intelligence is playing a more positive role than some in the industry feared. Generative AI is being used to create unique imagery, with obvious appeal in a market where personalisation matters. More practically, AI is having a significant impact on workflow and print management software. Looking ahead to 2031, AI-driven diagnostics and preventative maintenance are expected to become commonplace, helping keep presses running and quality consistent. That combination of reliability and inline inspection systems, Harper Smith argues, will be quite transformative for total cost of ownership.

Total cost of ownership remains a sticking point for inkjet, at least for now. Variable costs are still significantly higher than most analogue processes, driven by high ink costs, and the pace of technology evolution has meant presses are superseded relatively quickly, affecting depreciation and leasing decisions. But the direction of travel is positive. By 2031, ink costs are expected to have come down relative to analogue alternatives, replacement cycles to have lengthened, and higher productivity to be driving down cost per job. The gap will not close entirely, but it is narrowing.

Geographically, the headline story is Asia. North America was the largest market in 2021, but Asia Pacific draws level in volume by 2026, and by 2031 it will be the largest region by every measure. China and India are the powerhouses, with China set to overtake North America as the single largest country market. It is not just consumption: Asian manufacturers are producing more of the hardware and inks, creating real competitive pressure on Western developers. After forty years in the industry, Harper Smith regards the rise of Asia in inkjet as one of the most consequential shifts he has seen. China and India, he says, are markets no one in this business can afford to ignore.

Jon Harper Smith is a print consultant and analyst at Smithers with over 40 years of industry experience spanning inkjet, ink chemistry, business strategy, and market analysis. This article draws on his market report The Future of Inkjet Printing to 2031, published by Smithers.