Mainstream applications for screen printing have a weak outlook, but the technology will continue to be profitable for functional and industrial applications, such as electronics, promotional items, and apparel, according to new forecasting from Smithers.

Data from its new report, The Future of Screen vs Digital Printing to 2030, show that in 2025, revenue for screen print for graphics and packaging will be just $9.37 billion.

Screen in Graphics in Packaging

In short-run point-of-sale, display and signage work screen use has now largely been by wide-format inkjet. It remains in use for jobs requiring heavy varnishes or coatings, including for high-embellishment labels and packaging. As a consequence, most of the limited R&D work for this technology is directed on coatings and inks, rather than machinery.

As with other analog print systems, there are moves to increase automation and reduce energy consumption, and there has been some investigation of digital screen exposure, relying either on the exposure of photosensitive emulsions; or using an inkjet module to print an opaque positive image onto the screen.

These efforts have been constrained however by the small number of manufacturers invested in high-end screen printing, declining sales for new machines and increased technical competition.

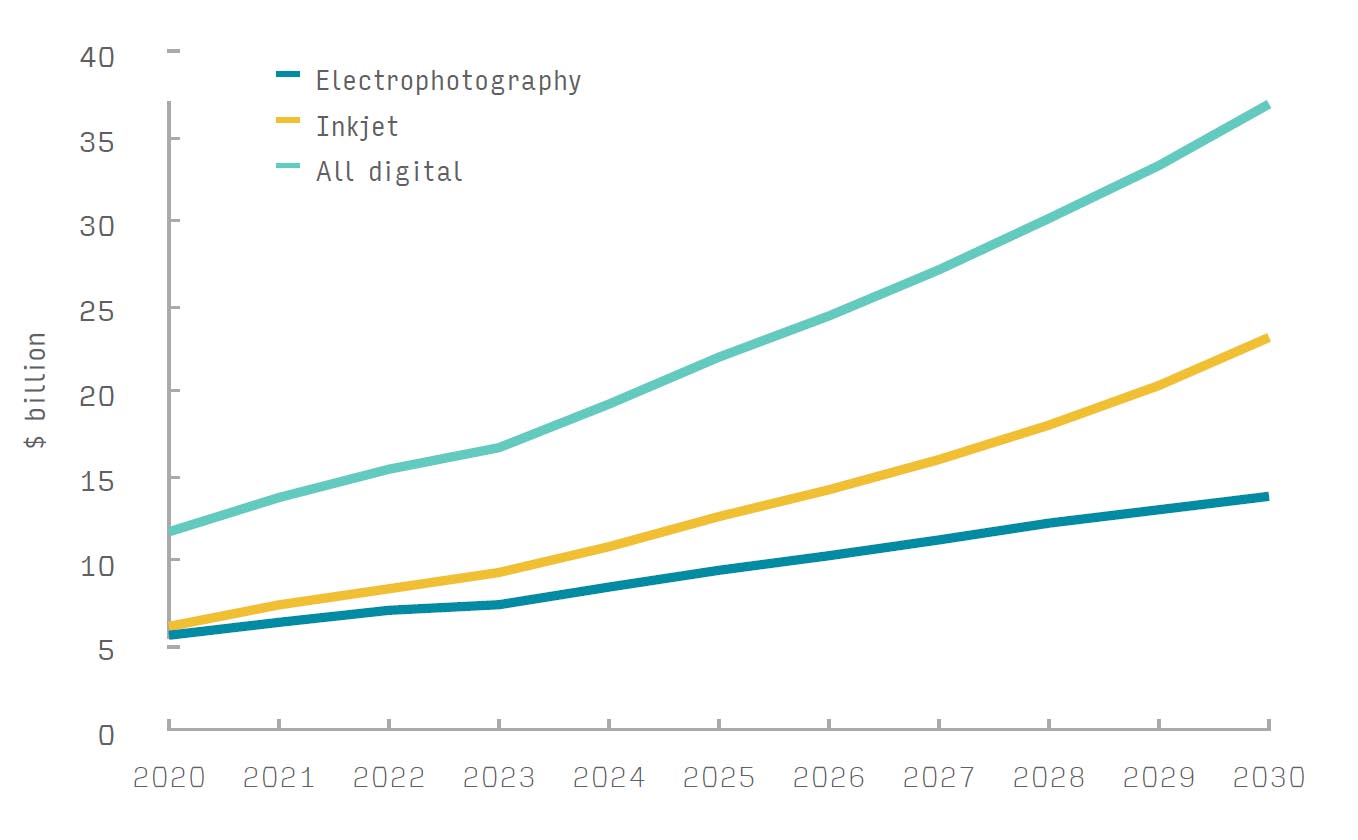

Technical innovation will have only a marginal effect on the conventional graphics market, where screen print will soon be challenged further by a new generation of specialist printheads built to jet drops of 50pl and bigger. Overall this will see demand for screen in conventional applications decline, down to $8.12 billion in 2030 at constant pricing. In contrast, across the same period inkjet and toner printing in graphics, packaging and labels work will steadily increase. Reaching a projected $166.9 billion in 2025, sales will top $200 billion in 2030 for the first time.

Screen Printing for Textiles and Electronics

These data do not include functional and industrial print, a distinct, lucrative sector of the market where demand for the versatility screen offers—depositing inks and specialty fluids onto a wide range of non-paper substrates, and printing high-quality images onto uneven or shaped surfaces—remains healthy.

Screen printing is the dominant technology for textiles with very high volumes of roll fabric printed on high-speed rotary printing lines with dye- or pigment-based inks. Smaller screen lines are widely used to print T-shirts, transfers, sportswear, workwear, bags, and accessories, which benefit from the high durability of screen-printed images. Smithers data show that in 2025, textiles and promotional item prints with screen will be worth $16.82 billion, and grow to $20.19 billion in 2030.

While this is high volume work, it is far from the most lucrative use for screen print; instead, that is in printed electronics, where metallic inks are employed to produce circuit boards, RFID tags, visual display units (VDUs), membrane switches, and touchscreens. Screen is preferred here because it can deposit high film weights and precisely metered layers of varying thickness to build up circuitry, with high reliability and excellent resolution.

Generating a projected $31.18 billion in revenue worldwide in 2025, printed electronics will also be the fastest growing application for screen in functional and industrial work across the rest of the forecast period.

Inkjet for Functional and Industrial Markets

Large percentages of R&D spending for conventional graphics and packaging print are focussed on digital, inkjet in particular. This is equally the case in functional and industrial print segments as it can deliver greater precision, control, and low cost for short runs. In response, manufacturers are developing a new generation of printheads capable of jetting very high viscosity specialty inks and coatings, with the latest Xaar printheads able to deposit coatings of up to 240gsm in high laydown mode.

For inkjet this is opening a wide variety of new applications. In 2025, value from functional and industrial work for inkjet $30.39 billion, about half the value of screen. It has grown at a rate of +9.7% year-on-year since 2020. Its main application by volume remains in ceramics, a segment inkjet has revolutionized due to the production efficiencies it offers—printing complex designs on lighter weight tiles, with far fewer breakages.

As with screen, the cost variables make printed electronics the most valuable application for inkjet, and one that will continue to grow revenue rapidly, alongside developing opportunities in the biomedical and automotive industries. Across the segment the precise droplet placement in inkjet offered is an advantage, and as a non-contact process it has become the preferred option for some VDU and solar panel production.

Simultaneously, inkjet continues to replace screen in all textile printing formats, from desktop t-shirts machines through to high volume roll-to-roll fabric printers over 5m wide. It is also gaining market share in décor print, where wide-format inkjet machines are superseding gravure to produce customized surface decorations on furniture and cabinetry.

The market and technology outlook in these two distinct print sectors is examined in detail in The Future of Screen vs Digital Printing to 2030. Available to purchase now from Smithers, this includes a comprehensive dataset presented in over 250 tables and figures, segmenting the global market by print process, end-use application, and geographic region.

John Nelson is an award-winning editor and journalist working in the market reports and consultancy business of Smithers. Here he covers market and technology developments across multiple technical and commercial segments; including home and personal care, sustainability, packaging, printing, paper, nonwovens, rubber, and tires.