By John Nelson

Developing inkjet equipment for various packaging segments is a top goal for many of the print OEMs, with even established analog manufacturers, such as Heidelberg, joining the movement. The advantages of digital print in packaging conversion are increasingly being appreciated and have been demonstrated in label print where both inkjet and toner have an established footprint.

The latest expert study from Smithers—The Future of Digital Print for Packaging to 2030—shows that in 2025 there are over 8,100 narrow-web digital presses in operation around the world, and that almost 1,150 new digital label presses will be sold. These will print around 103 billion A4 prints of labels in 2025, split equally between inkjet and toner. This has a value of $11.01 billion; giving digital an 23.3% share of the label segment by value.

Penetration into other segments has been slower. The total packaging and labels print segment is now worth $537.1 billion, and overall digital accounts for just 4.1% of value ($22.0 billion) and 1.3% of packaging volume. This means there is still room for digital to expand into printing corrugated, folding carton, flexible, and rigid plastic packaging—offering greater customization, faster turnaround, and less wastage—with a print quality that increasingly matches those of established analog systems.

As the market moves beyond these narrow-web presses, a number of outstanding issues are inhibiting the further adoption of digital.

Finishing and Automation

Converters need presses that fit in with their existing finishing machinery and workflows. This favored the initial adoption of digital in labels, with roll-to-roll narrow-web presses, running at relatively slow speeds, they converted using existing narrow-web finishing systems. Although as press speeds have increased up to 100 meters per minute (mpm), label converters have begun a move towards integrated or near-line finishing.

In other packaging applications there is still a mismatch between press and finishing line speed. In cartons, the Landa S11 runs at 11,200 sheets per hour (sph) while the Agfa Speedset is 11,000 sph, meaning a converter can print 20 runs of 500 sheets in an hour, with practically no makeready. To convert this output into finished cartons, an analog finishing line needs to prepare 50 dies, and perform 50 set-ups on a cutting and creasing machine, and a folder gluer. Even with increased automation, finishing equipment set-up times are still significant, making it much harder to realize the full potential of this new generation of high-throughput presses.

Simultaneously, offset litho and flexo OEMs are using automation, such as robotic plate loading, to reduce their set-up and makeready times—eroding a key advantage of digital production. And extended gamut process printing continues to proliferate, meaning an analog printer can ditch spot colors and handle fewer time-consuming ink changes.

Brand and Retailer Priorities

Analog printed packaging supply chains have developed over many years to satisfy demands of buying organizations, and there are potential risks for them in making a change to digital print.

A leading concern is the ability for a digital press to match brand colors accurately. In some cases this stops brand managers from using digital, although the rise of the hybrid inkjet/flexo press lines means that such colors, and metallics, may be reproduced accurately.

Modern retail is not about individual brands, but complex supply chains both within companies and among partners. To switch to digital print, stakeholders at multiple levels have to agree, and there may be downsides with additional costs and pressures in individual departments. Conversely it is easier for the smaller, start-up brands to make these decisions and implement a campaign exploiting the full potential of digital.

Safety Considerations

Food and beverages are leading applications for printed packaging, accounting for around three quarters of consumer formats. Such packaging, including any inks or coatings employed, requires regulatory approval before they can be used, to prove they will not transfer toxic substances into the foodstuff, or affect its composition or taste. This can be time-consuming and expensive, because the bulk of toners and inkjet inks for packaging are bespoke formulations for specific machines, usually sold by the OEM itself. There is now extra pressure to also develop packaging that prioritizes the recovery of high-quality materials in recycling, requiring consumables that can easily be removed during standard waste processing.

Safety considerations have restrained the wider use of inkjet in flexible packaging print, a natural extension for many converters already operating larger narrow-web presses.

For lightweight polymer substates water-based printing is preferred because of the thin ink film it deposits, while prior issues mean there is still skepticism over the safety of UV-curing inks. This ink has to adhere to wide range of substrates, dry effectively and then accept other processes including functional coating and lamination. For inkjet, these Chemstack properties are difficult to achieve because most of the coating and adhesives now available were developed to work with solvent-based flexo and gravure inks—giving toner a slight advantage in this segment, for now.

The Future of Digital Print for Packaging to 2030 is available to purchase now. Its in-depth technical and market analysis is quantified in an exclusive data set—presented in over 350 tables and figures—segmenting the market by print process, packaging /label type, geographic region, and leading national market.

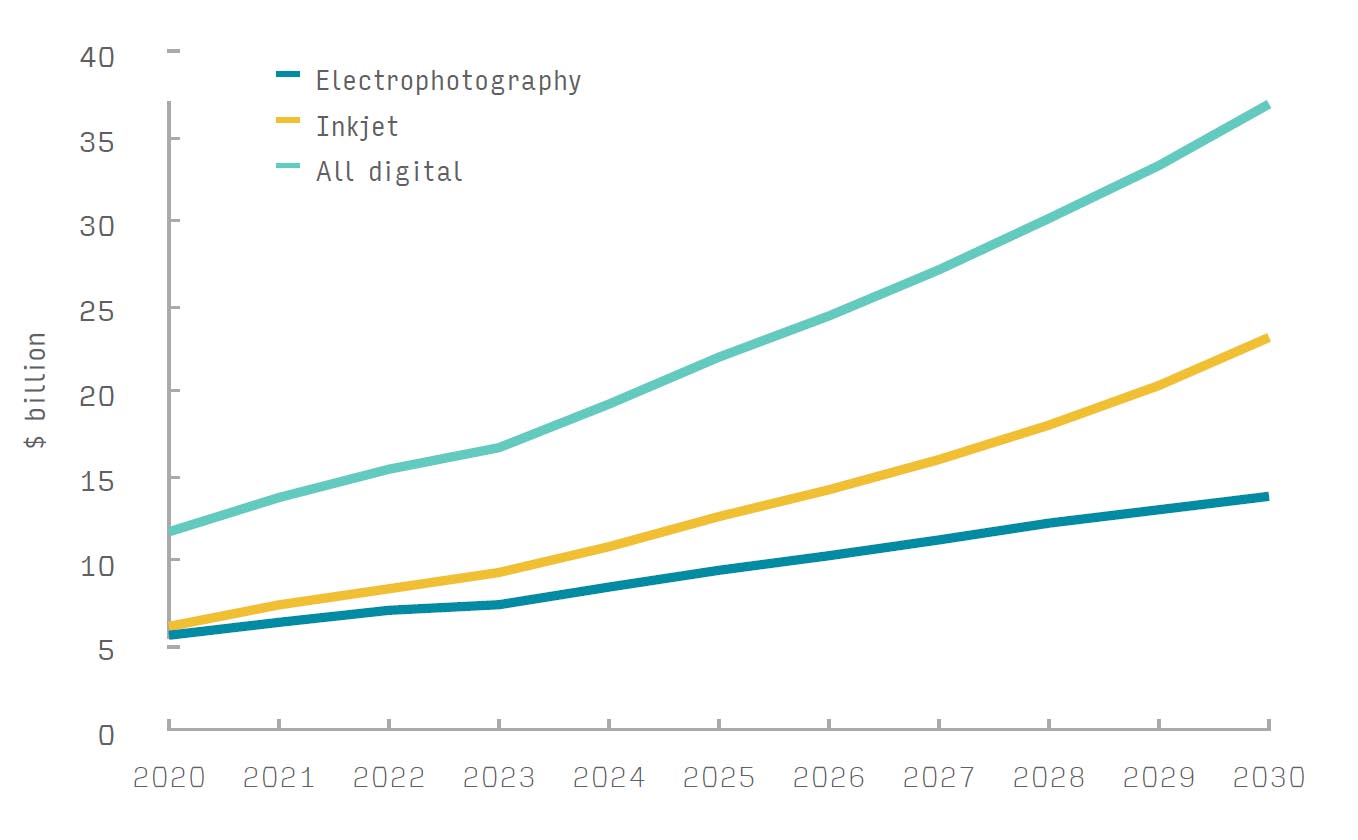

Figure 1: Global digital package and label printing value by electrophotography and inkjet, 2020–30 ($ billion, constant 2023 values)

Source: Smithers

John Nelson is an award-winning editor and journalist working in the market reports and consultancy business of Smithers. Here he covers market and technology developments across multiple technical and commercial segments; including home and personal care, sustainability, packaging, printing, paper, nonwovens, rubber, and tires.