By John Nelson

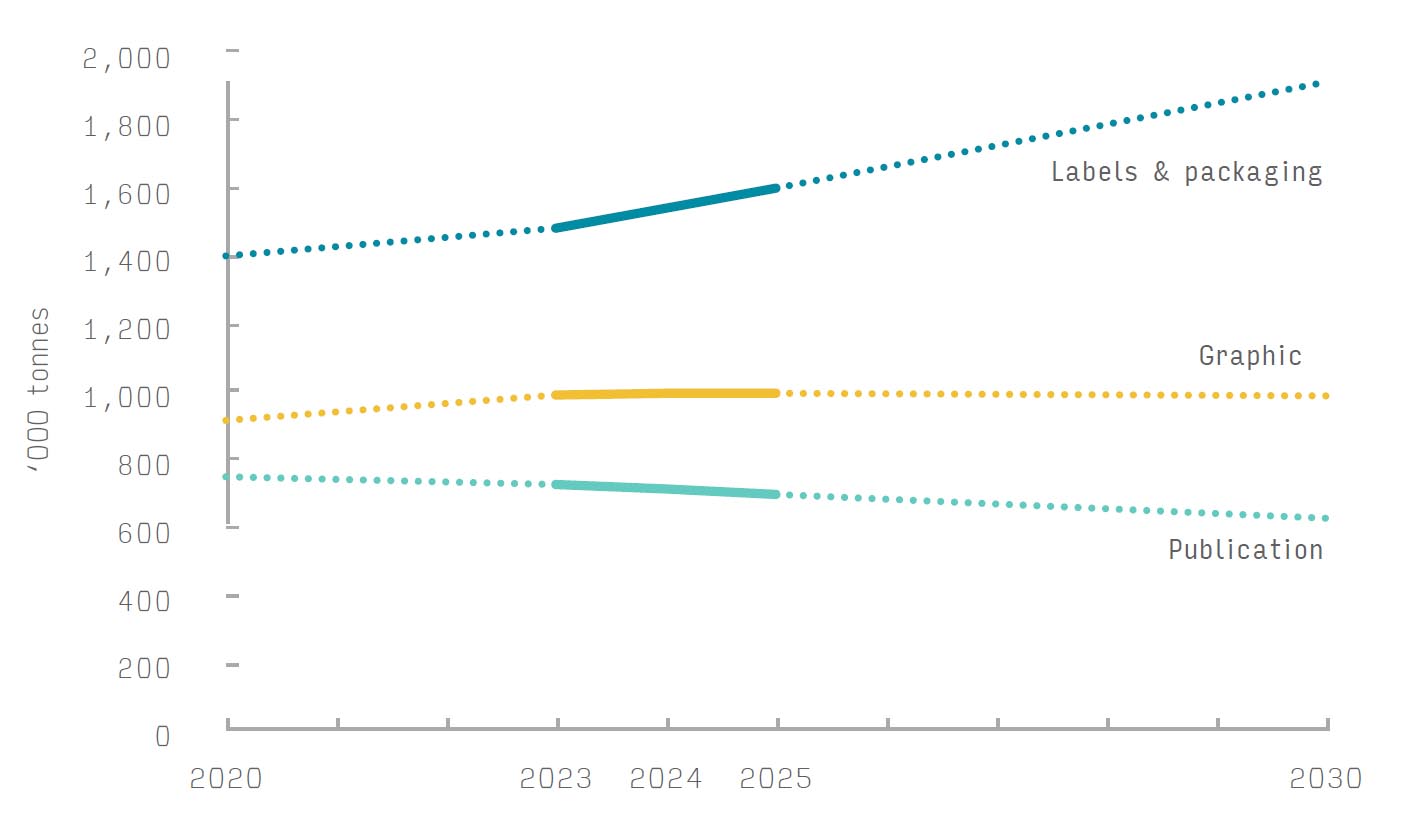

Demand for inks used in commercial graphics, publication, packaging, and label printing will reach 3.3 million metric tons in 2025, with a value of $35.8 billion according to the latest exclusive research from Smithers.

Consumption trends across the remainder of the decade will track wider influences in the print industry. Packaging and food contact-compliant inks will become more important, as publication print volumes fall and graphics print sales remains largely static. Extra value will also come from the development of more aqueous inksets, alongside more bio-based ingredients and higher demand for radiation curing and inkjet inks. Combined, these factors will push global value to $40.2 billion in 2030—equivalent to a compound annual growth rate (CAGR) of 2.3% at constant pricing—according to expert forecasting in the new Smithers market report, The Future of Global Ink Markets to 2030. Volume consumption will advance more slowly at a 1.4% CAGR, to reach 3.5 million metric tons in 2030.

Remaining competitive in this marketplace with raw material costs rising is increasingly dependent on innovation to address the evolving nature of print sector.

Digital Print

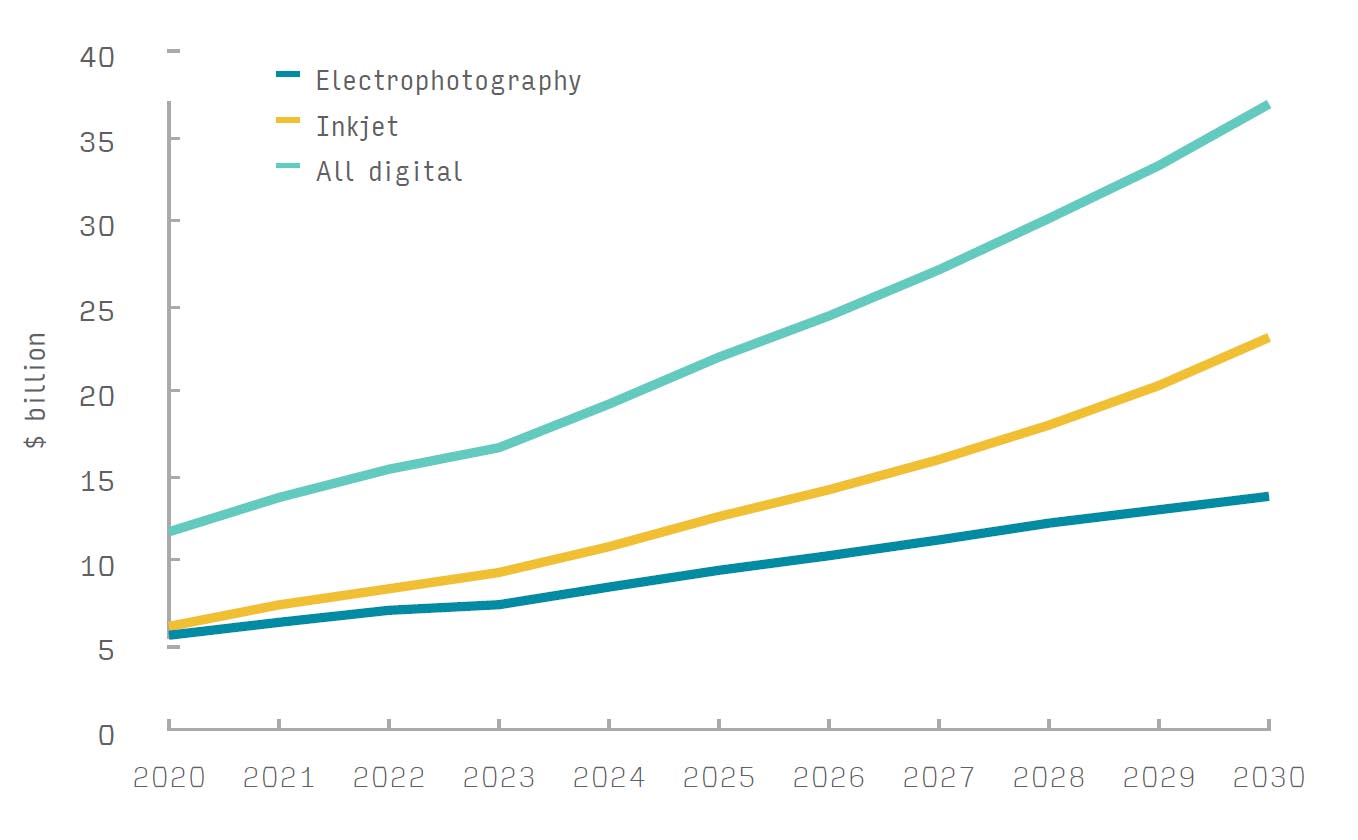

The call for faster turnaround on shorter print runs is pushing several segments towards wider use of digital print. While HP Indigo retains a significant share of the toner printing market, most future growth will come from a new generation of faster, high-resolution inkjet presses.

Water-based and radiation-curing inks are increasingly popular for inkjet, including some hybrid UV-water chemistries. While these do require extra drying or curing time, they are proving more popular than solvent inks that require out gassing prior to finishing processes such as lamination. On single-pass inkjet configurations, using water-based inks creates a greater emphasis on integrating recirculation technology to prevent nozzles clogging, or inline scanning to detect and compensate for blockages.

The digital print segment remains lucrative and the focus of much R&D. Partially because inkjet OEMs still operate a closed consumables model, with warranties linked to printing with approved proprietary ink formulations. Some hardware vendors are now implementing a “cost per page” sales model for inks and other consumables. Although not universally popular with printers and converters, it is an effective means of minimizing press downtime, and aligns to the trend for OEMs to offer service-based solutions to their customers. Some analog equipment suppliers are also investigating this potential, such as Heidelberg with its Subscription Smart and Subscription Plus programs that supply inks and other consumables alongside servicing, workflow, and training support.

Extended-Gamut Printing

Many press rooms are increasing automation, with some even moving towards a “smart factory” or fully “lights out printing” model, where jobs can be completed even when no staff are in the building. To increase uptime and eliminate the need to change colors, many more analog print lines are phasing out specially mixed spot color inks, and instead using fixed color or extended gamut printing. Besides improving uptime on the press this also reduces ink wastage.

This is a standard approach for inkjet and most offset litho presses with extra stations for orange, green, and violet inks or coatings increasingly common. Flexo presses are now moving towards this approach, with both BOBST and Mark Andy offering it as an option. This does pose extra challenges however to standardize anilox rolls, plates and plate-mounting tapes to run without spot colors.

Green Printing

Sustainability in operations is a unifying trend seen in nearly all end-use markets for print. This is driving greater sales of water-based inks, already accounting for 18.5% of contemporary volume consumption, these will be the fastest growing of any ink chemistry through to 2030, increasing their market share to 19.7%. The main applications for these are as replacements for solvent-based inks on flexo and gravure press lines, and proprietary inksets for inkjet systems.

Alongside this there is new interest in bio-based ingredients and inks that encourage better recycling of paper and plastic print substrates. This is pushing formulations away from materials such as nitrocellulose that are difficult to de-ink in end-of-life processes.

Multiple guidelines are being produced to promote the recyclability of labels and packaging, and make recommendations on ink and coating selections. Currently they are voluntary, but by 2030 these will be codified in Europe under new design-for-recyclability criteria that will be adopted as part of the Packaging and Packaging Waste Regulation (PPWR).

Simultaneously environmental claims are far more prevalent in marketing inks, highlighting the CO2 savings associated with reduced emissions of volatile organic compounds (VOCs) and faster, less energy-intensive drying.

Food Contact Inks

In parallel, there is a major drive towards more recyclable materials, including more paper-based substrates and new mono-material polymer constructions. This is placing an emphasis on developing new chemistries to enable inks to wet and bond with low surface energy substrates, faster drying inks, and new coatings to protect the finished print film.

With many of these being used in food packaging there is more interest in developing inks for both direct and indirect food contact. This will lead to more dedicated UV-curing inks being developed for inkjet printing on labels, flexible packaging, and corrugated board. New water-based inks are attracting greater interest both for indirect food contact printing, and increasingly direct food contact as well.

The Future of Global Ink Markets to 2030 from Smithers analyses and quantifies this market in dedicated detail presented in a data set of over 350 tables and figures. It is available to purchase now.

Ink consumption by end-market segment, 2020–30 (thousand tons)

Source: Smithers

John Nelson is an award-winning editor and journalist working in the market reports and consultancy business of Smithers. Here he covers market and technology developments across multiple technical and commercial segments; including home and personal care, sustainability, packaging, printing, paper, nonwovens, rubber and tires.