By John Nelson

Despite multiple forces pushing print service providers to adopt digital technology, a large installed base means analog presses will continue to print the majority of global output for years to come. Simultaneously, market factors will combine with technical developments to make flexo the fastest-growing analog process across the remainder of the decade, and beyond.

This outlook is examined and quantified in the recent Smithers market report The Future of Flexographic Printing Markets to 2029. Smithers expert data forecasting shows that in 2024, global flexo output reached 8.6 trillion A4 print equivalents (542.4 billion meters square), making it the second most productive print process, behind coldset litho.

Yielding revenues of $230.5 billion in 2024, flexo has the highest individual share of print value (25.7%), greater than sheetfed litho (20.2%) and digital (18.4%). It has the best outlook for any analog process. Smithers forecasts a compound annual growth rate (CAGR) of 3.0% that will drive value to $267.2 billion in 2029 (at constant pricing), with output topping 10 trillion A4 equivalents for the first time in that year.

Print Products

The prospects for flexo are positive because of its popularity in packaging applications where demand continues to expand, even as most graphics and publications sectors are static or declining.

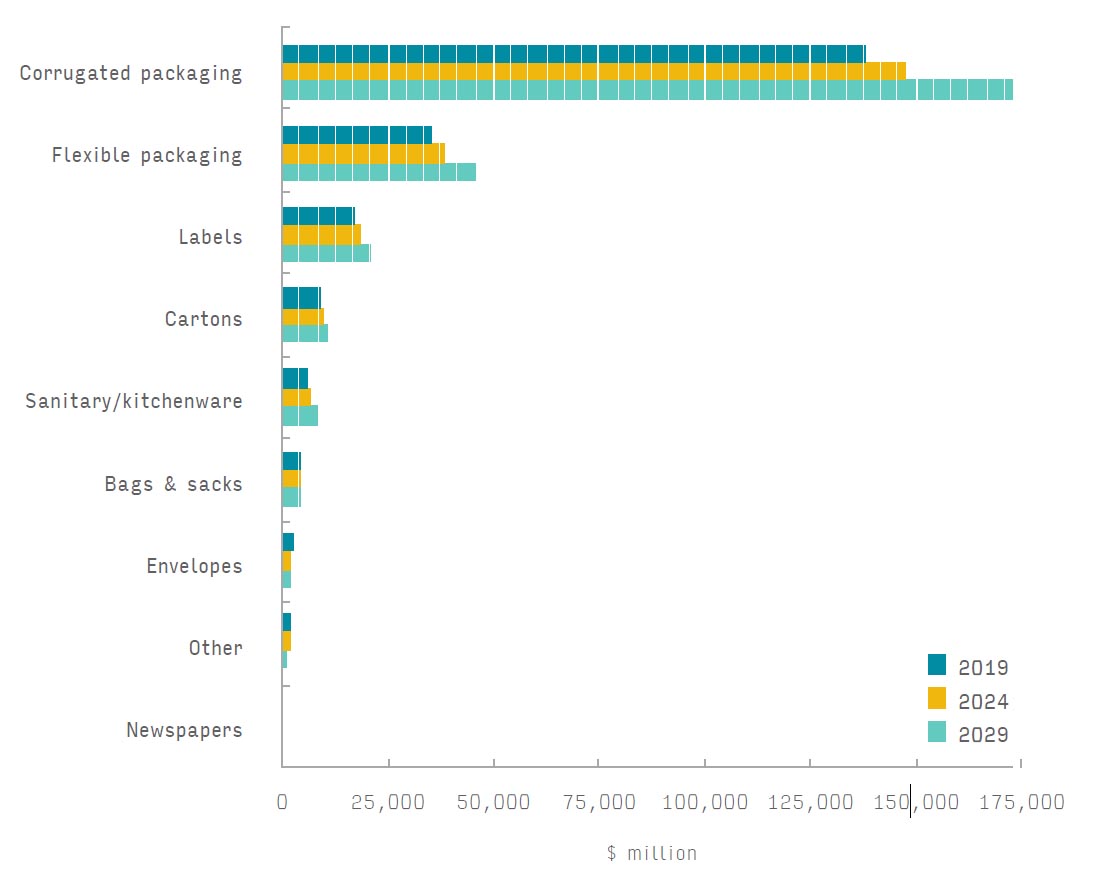

Printed corrugated board is the most important segment accounting for 64.0% of global flexo revenues in 2024; labels, flexibles, folding cartons, and bags & sacks account for a further 31.1% collectively. The outlook for all these is positive; except for bags & sacks, as these formats are phased out in favor of IBCs.

Flexo is used in newspaper and mail printing, which are facing steep declines as consumption moves to online channels. It has a much smaller exposure in these segments than other analog processes, such as offset litho, and any losses will be absorbed by rising demand for high-volume packaging work.

Digital Challenge

Flexo is well-positioned to resist the challenge from digital (inkjet and toner) print. Despite a large installed base of digital presses for labels, and the arrival of new higher-throughput inkjet machines for corrugated, flexo remains most cost-effective for the longest runs—where digital is least competitive.

For label converters, digital and flexo are increasingly being embraced as complementary. OEMs are selling more hybrid configurations with inkjet stations fitted on narrow web machines providing variable data functionality, while flexo units continue to print large areas and graphics.

Penetration of digital is lower in other packaging segments—flexibles, folding cartons, corrugated—and ongoing demand for cheap monochrome, lower-quality work will protect flexo print volumes in the future.

In non-packaging end-use markets for flexo, such as hygiene goods and kitchenware, digital printing is still an embryonic process. There are no clear advantages in printing these tissue or nonwoven substrates with digital, except for some novelty production.

Technical Innovation

Beyond embracing hybrid print, there are multiple other technical developments entering flexo print rooms. As with all print processes, there is interest in greater automation, including for automatic press parameters, such as impression pressure, registration, temperature, and tension. This is supported by hardware that scans plates and sleeves offline to measure surface topography, verify the quality of the plate, and record registration data. The potential of these is now being enhanced by more bespoke software, including AI-learning algorithms that can process data from multiple machines to improve job monitoring and maintenance planning.

In flexo, automation is answering the long-term goal of moving towards more fixed/expanded color gamut (FCG/ECG) printing, minimizing ink consumption, and requiring less operator intervention. On modern flexo machines, additional color stations can now give a Pantone color reproduction rate of over 90%. Development of FCG printing is not straightforward as it requires standardization of all inputs to the flexo process, including inks, plates, and tape, as well as parameters on the press.

Plates and Screens

Automation is being used to lower the financial and environmental cost of manufacturing flexo plates as well—moving a traditionally multi-phase process to a single step, which produces a mount-ready plate without operator input.

As print buyers increasingly investigate the carbon impact of their commissions, several innovations have been developed. Asahi Photoproducts has introduced the AWP CleanFlatMedium plate, featuring improved ink transfer to less planar surfaces, enabling converters to effectively print more sustainable substrates, such as uncoated papers and recycled film stocks. Plate makers are reducing the need for solvents in plate preparation, and incorporating more recycled materials into plates.

The impact of changing print demands, and the latest technology developments for flexo are analyzed and quantified in the new market report—The Future of Flexographic Printing Markets to 2029—available to purchase now from Smithers.

Figure 1: Global flexographic printing output by print product, 2019–29 ($ million, constant [2023] prices & exchange rates)

Source: Smithers

John Nelson is an award-winning editor and journalist working in the market reports and consultancy business of Smithers. Here he covers market and technology developments across multiple technical and commercial segments; including home and personal care, sustainability, packaging, printing, paper, nonwovens, rubber and tires.