By John Nelson

drupa 2024 provided a showcase for the latest developments in the ongoing competition between digital (inkjet and toner) and offset print, with a host of new higher-productivity inkjet presses on display. Across the event there was a major focus on software and connectivity for both digital and analog print lines—boosting productivity and responsiveness on each.

These technical developments underpin the enduring trend for work to transition from analog to digital, which itself has several distinct drivers, and is notably affecting the market for offset litho print. These are analyzed and quantified in detail in The Future of Digital vs. Offset Printing to 2029—the new in-depth market study from Smithers.

Falling Demand

Smithers market data show that demand for all offset litho (sheetfed, heatset, and coldset) work has declined since 2019, from 32.56 trillion A4 print equivalents, valued at $354.4 billion; to 26.97 trillion and $311.9 billion in 2024 (constant 2023 pricing).

The majority of volume lost was in heatset and coldset segments, with dropping demand for magazines and newspapers the principal reason. This was a pre-existent trend, but accelerated rapidly during the COVID-19 pandemic. Lockdown orders reduced publication purchases, with many consumers instead moving to online platforms for news and other media content.

This was especially noticeable for coldset litho where volumes fell from 16.86 trillion A4 sheets in 2019 to 13.03 trillion in 2024. Simultaneously global heatset volumes lost around 1.5 trillion A4 prints.

The smallest reduction was in sheetfed. Although the process is used in magazine print it has multiple other applications, mainly packaging and labels, that did not fall off during the pandemic. Still, total output declined from 7.18 trillion to 6.85 trillion A4 prints across the five-year period.

Smithers forecasts that for sheetfed litho across 2024-2029, although product mix will shift, value and volume will once again start to increase. Demand for coldset and heatset print will both continue to trend downwards, albeit at a slower rate, removing a further 2.54 trillion from global print volumes, and annual worldwide sales declining by $16.8 billion by 2029.

The Challenge of Digital

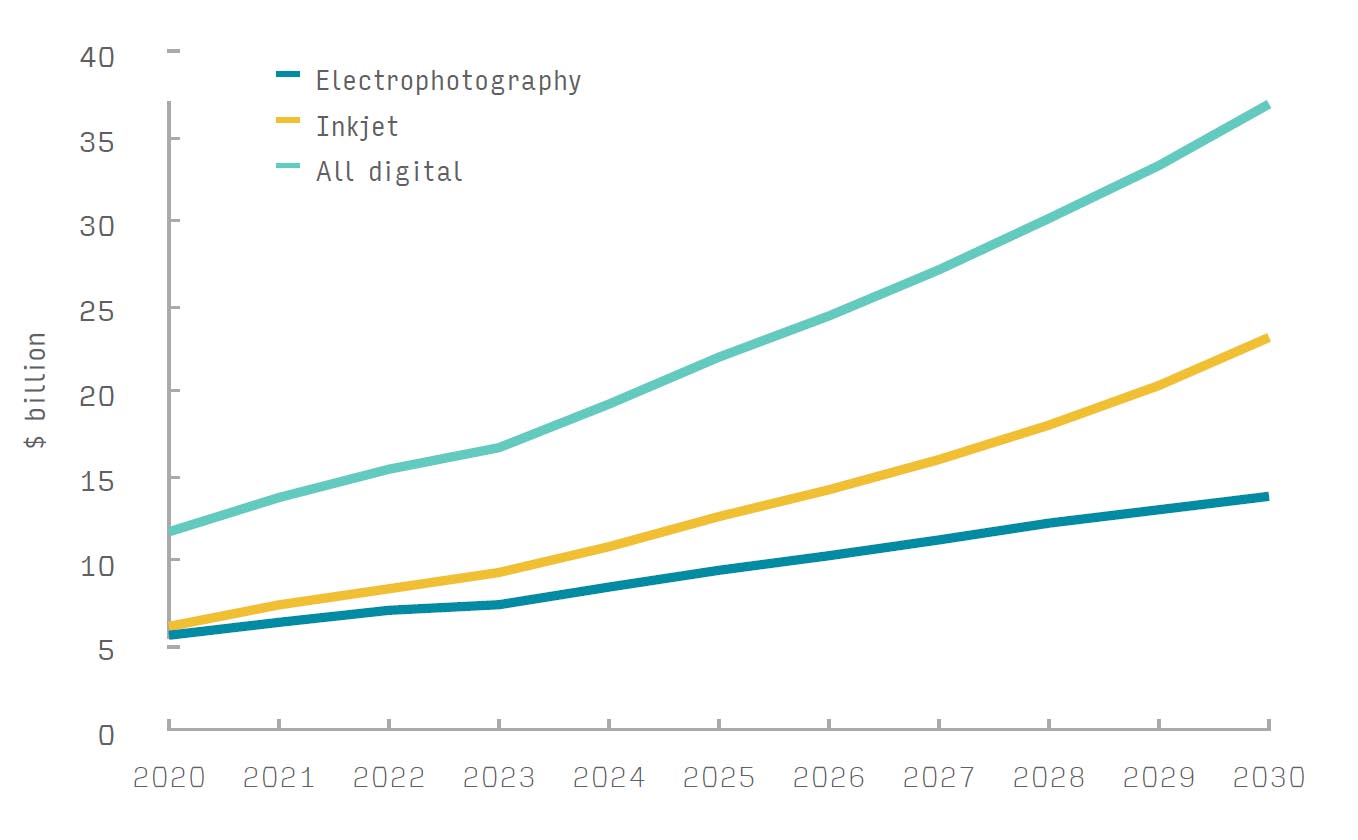

For remaining offset presses, especially sheetfed models, there is increasing pressure from digital printing. However, its market share by volume remains low, only 4.2% of global output in 2024. Digital is increasingly lucrative, worth $165.5 billion in 2024 or 18.4% of total print sales; and a focus for many OEM R&D strategies.

Digital is versatile, especially for variable data work, has very quick set-up, and low wastage, making it much more price-competitive for shorter run lengths. This is in direct contrast to offset, which is most cost-effective on the longest runs. Average run length orders are declining however, favoring digital. This reflects several customer developments, including lower inventory levels, and in segments like packaging, SKU diversification.

Print buyers are calling for faster turnaround and greater control of jobs, which is channeling work through web-to-print order systems. This benefits toner and inkjet machines, which as digital-native technologies are easier to integrate to these platforms.

As print buying continues to move toward short runs and online commissioning, Smithers forecasts that across the next five years total digital print sales will increase to $209.1 billion, giving it an 21.0% share of 2029 sales. As this happens inkjet will increasingly displace electrophotography as the preferred print technology, reflecting the greater availability of new higher performance presses and dedicated machines designed for growth segments like packaging. Across 2024–2029, inkjet sales will increase at a compound annual growth rate (CAGR) of +6.9%, compared to a more turgid +1.7% CAGR for toner, which is only marginally better than the outlook for sheetfed litho.

Opportunities for Offset

There is still potential for offset, especially sheetfed. Although consumption of traditional high-volume publication products—newspapers, magazines, and catalogs—will continue to fall, new sales into packaging and labels can compensate for this. It is an established technology that gives high-quality print and will still be competitive on longer runs where low unit cost is the priority.

Offset OEMs are investing in automation and superior software to improve sheetfed litho’s suitability on shorter run lengths. It is also enabling printrooms to better organize analog print lines, in some cases alongside digital presses in “smart factory” configurations—providing highly cost-effective production, with a minimum number of touch points.

Better automation addresses the worsening skills shortage in the sector. Newer presses are increasingly equipped with an array of sensors allowing remote diagnostics and predictive maintenance, often backed by AI learning algorithms.

Established offset press manufacturers can also follow the wider trend to diversify their sales business portfolio—moving to leasing models incorporating service, support, and maintenance services; as well as consumables. This approach enables print service providers in overcoming any cost barriers that restrict access to the latest equipment.

Newly published from Smithers, The Future of Digital vs. Offset Printing to 2029 quantifies the market by print process, end-use application, and region and is available to purchase now.

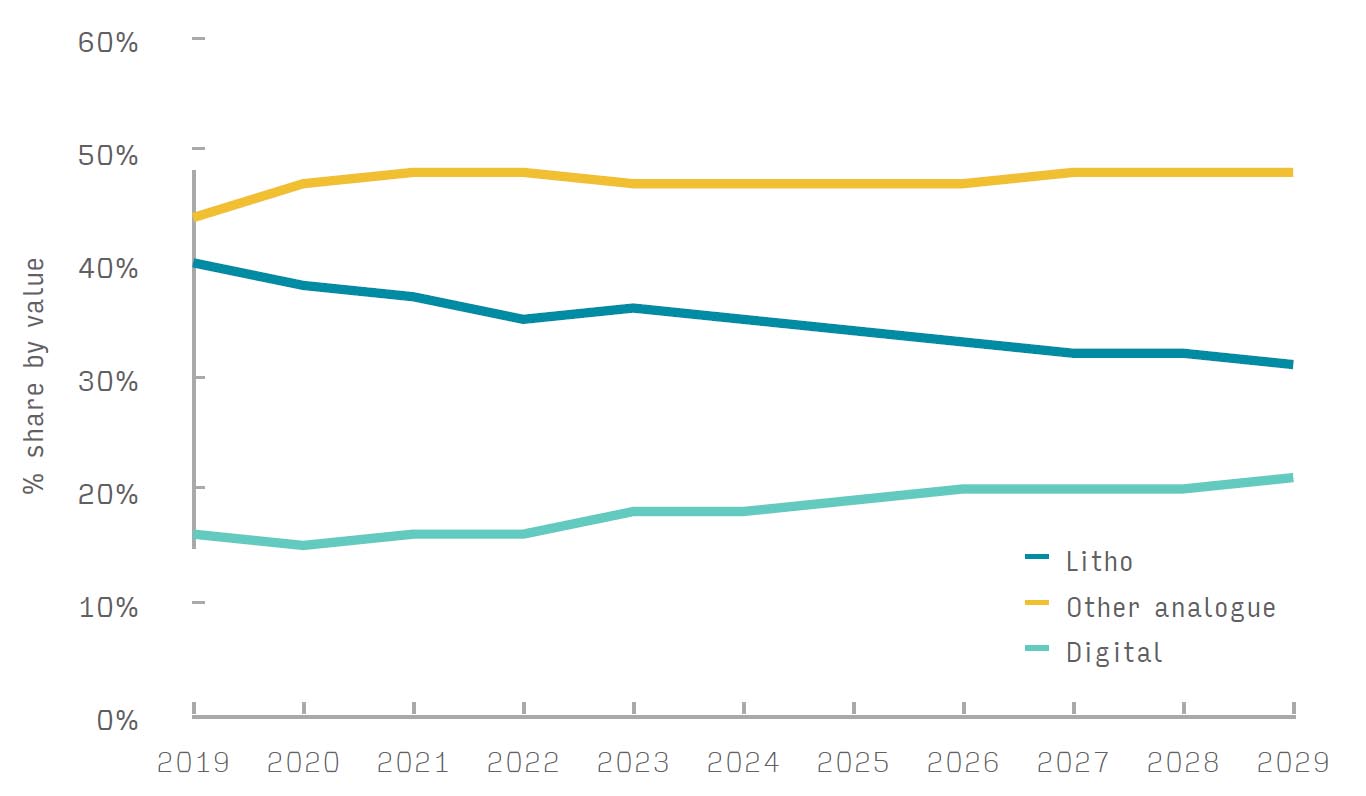

Figure 1: Litho, other analog and digital print market development, 2019–29, in value terms (% share by value, constant 2023 prices & exchange rates)

Source: Smithers

John Nelson is an award-winning editor and journalist working in the market reports and consultancy business of Smithers. Here he covers market and technology developments across multiple technical and commercial segments; including home and personal care, sustainability, packaging, printing, paper, nonwovens, rubber, and tires.