Have you considered reselling? An increasing number of printers are, and one of the surprising products they are ordering on behalf of their customers is paper checks.

Surprised by paper checks? You shouldn’t be. There are plenty of businesses and organizations that still use them. According to The Federal Reserve, there were 3.1 billion commercial check transactions in 2023. This is down from 6.0 billion transactions in 2013, but 3.1 billion is still a lot of checks.

Who’s writing all these checks? We intuitively understand that small businesses and nonprofits are more likely to do so than others. However, we also see paper checks being written in markets such as construction and the trades, property management and real estate, government agencies, healthcare, and education.

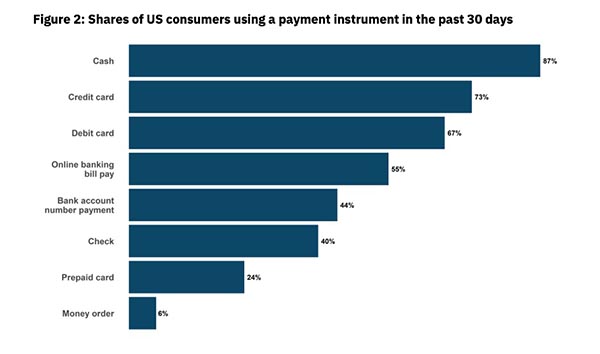

Source: “2023 Survey and Diary of Consumer Payment Choice: Summary Results” / 2023 SDCPC

Financial Models That Drive Paper

What is it about these markets that makes them more likely to use paper?

- Transaction costs. Businesses with high numbers of transactions are more likely to use checks. The more transactions a business processes, the more the per-transaction fees add up. For some, the processing costs of card payments can have an out-sized impact on their bottom lines.

- Paper trail. Paper checks appeal to businesses in highly regulated industries that need to maintain detailed financial records. In these situations, the written paper trail offered by paper checks can be a real plus.

- The combination of the paper trail, higher level of security of the physical checks, and ability to manage payments (such as being able to stop a check if necessary) means that checks maintain their appeal for some businesses, especially for larger payments.

- Familiarity and comfort. Sometimes a business owner is simply more comfortable with traditional banking workflows. This is the factor the most likely to change with time, but for now, it’s still driving check volume.

- Ability to manage cash flow. Especially for those handling large pass-throughs of payments, by delaying cashing a check, businesses can maintain liquidity for a longer time.

Ultimately, it largely comes down to how businesses handle their finances. Businesses that fall into the categories above are great candidates for both check printing and resale based on their business and financial models.

Large Payees Are Disproportionate Check Users

For example, businesses that make and accept large payments are disproportionately likely to use be check users. While the number of commercial checks processed has dropped by nearly 50% over the past 10 years, the average value of each check has gone up. In 2023, the average value of a commercial check was nearly $2,700, more than double the value 10 years earlier when it was $1,329. (In today’s dollars, that $1,329 would be $1,776, so this increase in value is not solely due to inflation.) Compare this to the average commercial credit card payment of $259.

This pattern exists on the consumer side, too. According to The Federal Reserve Bank of Atlanta (“2023 Survey and Diary of Consumer Payment Choice”), 71% of consumers still own paper checks, and 40% had used them to make a payment within the previous 30 days of the survey. According to the U.S. Federal Reserve, consumers (like businesses) tend to use paper checks for larger payments. In 2022, the average check payment (for both businesses and consumers) was $378. For credit card payments, it was $98.

What’s the takeaway? There may come a time when the printed check business disappears entirely. But that time is not now.