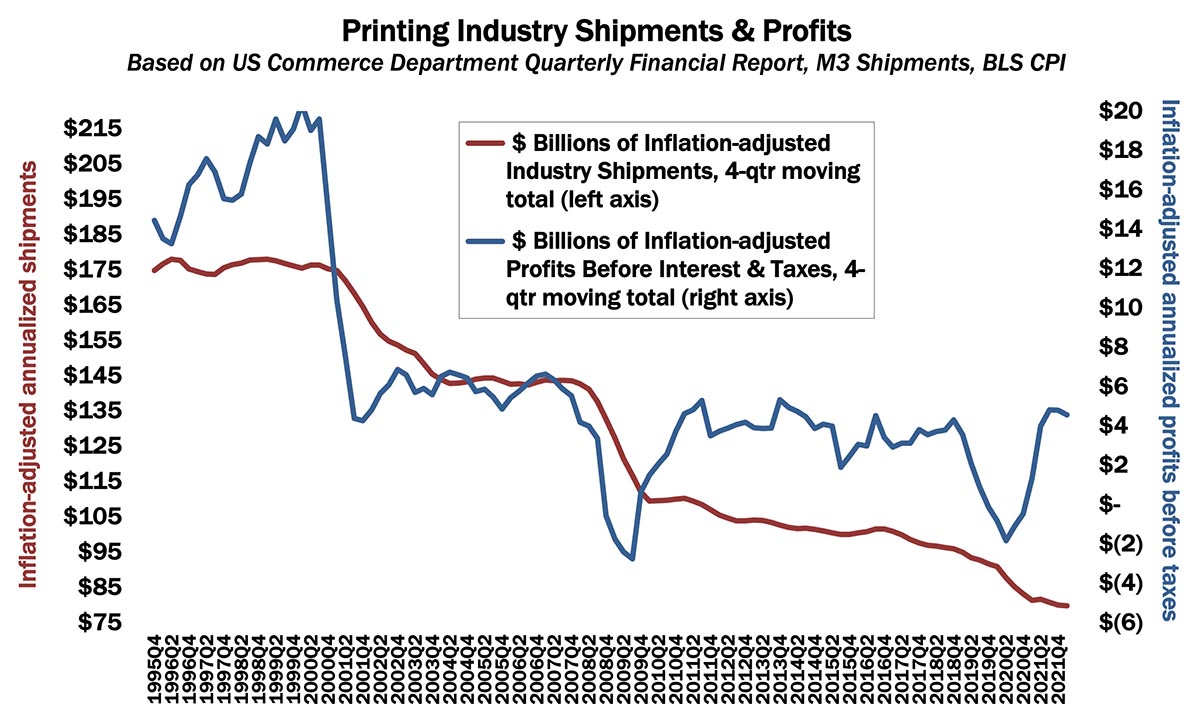

Despite COVID, printing industry profits have been pretty good (heck, we don’t need a pandemic to be unprofitable) with annualized profits for Q1 2022 coming in at $4.55 billion, down a tad from $4.79 billion in Q4 2021.

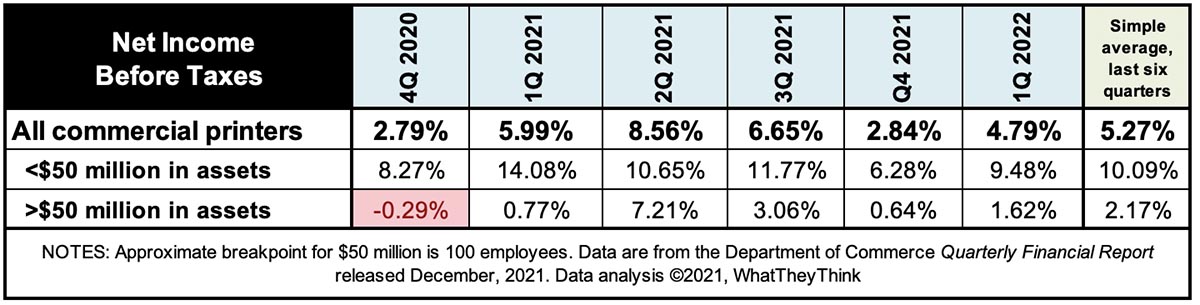

We also look at printing profits by asset class: large printers (more than $50 million in assets) and small printers (less than $50 million in assets).

In Q1 2022, for large printers (those with more than $50 million in assets), profits before taxes had been +1.62% of revenues, not the greatest of quarters, but not the worst either. For smaller printers (less than $50 million in assets), profits before taxes in Q1 were +9.48% of revenues, Again, not the best but not the worst quarter. We had been referring to the disparity between “big” and “small” printers as our “Tale of Two Cities” since there had been a great profit disparity between those two asset classes, although the Census Bureau’s adjustment to $50 million as the break point (see below) now disrupts that narrative a bit. So in Q1 2021, all printers big and small did better profitwise, which means that, for the industry on average, profits before taxes were +4.79% of revenues, up from Q4’s +2.84%. For the last six quarters, profits have averaged +5.27% of revenues.

The asset class division is based on the breakdowns in the Census Bureau’s Quarterly Services Report, whence we get our profits data. Starting with the Q4 2019 Quarterly Services Report, the Census Bureau changed their asset class breakdowns from more/less than $25 million to more/less than $50 million.