In 2018, the world produced about $36 trillion worth of manufactured goods, almost all of which was packaged, protected, and shipped in some form of industrial packaging.

The latest dedicated market investigation into this sector by Smithers—The Future of Industrial Packaging to 2024—tracks how the value of these formats will reach nearly $66 billion in 2024, growing from an estimated $56.1 billion in 2019. This is equivalent to a 3.2% compound annual growth rate (CAGR) across those five years.

An Evolving Market

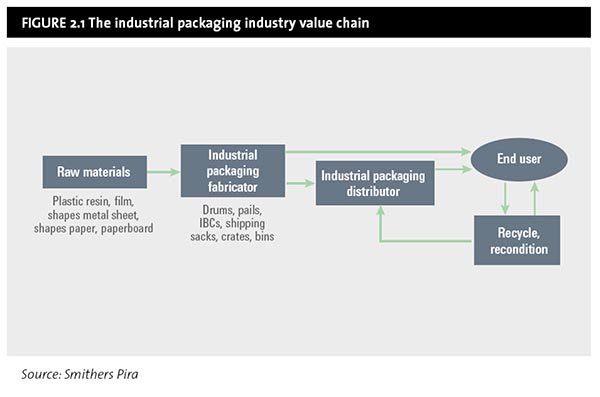

Industrial packaging products and many key end uses are quite mature, and innovations are generally evolutionary and relatively infrequent. The key formats examined in the latest Smithers study are:

- Metal, plastic, andfiberdrums

- Rigid and flexible intermediate bulk containers (IBCs)

- Paper, plastic, and multi-layer composite shipping sacks

- Metal and plastic pails

- Rigid crates, bins and boxes, typically made from wood, metal, or plastic

Growth in physical volumes and value generated by the sector are strongly dependent upon the overall level of global and regional economic health, international trade, and manufacturing activity. Direct innovation in industrial packaging tends originates with raw materials suppliers, especially with plastics materials for drums, pails, and rigid IBCs.

Sacks remain the most valuable industrial packaging format—worth just of a quarter of the market in 2018. Use of sacks is forecast below the market average, however, with the greatest new demand coming for IBCs and drums.

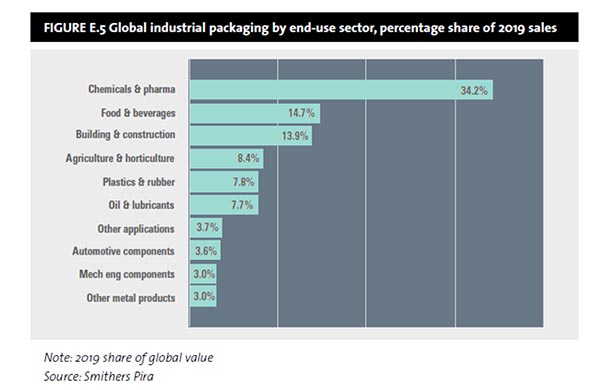

Chemicals and pharmaceuticals remains the largest end-use segment for the global industrial packaging industry—formats for these products will be worth $19.2 billion in 2019. It will also be the fastest growing across the next five years. By 2024, sales into this market will be worth more than the three next largest industrial packaging end uses (food and beverages; building and construction; and agriculture and horticulture) combined.

Smithers’ analysis identifies that over the period 2019–2024, the following specific trends will be key to shaping the use of industrial packaging and selection of formats; alongside general economic shifts:

Sustainability

Reducing environmental impact is a pressing concern across the packaging industry. For industrial packaging, the pressure is less pronounced than in primary packs that consumers actually handle and dispose of. Furthermore, economic pressures mean much industrial packaging is already re-used either directly or via reconditioning. Smithers data shows that, in 2019, 31.2% of steel drums and 20% of plastic drums are reconditioned for re-use.

There are further steps industrial packagers can make towards contributing to a green world. These focus principally on:

- Reducing the amount of packaging material required to ship a unit of product

- Recovering, reusing, or recycling packs.

Downgauging

Pack downgauging also has the advantage of saving on raw material costs for the packaging producer. Improvements in polymer properties allow substantial reduction in the amount of resin required to make a standard 225-liter plastic drum and in plastic and multiwall paper sacks, for example.

Re-use of industrial packaging directlyfavorscertain formats, specifically Intermediate bulk containers (IBCs), metal and plastic drums, and crates/bins. The price of a new drum or IBC, coupled with its durability and ruggedness, and the relative ease with which it may be cleaned, facilitates recovery and reuse.

Global industrial packaging leaders, like Greif, Mauser, and Schütz, provide collection, reconditioning, and recycling services as do numerous local and regional players.

Packaging Waste and Safe-Shipping Regulations

Further impetus for more sustainable industrial packaging is being supplied by legislative initiatives around packaging waste, especially in the EU. Current EU regulations establish timetables and goals for the reduction or elimination of various categories of packaging wastes. The time horizon for these goals is generally 2030.

Regulations that impact producers and users of industrial packaging address regulations aimed at promoting sustainable packaging and regulations aimed at providing safer transport of dangerous goods.

The latter will evolve across the next five years within the scope of existing frameworks, such as the UN’s Orange Book of Recommendations on the Transport of Dangerous Goods. These will coordinate with local and sector-specific legislation to promote more seamless international trade.

Smart Logistics

More sophisticated and affordable electronic sensor and communications technologies, combined with management information software and integration services, are allowing for more sophisticated management of shipments in real time.

Simultaneously, authorities and brand owners in pharmaceutical and food industries are demanding greater transparency to guarantee the safety of bulk shipped goods—for example, monitoring of temperature vs. time exposure of sensitive, high-value shipments like fresh fish and seafood or certain dairy products.

These smart packaging systems are expected to spread rapidly across the forecast period. Smart logistics concepts are unlikely to fundamentally change the design or function of existing industrial packaging formats, however, although there will be greater demand for machine readablelabeling, integrated RF antennas, and monitoring circuitry. This roll-out will significantly increase the overall value added by logistics functions.

Material Innovation

Polymer suppliers continue to innovate to deliver incremental improvements to materials sold for existing industrial packaging formats.

Current improvements are manifest in the development of blow-moulding grades of high-density polyethylene (HDPE) plastic resins that provide greater strength, rigidity, and greater resistance to impact or abrasion. Fabricators may use these improvements to provide safer plastic drums and IBC bottles for transporting hazardous goods, or to offer lightweighting gains.

Similarly, grades of low-density polyethylene (LDPE) and linear-LDPE are being engineered to provide greater puncture resistance and tensile modulus to enable downgauging in shipping sacks. And both LDPE and HDPE grades are being produced that have superior resistance to degradation and stress cracking.

Another area of research is multilayer structures to build plastic drums and rigid IBCs bottles in particular. The goal is to provide a barrier to the diffusion of product molecules or gases through the walls of the container. Similarly, constructed barrier films may be formed into removable, disposable liners for drums and IBCs.

The impact of these changes and other key factors is analysed and quantified in over 300 data tables and figures segmented across all key metrics in Smithers Pira report The Future of Industrial Packaging to 2024.