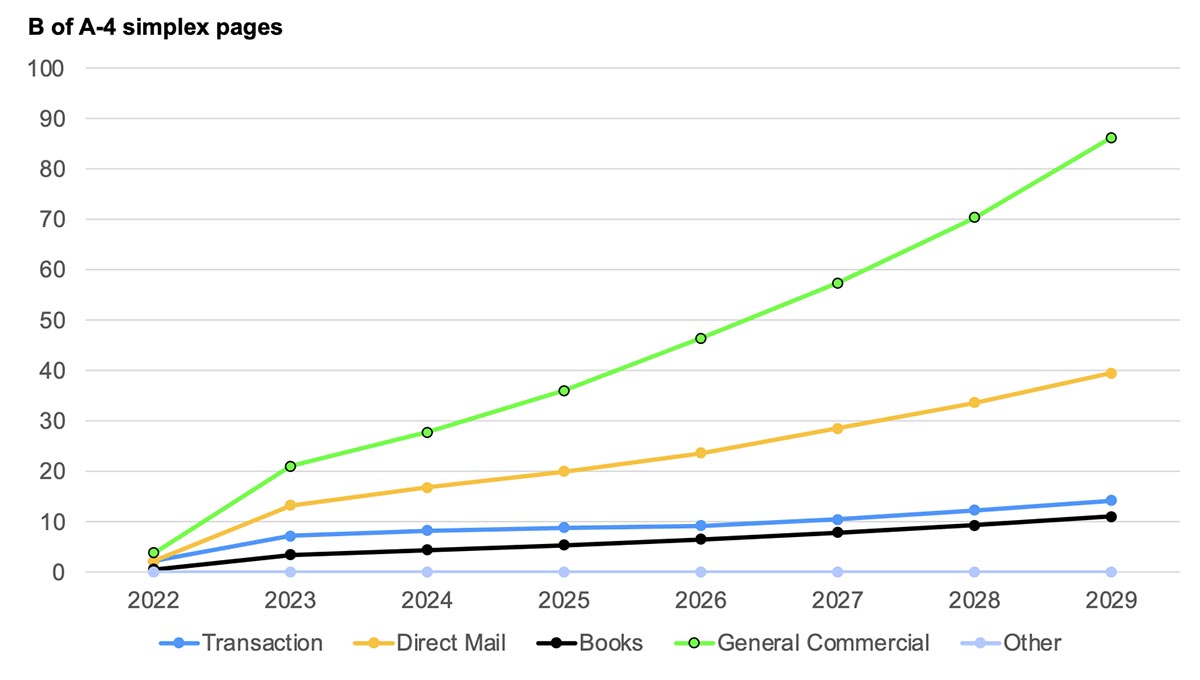

After years of anticipation and frustration at fragmentary progress, it is now possible in 2013 to say that digital textile printing has achieved breakthrough success in soft signage and production apparel printing. Vendor revenues for dedicated systems and ink for digital printing of textiles have come close to $1 billion and are growing at 16%. The biggest news (and the biggest volumes of inkjet textile print) may be the breakthrough into production printing. Though it is specialized, it demonstrates an important future model.

Soft Signage

Soft signage is printed at both specialist print service providers who print flags and fabric signs/banners as well as at general wide-format print service providers who offer fabric signage among other products. Soft signage is printed on dedicated textile specialist systems most of which are used for both soft signage and small quantities of apparel print in the form of samples, strike-off single garments, and design print, all of it roll-to-roll for subsequent cutting and sewing. Print service providers printing soft signage range from the very small to large-contract suppliers. The latter give rise to the demand for larger high-end dedicated fabric printers.

In general, in both the low- and high-end markets about three-fourths of output on dedicated roll-to-roll textile printers is soft signage and one-fourth is the other apparel-related output. In other words, soft signage drives the growth of roll-to-roll dedicated inkjet textile systems.

Value Proposition

The value proposition of soft signage is a specialist one. Soft signage is not displacing large quantities of signage printed on other technologies and substrates so much as generating supplemental demand for a product, which has a special aesthetic appeal to some customers as a more environmentally friendly substrate than some outdoor film products. It also has appeal as a banner- or flag-like format externally, and for some people the dye-sublimation inks used to image the mostly polyester textile substrate generate a unique brilliance of color. There is even a specific and relatively new specialist demand for flags, not just national flags, but local or seasonal flags, or for clubs and associations.

Non-Signage (Low-/High-End Roll-to-Roll) Print Service Providers

Non-signage applications undertaken on roll-to-roll systems consist of apparel-related design, sampling, and strike-off functions. There are specialists focused only on these applications, but it is also true that many print service providers who have dedicated textile roll-to-roll systems are printing these apparel-related applications, so that the total amount of these applications left to be printed at real specialists is only very small.

Value Proposition

The importance of getting inkjet samples in the mainstream apparel industry has been understood for many years; inkjet is able to quickly get samples to market while screen-printed sample swatches can take months to reach the market. The use of inkjet printing in the apparel design process is also understood, as is the use of inkjet for strike-offs (single garment print preproduction). But the market is limited geographically and in volume of print, according to our own user research. Originally, vendors of dedicated roll-to-roll inkjet textile printing systems saw their systems as the gateway to production textile apparel markets. This turned out to be the wrong channel and mode of approach to that market (see below). This means that apparel-related markets in roll-to-roll non-production systems have probably largely taken their value proposition as far as it can go.

Textile Channel Production Roll-to-Roll

This channel, which we are separately defining, constitutes the biggest news of all in digital inkjet textile printing in recent years, and it shows the way forward to a much bigger apparel inkjet production market in the future. Inkjet in Italy in the specialist luxury silk and cotton market has become a technology of choice for analog screen print providers, and today substitution of screen by inkjet is taking place at a growing rate.

The core “channel” for this market is the specialized and close-knit group of screen textile printers in northern Italy who serve the specialist high-value luxury market focused on this region for printed silk and cotton goods. This is a community of many tens of independent printers that has co-developed hybrid inkjet textile printing systems with two major printer vendors and their Italian subsidiaries and partners: Konica Minolta and Epson. The model adopted by Konica Minolta and Epson in Italy was to work cooperatively over a 10-year period with print providers, textile machinery manufacturers, and ink companies to generate a kind of organically-designed set of systems. There has been a pooling of knowledge and experience and of considerable resources without which production inkjet printing of textiles might not have become the reality it is in Italy today.

This cooperative approach has had the knock-on effect in Italy of encouraging Italian textile press and machinery manufacturers who export around the world to develop their own inkjet systems and further spread the word and the technology awareness, which this industry has not had for so long.

Still on the subject of channels and the participants in them who take technology to markets, a further knock-on effect of the development of production systems in the Italian market has been to encourage digital vendors like Durst and probably others who will follow them to develop production textile systems.

Inkjet Printing: Offering a Change in Business Model

The countertrend to the current dominant apparel manufacturing supply chain is the appearance of companies like Zara in Europe, UniQlo in Japan, and Shanghai Tang in China. These companies have reversed the old model and have in some cases fully re-integrated the supply chain back into their own hands in the belief that with modern instant communications, maximum flexibility in time and manufacturing will capture a bigger, higher margin market. This has certainly worked for Zara (Spain), which is now the world’s largest apparel company at $16 billion revenues and the owner being the richest man in Spain. This model would have a clear use for digital printing’s value proposition, though even here the gospel still has to be spread.

It is not today possible to be sure that the new model favoring digital printing with its re-integrated structure will win out over the old model, though it may do so and re-orient the fashion world to fully localized fashion (for which digital printing is also excellently suited).

At this time, the old supply chain stands in the way of the new printing technology. There is effectively no one to talk to and no structural understanding of the ROI of digital printing, and where the investment should be made. There are also no motivations to do anything other than reduce cost. What can happen—and is beginning to happen—is that smaller and specialist retailers as well as some of the new-model supply chain re-integrator companies like Zara can open a path to organic growth. This is happening in Europe, but is also beginning in countries like Turkey, Brazil, and India. There are indications that there is interest in China. The model seems to be more one of specialist market and parallel new market development as so often with digital print. But a more rapid conversion to digital in the textile industry is going to have to await fundamental shifts in the mainstream supply chain.