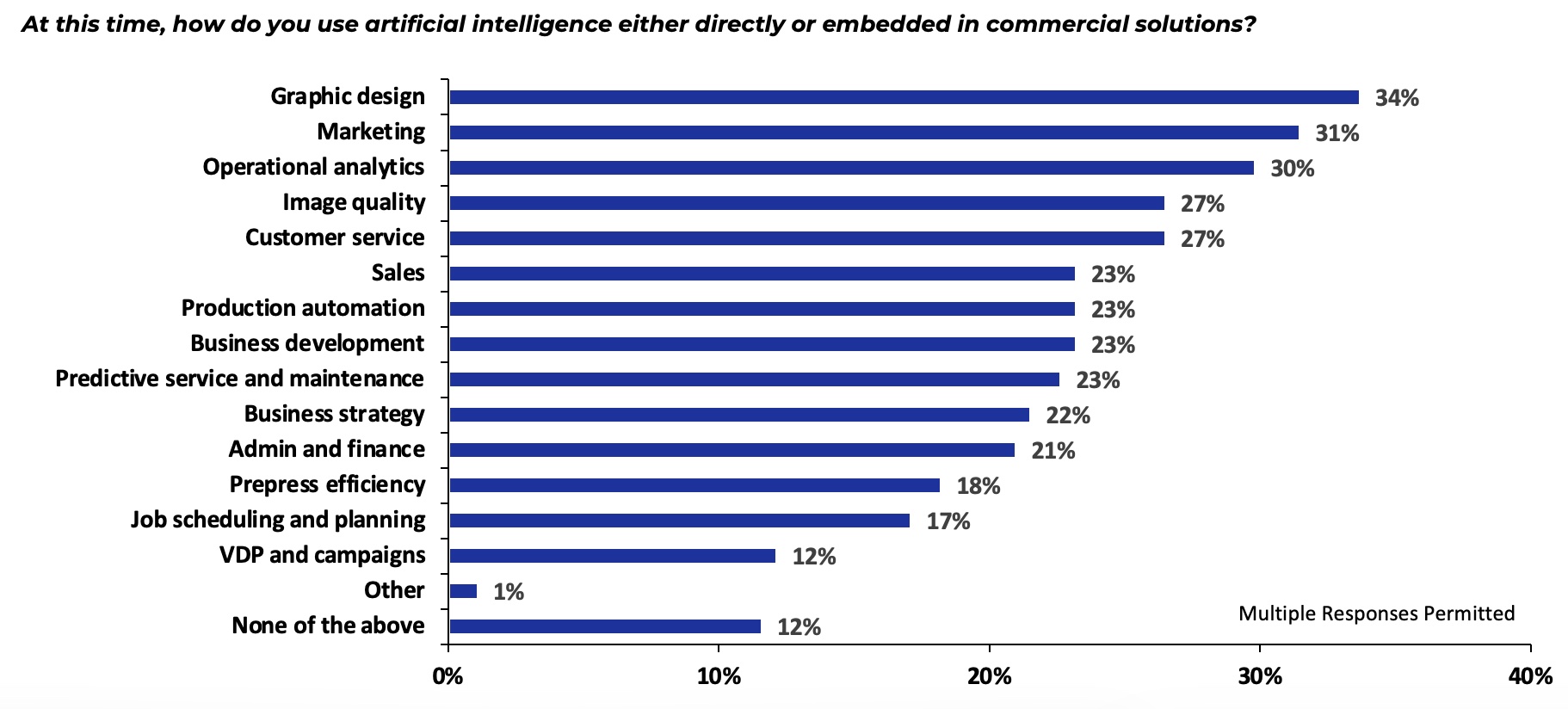

- Package printing’s share of total print is forecasted to increase from 45% in 2024 to 55%–60% by 2030.

- Labelexpo Europe attendees had a variety of opinions about their participation in the industry, their specific offerings, and the importance of narrow web labels within their overall businesses.

- There is a powerful message about the success of digital coming from mainline converters, but this success is not being successfully promoted by the industry.

(Image courtesy Labelexpo)

By Jeff Wettersten

Introduction

During Labelexpo Europe (held September 16–19 in Barcelona, Spain), conversations about the future of digital printing in the packaging sector proved just as revealing as the technologies on display. In addition to observing the equipment and solutions at the event, we at Keypoint Intelligence set out to better understand digital’s role in packaging. Our discussions with converters, suppliers, and industry leaders uncovered both optimism and hesitation, but one thing became abundantly clear: waiting on digital is no longer an option.

This article provides a brief overview of what we heard during our discussions at the show as well as our opinions about their potential implications. If you’d like to see some of Keypoint Intelligence’s video content from Labelexpo Europe 2025, click here.

Highlights from Our Discussions at the Event

According to numerous analysts, pundits, and publications, package printing’s share of total print is forecasted to increase from 45% in 2024 to 55%–60% by 2030. During Labelexpo Europe, we at Keypoint Intelligence sought to understand how this shift might impact various businesses if this forecast proves true. Our primary desire was to answer the following question: If package printing increases its share to 55%-60% of digital print, and if digital printing grows its share against analog, is the digital supply chain taking the right actions to accelerate market participation?

The discussions we had with converters revealed three distinct models relative to the deployment of digital assets:

- The first is the web-to-print model using an active front end (customer-facing web) to serve the on-demand needs of small businesses. Digital is an ideal fit for this business model.

- The second model includes small to mid-sized converters serving local markets. Digital is also a good fit here, and many in this category are upgrading their aging flexo equipment with digital assets.

- The final group includes mainline label producers, which are typically large single-site operations or multi-site regional/global operations. Many of these firms are using digital printing to drive plant-wide productivity.

We asked converters about their existing customers, how they are responding to their customers’ needs, and whether their customers’ needs change across the three business models cited above. Many of them challenged the specification of three models, as opposed to one. They were also anxious to hear our opinions about the differences in market needs, where they were positioned, and their competitors in that space.

This highlights an industry need. Original equipment manufacturers (OEMs) are focused on print as the ultimate solution, and on their technologies in delivering the ultimate capabilities. The ability to print enables web-to-print participants to deliver a different value proposition to their customers. Likewise, small and mid-sized converters have different needs than mainline label converters.

The industry has an opportunity to accelerate “scale” within narrow web label through mainline converters. Among mainline converters, digital printing is driving plant-wide productivity improvements. There is a powerful message of success coming from mainline converters, but this success is not being successfully promoted. Instead, the industry continues to rely on a 20-year-old value proposition for digital printing.

Whereas other print markets are declining, packaging is growing. This is attracting printers as well as suppliers to expand into packaging. The lines between traditional packaging converters are blurring, with single converters now participating in multiple packaging applications. Digital printing is also enabling broader participation for upstream value chain participants, including contract packaging, contract manufacturing, fulfillment operations, and brands.

The Bottom Line

We believe that market access will be the primary driver defining future levels of participation in digital printing. Industry consolidation may occur on several levels, with traditional analog participants entering digital printing (e.g., Heidelberg/Gallus, Mark Andy, Bobst), incumbent digital participants partnering with analog incumbents (e.g., domino, Konica Minolta/Mark Andy, Durst/OMET), and other incumbent suppliers seeking value-added capture through vertical integration (e.g., Flint/Xeikon). We expect these changes to accelerate in future years.

Through our discussions with Labelexpo Europe attendees, we were able to gain consensus that even if the digital supply chain is taking the necessary actions to accelerate market participation, digital print for packaging will still need to rapidly accelerate to secure a meaningful position in printed packaging. At Keypoint Intelligence, we’re often asked why digital print for packaging has not seen more success. Our response is this: Digital printing requires some level of investment, as well as commitment by the organization to make it succeed. The industry must do a better job of highlighting digital success in driving the entire business forward, rather than merely supporting a small piece of the business.

Staying Ahead of the Curve

Keypoint Intelligence is evaluating the launch of a multi-client study to explore the role of digital in package printing. The intent of this study would be to highlight and promote the business transformation occurring across all segments of packaging, narrow web labels, corrugated, folding cartons, and flexible packaging via converter and brand case studies. We would hope to gain a clearer understanding of the issues addressed, the solutions deployed, and the impact within the industry. We have some powerful examples that may help highlight the true potential of digital printing, shifting the message from threat to opportunity.

We would welcome your input/questions as we continue our discussions about whether to take on this important project. Please feel free to e-mail us at [email protected] or [email protected] if you have any thoughts or desire additional information.

Jeff Wettersten is the VP of Packaging for Keypoint Intelligence’s Labels & Packaging Advisory Service. Jeff uses his expertise to assist digital technology developers in assessing and developing commercialization strategies for new and emerging digital markets.