By John Nelson

The US printing industry is in a period of profound transition, posing new challenges for leaders at all stages of the value chain. Traditional print segments are declining sharply, new commercial opportunities are emerging, but often require strategic reorganization of businesses and equipment assets. This is happening at a time when the composition of the typical US print room is also changing, with older veteran staff replaced by less experienced, but digitally native, operators.

How this ecosystem will evolve across the next five years is one of the main topics in the latest report—The Future of Printer Demographics to 2028—from Smithers, the leading consultancy for the paper, print, and packaging industries.

This Smithers survey covers 60 countries worldwide. It calculates that since 2018, the number of printing and related businesses globally has declined by -11.9% from 667,630 establishments to 587,934 in 2022. There has been a corresponding fall in workers in the sector, reaching 4.06 million in 2023; down from 4.80 billion. This is indicative of a general decline in demand for conventional printed books, newspapers magazine, etc., since the beginning of the millennium, which was accelerated once COVID-19 lockdowns catalyzed even greater use of online content.

How Are US Printers Doing?

These trends are very evident in the US. The number of printing and allied business in the country dropped from 24,775 in 2018 to a projected 21,843 in 2023. Employment meanwhile fell from 438,251 people in 2018 to 370,920 in 2022, a fall of over -15%.

US print rooms suffered during the pandemic. Furloughing and employee retention schemes were less generous than in many other developed markets, and many older experienced workers took pandemic layoffs as an opportunity to leave the workforce permanently.

Value in the segment followed a similar trajectory. Declining from $82.6 billion in 2018 to $79.59 billion in 2019, there was a sharp drop to $73.77 billion in 2020. This was followed by a recovery year in 2021, when revenues reached $77.52 billion. Exports of print products from the US have also declined, while imports have shown a slight increase.

There are still some positive signs. Over $5 trillion of post-COVID stimulus funds has helped drive a return of consumer spending, while the US economy has suffered less from the rise in energy prices in the wake of Russia’s invasion of Ukraine.

Where Is Demand Growing?

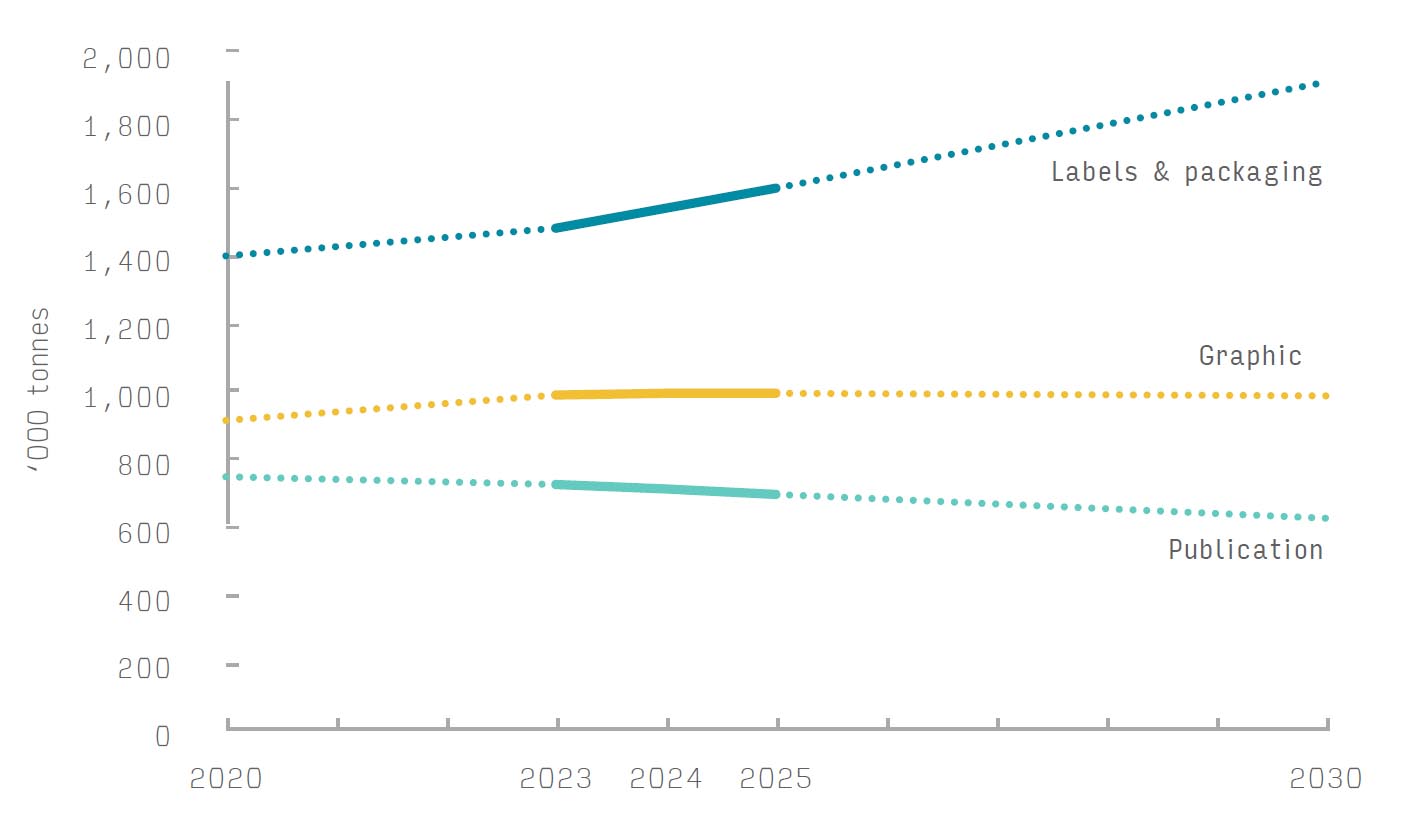

Rather than anticipating the return of vanished markets, for print business owners the impetus now is to identify and secure market opportunities in the new post-COVID economy. Smithers data show US publications print (newspapers, magazines, books, directories) will continue to decline at -2.7% year-on-year across 2021–2026. Meanwhile, graphics work (advertising, commercial print, photobooks, direct mail/transaction print, and security print) will continue to decline marginally at -0.8% year-on-year, despite a minor post-COVID bounce.

In contrast, the demand for printed packaging and labels—a segment where there is no virtual, online competition—continues to grow at a forecast rate of +1.7%; and will represent 56.4% of all value in the US print market in 2026.

There are several trends within the packaging print market that can be exploited for profit. Run length orders are declining, even as CPG companies are again increasing the number of SKUs they sell. The market is calling for faster turnaround in print jobs, with anticipated delivery times reducing from weeks to days—some businesses now promise next-day delivery with a significant payment premium.

Within the packaging segment, these factors are especially important for e-commerce businesses. This is a segment that will pay more for fast turnaround and greater flexibility in print ordering. Demand for printed e-commerce packaging is booming—Smithers forecasts this will almost double globally from $13.01 billion in 2023 to $24.57 billion in 2028 (at constant pricing).

The same factors are present in other subsegments of the market, including lucrative channels such as print-on-demand apparel, photo products, home furnishings, and books.

For commercial print, some organizations used COVID to rationalize their operations, including the closing of corporate reprographic departments. This creates opportunities for discrete businesses if they can connect with these new customers and provide a responsive, high-touch service.

At the same time many corporate clients are reappraising their supply chains in the light of stronger environmental, social and governance (ESG) targets. This includes cutting wastage of print media, reducing VOC emissions, using more planet friendly inks, and optimizing recyclability by moving from plastic to paper substates. A focus on sustainability will support the reshoring of some print work, but creates an onus for print business owners to be able to articulate their own environmental performance. Superior sustainability performance is increasingly common in equipment literature, but there is a need to explain to customers how this translates into a lower carbon footprint for them as well.

How Will This Affect US Printers?

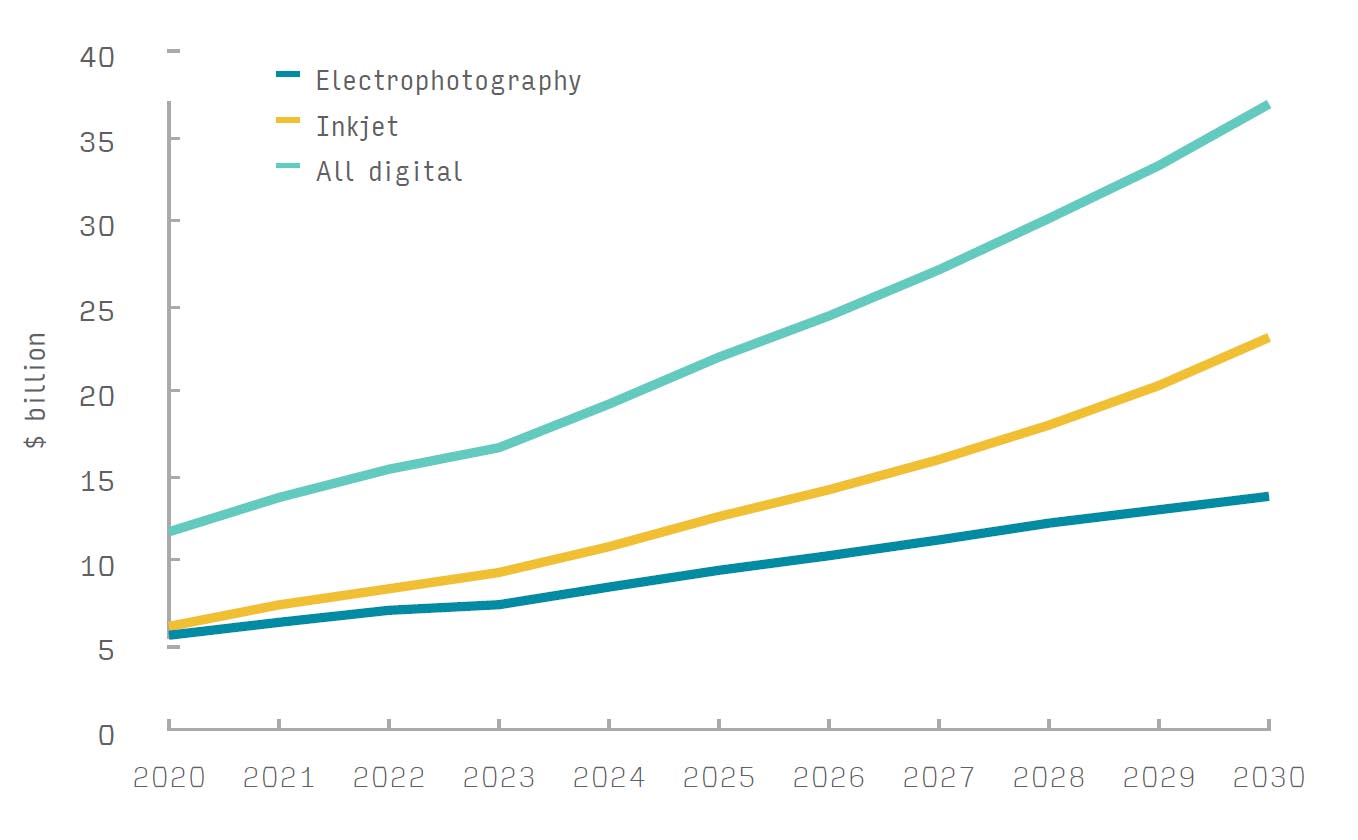

The move to shorter print run jobs is favoring digital, mainly inkjet. For e-commerce in particular, low print runs and fast turnaround favors digital over analogue. As this happens there is a rationale to invest in digital print equipment, especially as quality on these is improving—in some instances indistinguishable to offset litho—and throughput speed improvements are making them more cost-competitive for medium-run commissions.

This is merely the tip of the wider post-COVID trend to increase automation of presses. Even if inkjet machinery is most compatible with the approach, the same trend is evident in analog. OEMs continue to provide enhancements such as automated plate engraving and changeover on flexo and offset litho presses. These steps simultaneously cut wastage in pre-print, reflecting customers’ interest in green print supply.

The range of water-based inks and coating continues to increase across all press types, as do those formulated with fewer petroleum-derived ingredients, such as soy-based inks. In segments like flexible packaging, print line equipment is being optimized to handle rougher, less planar paper substrates in place of plastics; and deposit a new range of easier to recycle barrier coatings. These are all positive gains print leaders can communicate to customers.

Better automation cuts the number of staff needed to maintain and operate a press, helping address long-term staffing issues. Many OEMs are now supplying proprietary smart diagnostic tools, with the potential to collect data from multiple presses in a global network. Such data can be leveraged by OEMs to better analyze faults, and resolve these more quickly via online support subscriptions.

In multiple applications investment in web-to-print platforms for ordering packaging or other products offer benefits in order turnaround. These enable the customer to design work themselves online in pre-set templates, which can be passed to the press with minimal changes or interaction from press operators.

To do this however a print business must have a strong online presence to connect to customers., with an emphasis on communicating reliability, quality, and turnaround. The Internet and platform economy models make finding new clients easier, but the same is true if existing customers want a new print partner. Higher levels of customer service and engagement can help ameliorate this threat.

The rate of decline in number of US print business will continue – even if the remaining companies are handling more work, more efficiently. Smithers forecasts that by 2028 print and allied business in the US will drop to 18,070. There is a parallel inclination to consolidate group smaller print businesses together into networks that can guarantee quick order completion regardless of a client’s location. Better automation means that fewer staff will be required, around 330,000 in 2028, although they will need to be more technically fluent to get the best results out of the latest generation of print equipment.

The Future of Printer Demographics to 2028 is available to purchase now from Smithers.

John Nelson is an award-winning editor and journalist working in the market reports and consultancy business of Smithers. Here he covers market and technology developments across multiple technical and commercial segments; including home and personal care, sustainability, packaging, printing, paper, nonwovens, rubber and tires.