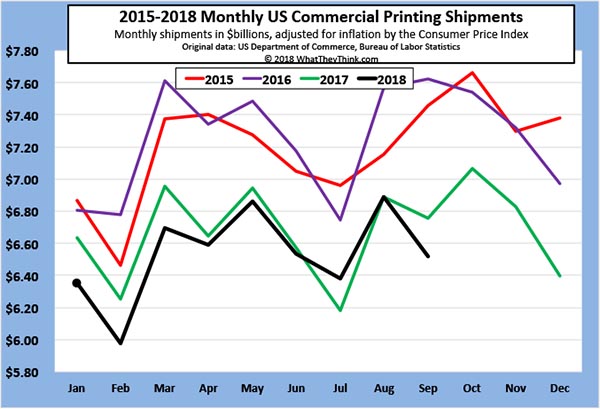

Shipments for September 2018 were down from August, and this is the second year in a row where September shipments have been down from August. As we always say, two data points don’t make a trend, but are we starting to see a new seasonal pattern? Or are we starting to see that there is no seasonal pattern? Certainly, print businesses that serve retailers have been remarking for a few years now that the concept of the “marketing calendar” is a thing of the past, with print work being more and more catch as catch can. Is commercial print in general going that way, as well?

Still, we had a good summer; August was the second time since 2016 that shipments for the month exceeded those of a previous year—but, well, we did indeed take a fall in September.

We are losing some of the ground we had been making up: on a year-to-date (January-to-September) basis, 2018 comes in at $58.8 billion, while 2017 January-to-September shipments came in at $59.8 billion (all dollars adjusted for inflation).

Next month, should we expect an “October surprise”? Will the traditionally biggest month of the year (to the extent that anything can be called “traditional” anymore) see a rise in shipments? How will this compare to previous years? And, perhaps most importantly, are comparisons to previous years starting to lose their relevance?

Mark your calendars! On Wednesday, December 12, from 2:00–2:30 p.m. EST, Dr. Joe Webb’s “Farewell Webinar” will cover these and other economic issues. Watch for a registration link as the date draws nearer.