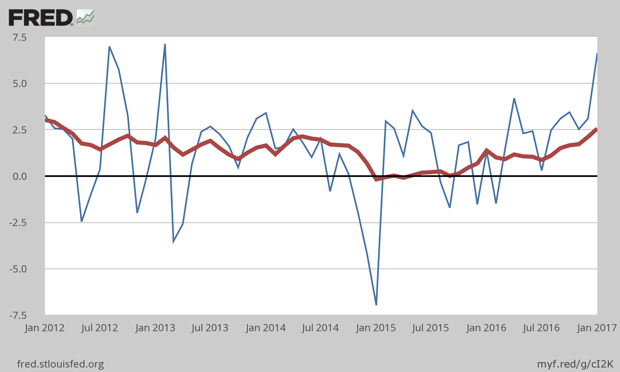

Consumer inflation for 2016 was increasing, with December’s reading +2.5% higher than 2015. December’s rate alone was at a +6.6% annualized rate. The chart shows the monthly comparisons as the blue line and the year-to-year comparisons as the heavier red line. The main reasons were gasoline and rent, with analysts also noting that food prices were declining. Good try, analysts!

Food prices had been rising higher than general inflation for most of the time since the December 2007 recession began, and are still much higher than that time. They don’t show any likelihood of falling all the way back to the CPI level.

Barring any catastrophe, it is very likely that the Fed will raise rates in March, sending markets into a panic as they realize they have to pay a whole 25 cents more to borrow $100. The increase is small, but markets will look at it as a sign that the Fed will no longer support the markets so generously. It’s likely that any increase will then put the Fed on hold until they see if Congress acts on a new tax policy. That would allow the Fed to raise rates as the economy improves from those policies. Otherwise, the Fed punch bowl will still be nearly full, but just 25 cents more. If there are no policies enacted to stimulate savings and investment, and the economy continues at its slow pace, these inflation data indicate the risks of stagflation may be rising.