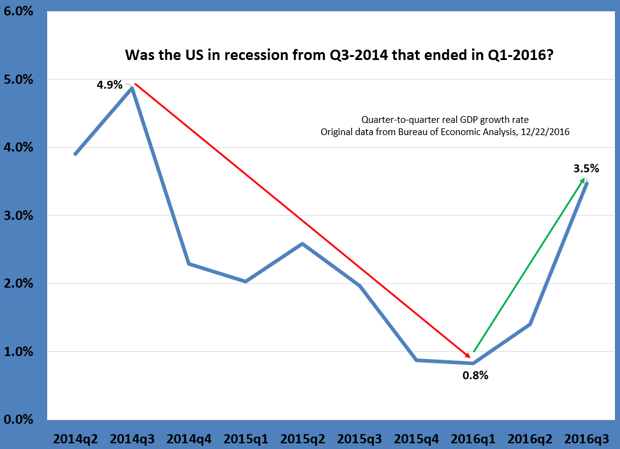

The Bureau of Economic Analysis released its third report of real Gross Domestic Product, at an annualized +3.5% over the second quarter. This is considered the final report, revising the advance report of +2.9% two months ago, and +3.2% in last month's preliminary report. This is important because each release of GDP data is based on increasing amounts of actual reported data. The advance report relies the most on estimates and models.

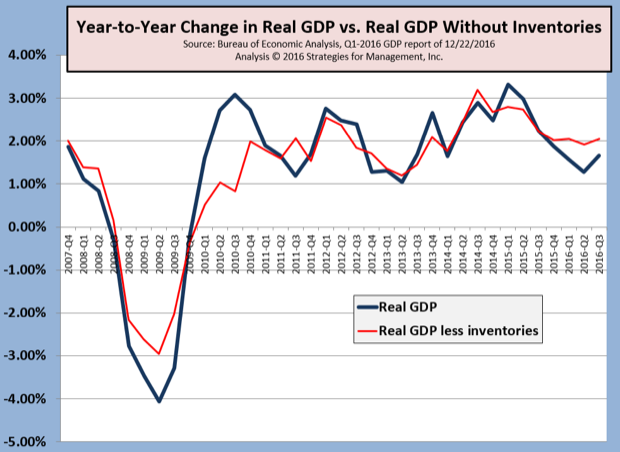

Readers know that we have great preference for the year-to-year reporting which smooths the data and shows long term trends. The revised report barely changed those trends, with real GDP running below +2%.

One of the distorting factors to GDP reporting is net inventories. By removing that, GDP seems to be right at the 2% level. What is interesting is that net inventories was small after the second quarter's negative net inventory value. Theoretically, net inventories should be zero as demand is satisfied by supply because the economy is able to use resources “perfectly.” That is not possible, of course, with many products having long supply chains, and negative net inventories are signs of the economy correcting itself. Last year, net inventories averaged $84 billion. The first three quarters of 2016 average only $12. That's a good sign.

Just because we prefer the year-to-year measure does not mean that we don't look at the quarter-to-quarter changes. Our chart shows something quite interesting: the economy's growth rate peaked in the third quarter of 2013 and weakened ever since. It bottomed in the first quarter of 2016 and appears to be improving. If this period was dated as a recession, it lasted six quarters with a recovery that has lasted six months.

Recessions are not dated as two consecutive negative quarters, but that rule of thumb is not so bad most times. The actual definition describes to a peak level down to a contraction or near-contraction.

The past actions of the Fed, such as the decline in interest rates and the expansion of their balance sheet, may have prevented a true recession but they also created a weight on economic growth. Recessions reallocate resources, but sluggish economies give mixed signals that delay the reallocation of resources to better uses. Perhaps this is a sign that the reallocation has finally taken place.

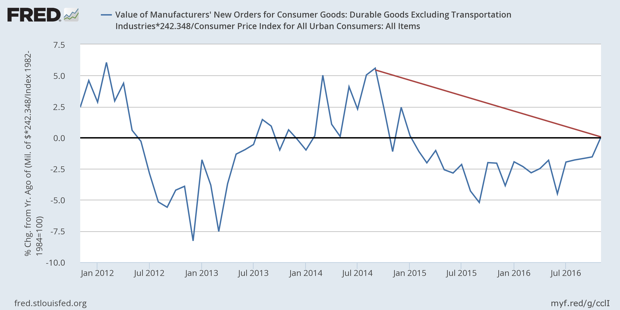

We've certainly had that on the manufacturing and investment side of the economy with negative year-to-year comparisons for more than a year. Consumer spending has been keeping GDP from being negative.

Durable goods adjusted for inflation by the Consumer Price Index shows a similar pattern, but slightly delayed, now turning barely positive after 21 months of negative comparisons.

The economy is not about to take off, so it's not reasonable to expect a big fourth quarter GDP. Any changes by the incoming administration and Congress require changes in law, and that can take time.

The issues are fully discussed in the Forecast 2017 report now available at the WhatTheyThink Report Store.