Global Bond Rates May Make it Hard for the Fed to Affect US Long-Term Rates

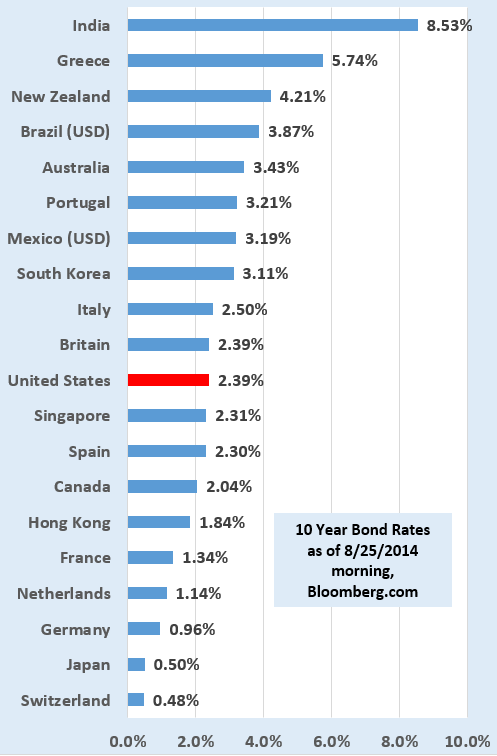

The Fed has been in unchartered territory with its post-2008 actions, and unwinding them may take a bit of creativity. One of their obstacles might be the rates of long term government bonds around the world. The chart below shows the yield of 10-year bonds earlier this week. The rate on US 10-year bonds is more than 4x Japan's and more than 2x Germany's. In an odd situation, US bonds are actually paying less than those of Spain. Global investors looking for yield (pension funds, governments, mutual funds, and others) may thwart Fed actions by finding US funds to be compelling deals on a relative basis. The Fed can usually affect only short term rates, which was one of the reasons they became aggressive in buying long term debt in their Quantitative Easing (QE) actions. Getting yields down for all durations is what made their actions were essentially unprecedented for the US. If they attempt to sell their holdings quickly to raise rates, there might be more buyers than they anticipate, making the action fruitless. It still looks like once the QE buying is done in the next few weeks the Fed will simply let their most of their holdings mature rather than force-feed them to the market. Listen for the word “macroprudential” in the next months. That's how Fed officials are describing the gentle prodding they may have to take to reverse their course. It turns out that some of the Fed members are worried their actions may encounter resistance, so they will resort to some arm-twisting to push banks to act in the manner they want. That hasn't worked well in the past, and it probably won't work well now, but it does add a word to our vocabulary.

The Fed has been in unchartered territory with its post-2008 actions, and unwinding them may take a bit of creativity. One of their obstacles might be the rates of long term government bonds around the world. The chart below shows the yield of 10-year bonds earlier this week. The rate on US 10-year bonds is more than 4x Japan's and more than 2x Germany's. In an odd situation, US bonds are actually paying less than those of Spain. Global investors looking for yield (pension funds, governments, mutual funds, and others) may thwart Fed actions by finding US funds to be compelling deals on a relative basis. The Fed can usually affect only short term rates, which was one of the reasons they became aggressive in buying long term debt in their Quantitative Easing (QE) actions. Getting yields down for all durations is what made their actions were essentially unprecedented for the US. If they attempt to sell their holdings quickly to raise rates, there might be more buyers than they anticipate, making the action fruitless. It still looks like once the QE buying is done in the next few weeks the Fed will simply let their most of their holdings mature rather than force-feed them to the market. Listen for the word “macroprudential” in the next months. That's how Fed officials are describing the gentle prodding they may have to take to reverse their course. It turns out that some of the Fed members are worried their actions may encounter resistance, so they will resort to some arm-twisting to push banks to act in the manner they want. That hasn't worked well in the past, and it probably won't work well now, but it does add a word to our vocabulary.