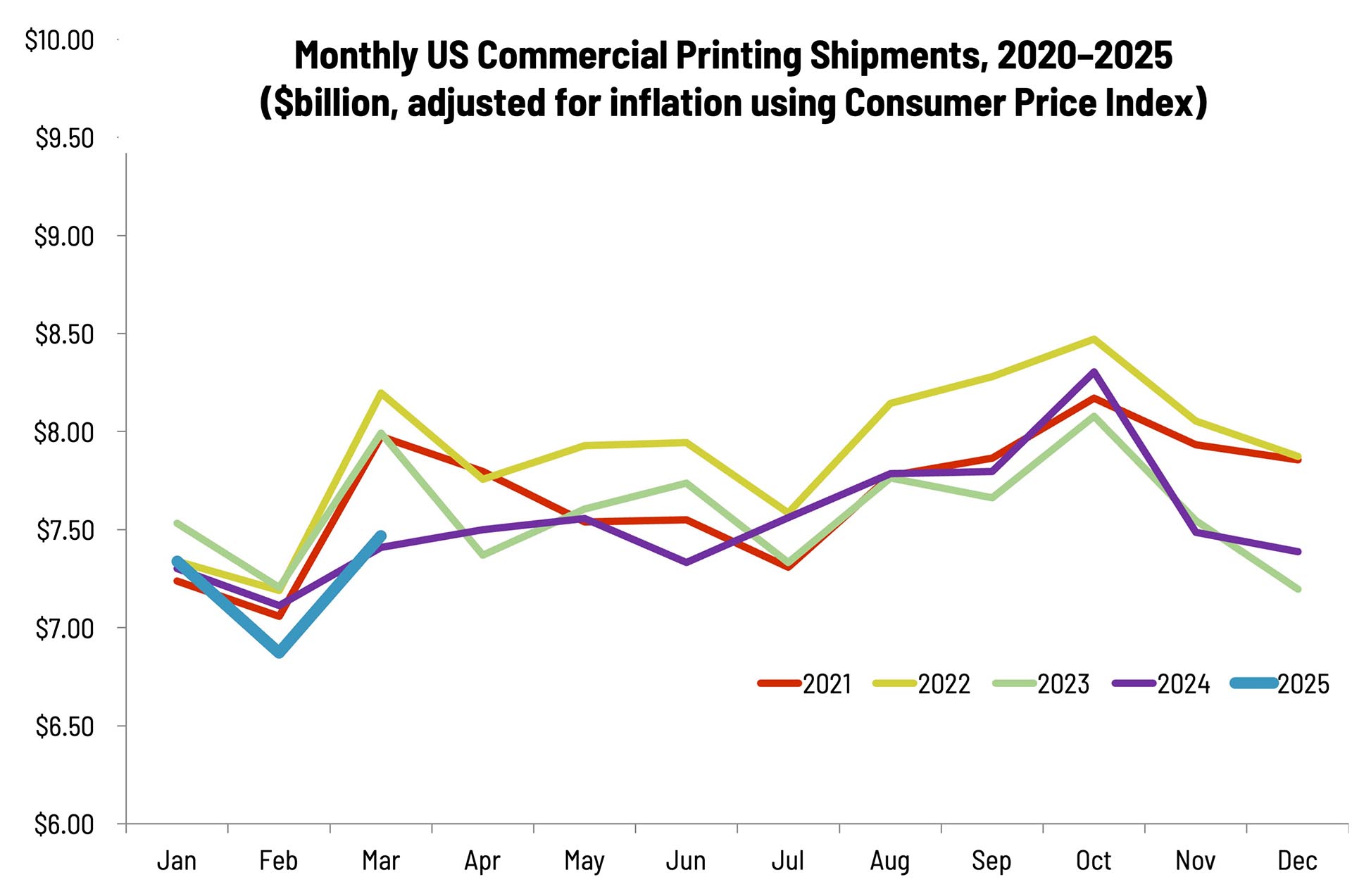

We’re a little behind on our shipments reporting, which is just as well, as February was perhaps the most dismal month in the history of printing shipments—dipping below $7 billion for the first time…ever. February is usually a slow month, but good grief! Happily, shipments rebounded in March, and at least surpassed March 2024’s shipments. We started the year off pretty well, so there’s reason to be optimistic that February may be as bad as it will get. (As we saw last week, Q1 GDP declined, so everyone was having a bad time in Q1.)

As we mentioned when we reported on January shipments, this data is still from before the recent tariffopalooza and “uncertainty” became the order of the day. So how it will play out—macroeconomically and within the printing industry—is still anyone’s guess at this point. On the plus side, the Atlanta Fed’s GDPNow is currently tracking Q2 GDP growth at +2.3%, so even though we’re only halfway through the quarter, it’s still encouraging.

We said last time that, since shipments lag two months, “we may have a couple more ‘calm’ reports before any turmoil shows up in the data”—although February was anything but a calm report. Again, let’s hope that’s as bad it things get, but we’re likely in for a rocky next few months.

Our Printing Outlook 2025 report is now available. Find out how print businesses fared in 2024—and what we’re likely to see in 2025.