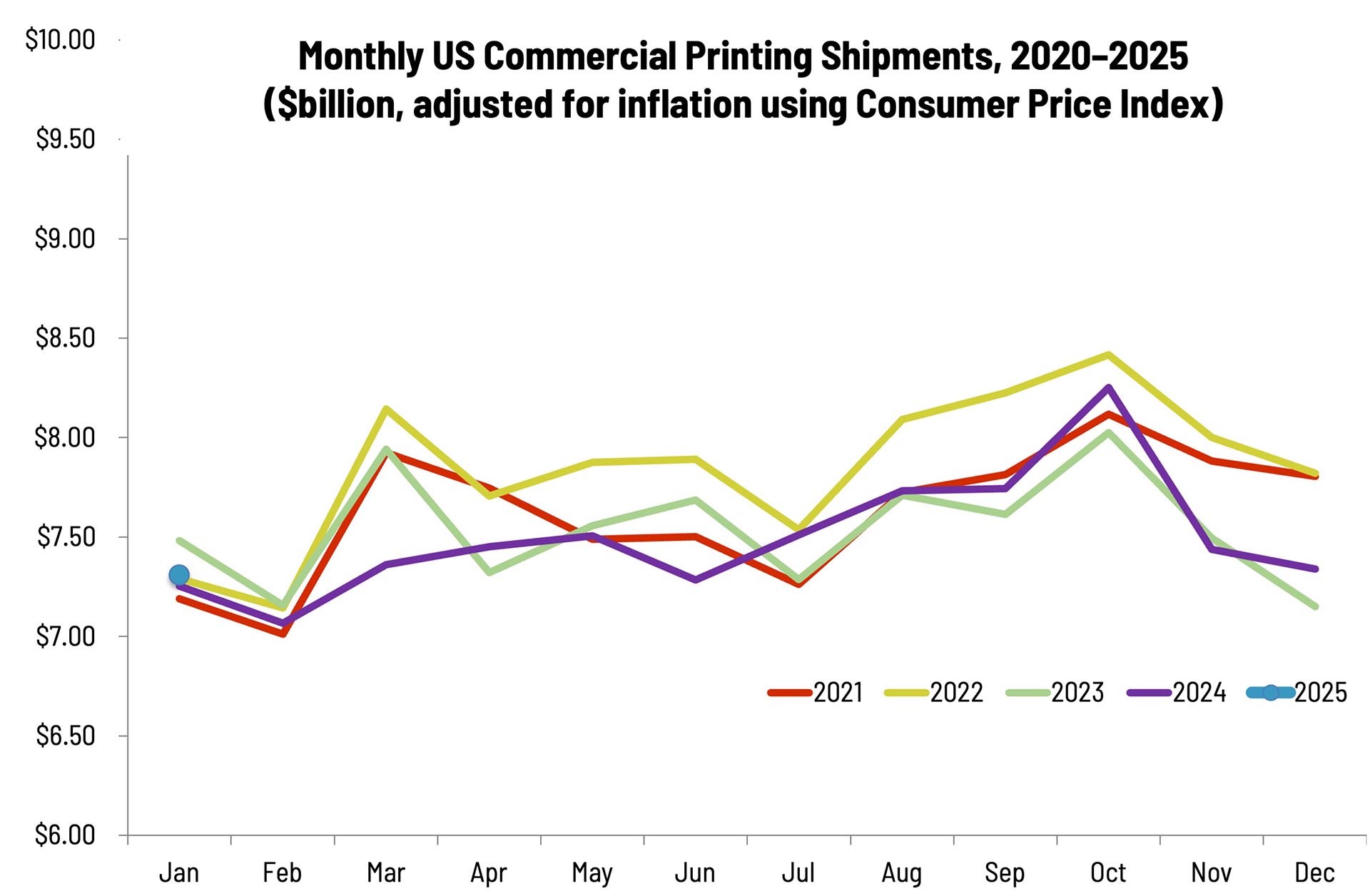

The value of printing shipments dropped slightly from December 2024 to January 2025, from $7.34 billion to $7.31 billion. However, it was the second best start to the year since the pandemic. That’s the good news. The bad news is that this data is from well before the recent tariffopalooza roiled the markets. How the uncertainty will play out—macroeconomically and within the printing industry—is anyone’s guess at this point, and many economists’ teeth are grinding like tectonic plates. Are we headed for the “r” word? One of our go-to sources for economic analysis—Calculated Risk—is on “recession watch” but is not predicting a recession thus far. Regardless, none of what is happening is going to help with what was one of the biggest problems of the post-pandemic period: rising prices. This doesn’t necessarily affect the value of printing shipments—except insofar as price pressures throughout the economy make other businesses increasingly likely to cost-justify their print-buying—but it does impact print business profitability.

Shipments lag two months so we may have a couple more “calm” reports before any turmoil shows up in the data—and hopefully it won’t, or will at least be minimal. But we’re likely in for a rocky next few months. Strap in.

Our Printing Outlook 2025 report is now available. Find out how print businesses fared in 2024—and what we’re likely to see in 2025.