Covid in the Rear-View Mirror, Finally

Over the past 13 years, we have chronicled, logged, and commented on the merger and acquisition activity in several print-centric business segments, with special attention to commercial printing, packaging (labels, folding cartons, and flexible packaging), wide-format, and direct mail companies. At the end of August each year, rather than focusing on the prior month’s deal activity, we take a look back at the past twelve months. If past is prologue, and to a reasonable extent we believe it is, then we hope to provide a high-level macro perspective on what the deal activity tells us about where the industry is headed. Which segments have experienced more, or less, deal activity? What are the trends in the buyers’ rationale to complete these acquisitions? Are acquirers adding facilities to their networks, or opportunistically folding acquisitions into their existing facilities? What does all this tell us about the potential future transactional activity within each print segment?

At the end of August every year, we review, categorize, sort, count, and chart the data we have collected, comparing the trailing twelve months (“TTM”) with the same period of prior years.

During the Covid years, we extended our look-back time frame to bridge the pandemic. We thought that the longer time period was necessary, and used 2019, the pre-Covid year, to provide a benchmark across the chasm created by the shut down, so that we might know when the market has returned to normal. In our M&A practice at GAA, we have finally reached the point where we no longer have to do mathematical somersaults in order to extract the impact of Covid from our analysis (well, not entirely, there are still PPP loans and ERC credits salted into many financial statements, but less and less as each month goes by). The Covid years of 2019 to 2021 are fading into the distance in our rear-view mirror, and we have returned to our pre-Covid practice of a three-year comparison in most of the charts presented here.

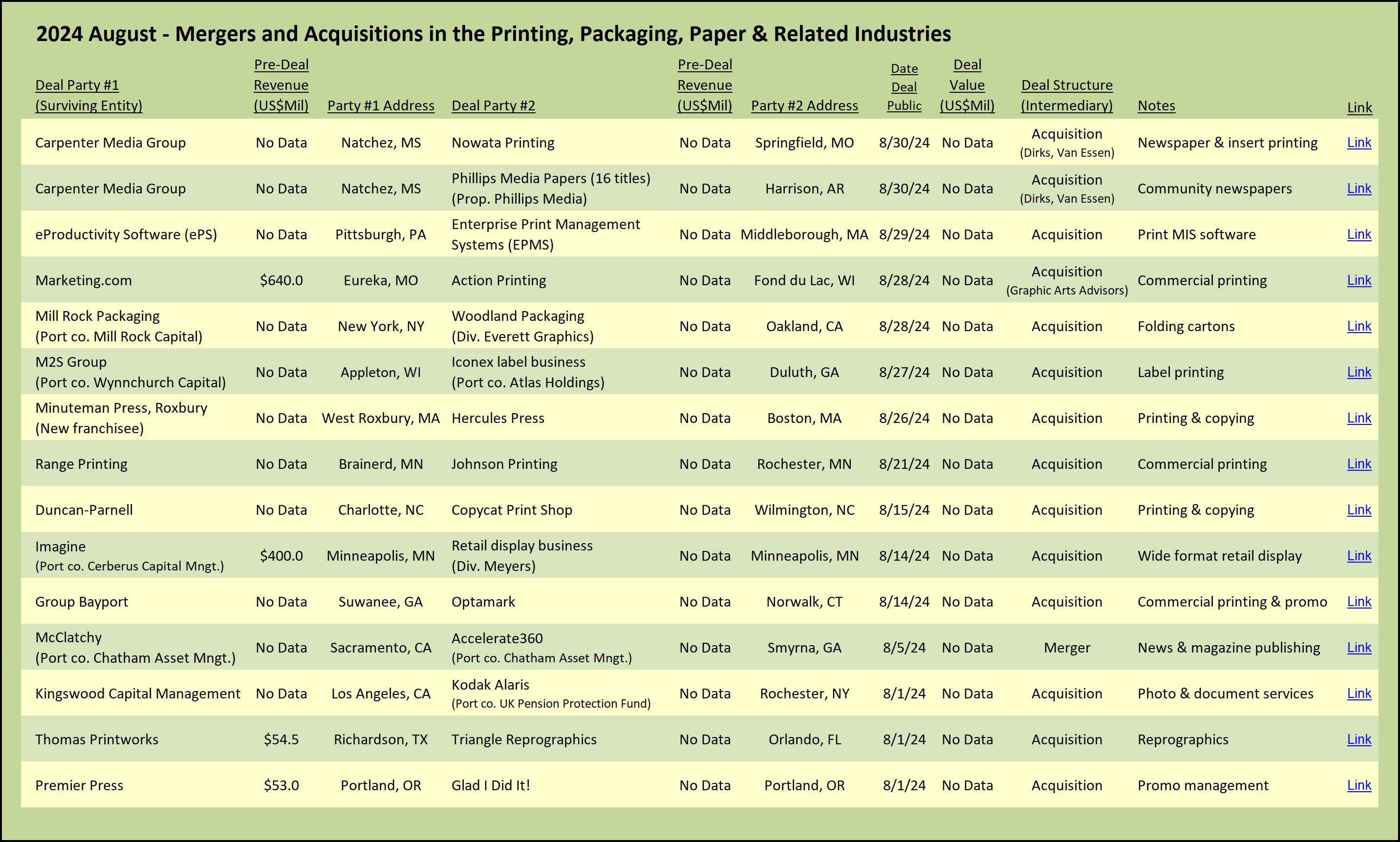

In pure numeric M&A terms, deal activity during the past twelve months was off 5.0% from the prior TTM period, which was in turn off 10.0% from the prior year. We identified 189 transactions of interest during the past twelve months; the lowest number we have tracked in any period since we began counting for our annual reviews in the autumn of 2016.

Last year at this time, the big question was whether the economy could ease its way down from the euphoric post-Covid bulge in demand. We noted that the classic signs of turbulence were in abeyance, and it appeared that the economy, and therefore by extension the printing and packaging segments, might navigate the turbulence and nail the elusive soft landing. We noted last autumn that not all was well in our industry, however, as paper manufacturers and distributors announced deals that further consolidated the industry. Some paper mills closed, and other mills converted from printing to packaging grades, portending another possible tightening of the paper market in the future. (See The Target Report: Is a Soft Landing in Sight? – September 2023.)

With the year behind us, as we head into the autumn of 2024, it appears that the US economy has in fact managed the soft landing. However, there are some bumps on the landing runway that indicate not all is well. The data noted below about bankruptcy filings and non-bankruptcy plant closings indicate a bumpy ride for some. We hear from many owners, but not all, in all printing segments, across the country, that there has been a softening of demand. At GAA, our special situations practice, in which we assist owners of financially challenged and highly distressed companies, has been unusually busy for most of 2024.

We are often asked what time of the year is the best time to go to market and when are buyers likely to close on deals? Historically, deal activity tends to drop off every year as we head into the summer months. This year was an exception. Although deal activity was off a bit overall this year, on the basis of a three-month trailing analysis, the announcements kept up a fairly steady pace throughout the past twelve months.

![]()

The chart above shows total counts of publicly announced M&A deals and provides a general view of the industry. The printing industry is not monolithic and in order to understand the market better, for the past thirteen years, we have categorized all the deals logged by the segment in which the acquired company primarily operates. We then dig deeper into the packaging, commercial printing, direct mail, and wide-format printing businesses, seeking to understand the rationale behind each deal, and gestalt the results by segment. We also analyze bankruptcy filings and non-bankruptcy plant closings to determine in which segments the business challenges are most pronounced.

The next chart breaks down the M&A transactions over the past three years into all the segments we track in The Target Report.

![]()

Commercial Printing

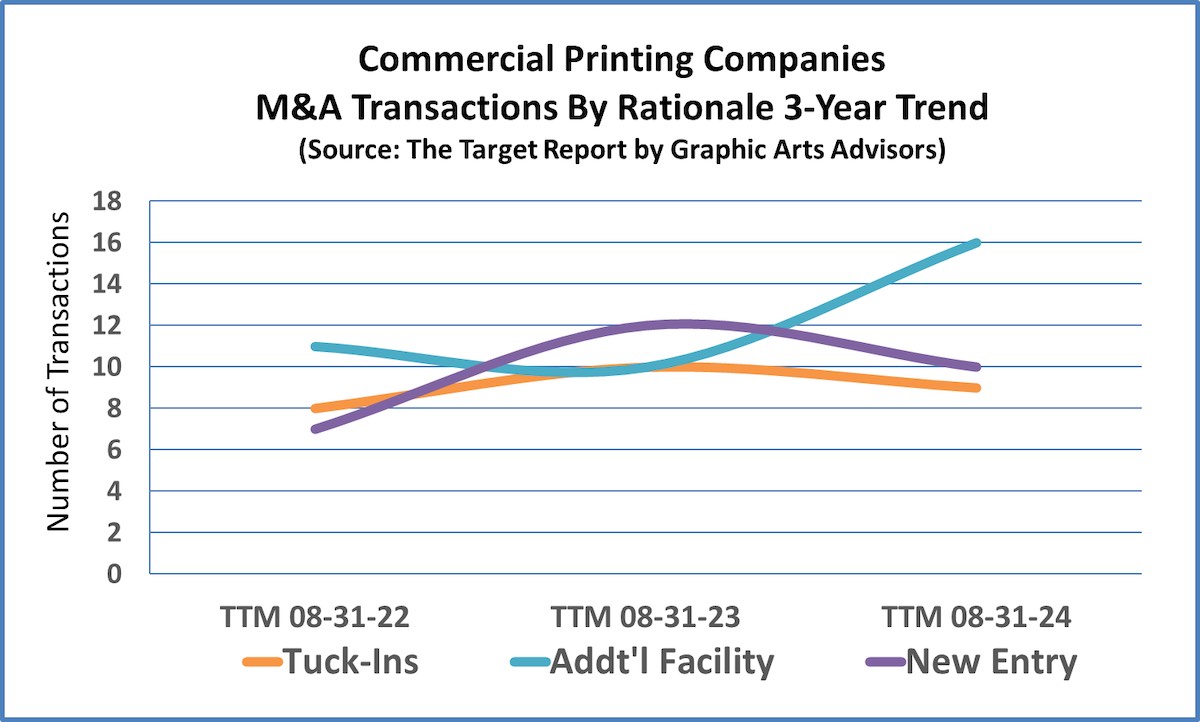

Our annual deep dive into the rationale behind the transactions in the commercial printing segment suggests that the commercial printing business has been reasonably stable, you might even say a bit upbeat. The percentage of deals that were structured as tuck-ins dropped to an all-time low of 25%, in contrast to a high of 70% back in 2019. In these tuck-in transactions, the customers of the acquired company are transitioned to the buyer’s production facility. Buyers will often leave the disposition of the plant and equipment to the seller, or to the seller’s agent, avoiding responsibility for trade and other debt, and possibly cherry-picking certain equipment that is needed or desirable for the smooth continued servicing of the acquired customers. In our opinion, a higher percentage of tuck-ins is indicative of overcapacity and financial stress, with the consequential result that there were fewer buyers willing to acquire an operating company within that segment of the industry.

There were 26 acquisitions in the commercial printing segment where the acquired facility was important to the buyer and will remain in operation, as-is-where-is. Sixteen of these buyers acquired the target company to add a location, with the stated goal of keeping the plant operating, the opposite of the tuck-in strategy. Notably, the other ten of these were sold to “new entry” owners that were not previously invested in the commercial printing industry. This is in stark contrast to the number of transactions in commercial printing that were completed by new entrants in 2019, only two. Clearly, something has changed: outsiders are once again interested in, and more important, they are investing in the printing industry. The idea that printing is dead is dead.

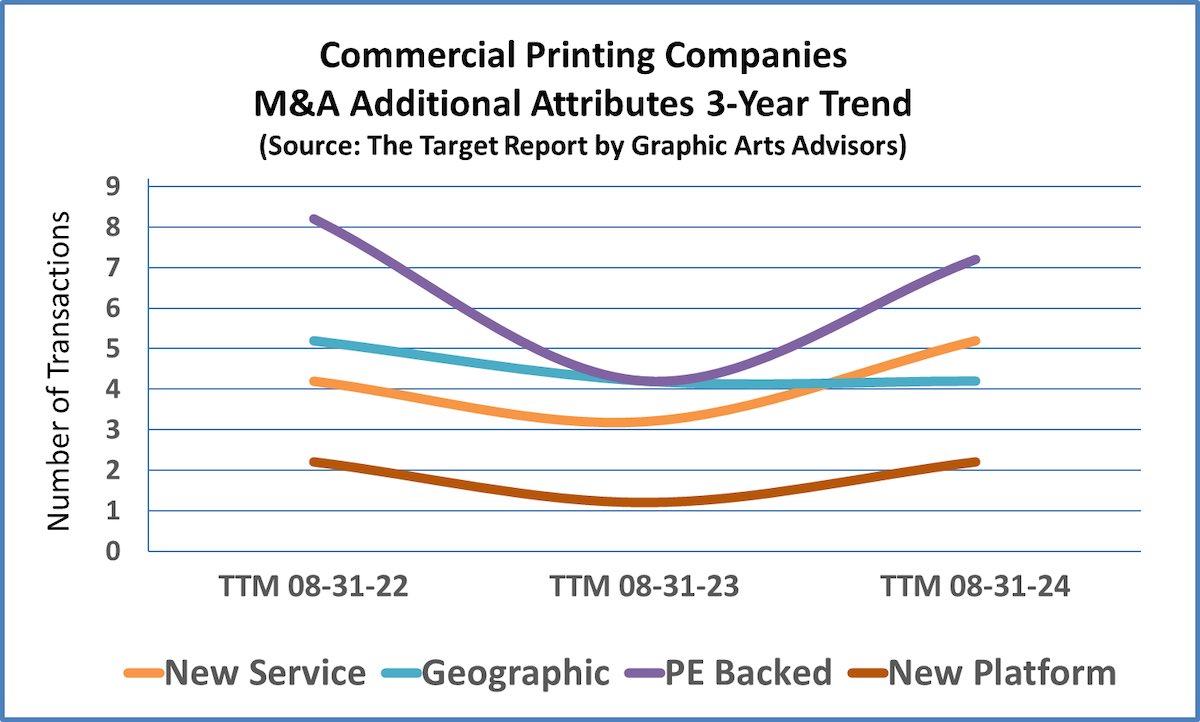

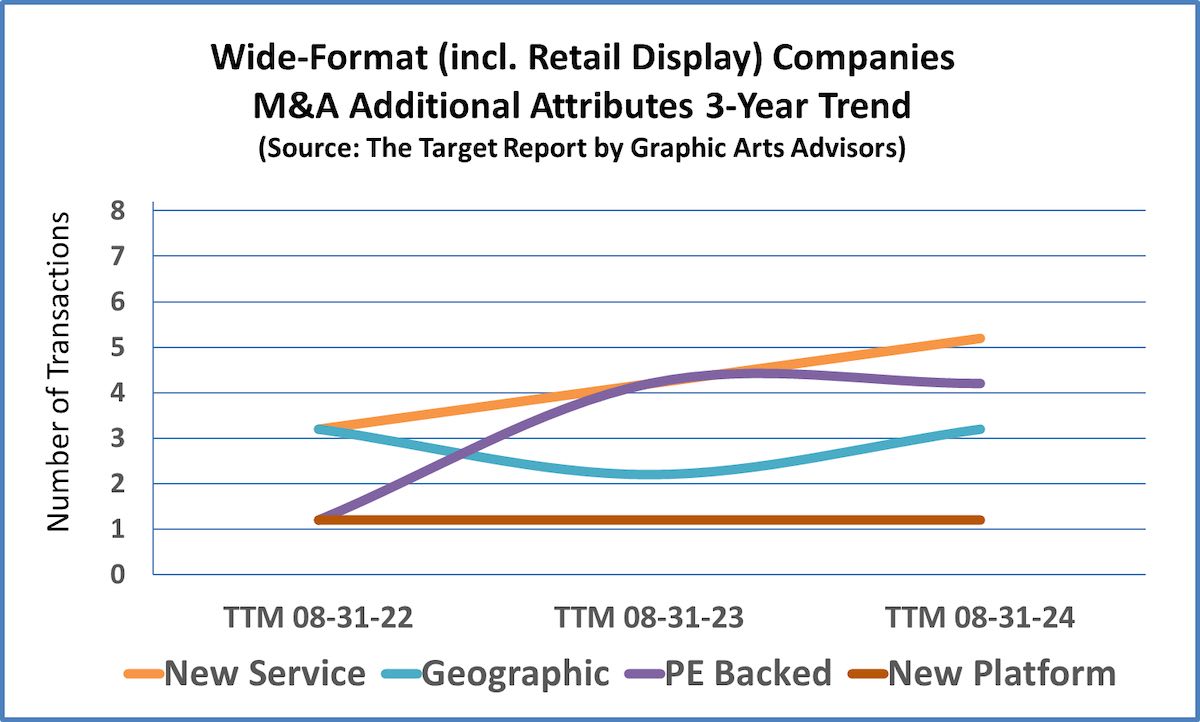

Digging a little deeper, we looked for instances in which buyers cited geographic expansion and/or adding new services as the rationale behind their acquisitions. We also noted whether a private equity sponsor was involved.

Adding a new service offering edged out expanding the company’s geographic footprint as the most often cited reason for completing a transaction. Adding wide-format was a common reason, while a couple were non-printing companies that added commercial printing.

Many owners we talk with in the commercial printing segment have told us that their companies did quite well in 2022, and that positive performance continued right up to the third quarter of 2023. That started to change as the fourth quarter of 2023 rolled into 2024, and we have been told by many owners that they have adjusted to a new normal, which is off from the go-go year of 2022. We hear even less about labor issues than we did last year, however some owners note that finding well-trained operators is still a common problem, especially for analog machines. We hear almost no complaints about the paper supply and most companies have worked off the excess inventory that was purchased at inflated pricing. We also hear from owners that their company’s customers do not accept price increases with the ease experienced when paper supplies were tight. (We hear similar comments across the various printing and packaging segments, not just from commercial printers.)

After a quiet period at the beginning of 2024, owners that had put their exit plans on hold are now back in the market actively seeking a buyer or preparing for a sale process. The average owner in the commercial segment is older, and having survived the turbulence of the Covid period, many are deciding to bring their company to market. Rather than commit to another round of capital equipment spending with its related long-term debt, many owners are opting to cash out.

Our candidate for the most interesting transaction in the commercial printing segment during the past twelve months was RR Donnelley’s huge jump into the free-standing insert business with the acquisition of the Vericast business (See The Target Report: Half a Loaf is Better than None – March 2024.)

Packaging

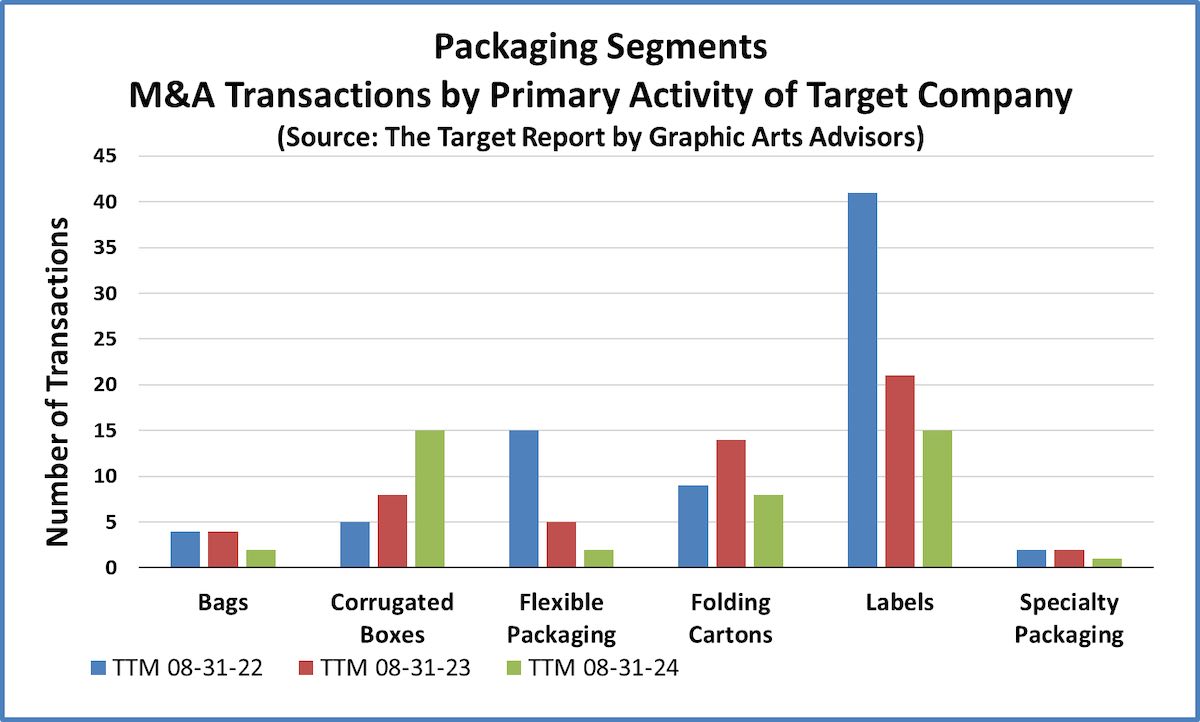

For the third year in a row, the packaging business is again the most active among the segments we track. However, consistent with the reduction in overall deal activity, we found 26% fewer publicly announced transactions in the packaging segments we track. The red-hot market for label printing companies has continued to cool off and is now matched by the number of transactions involving corrugated packaging.

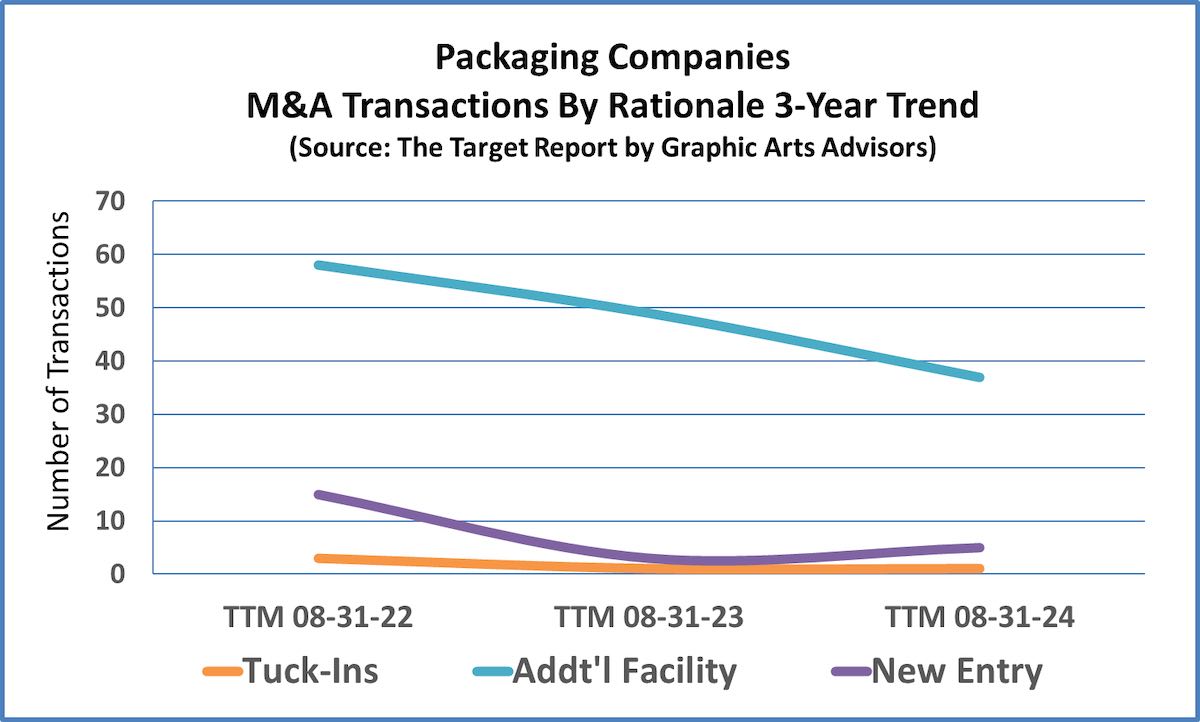

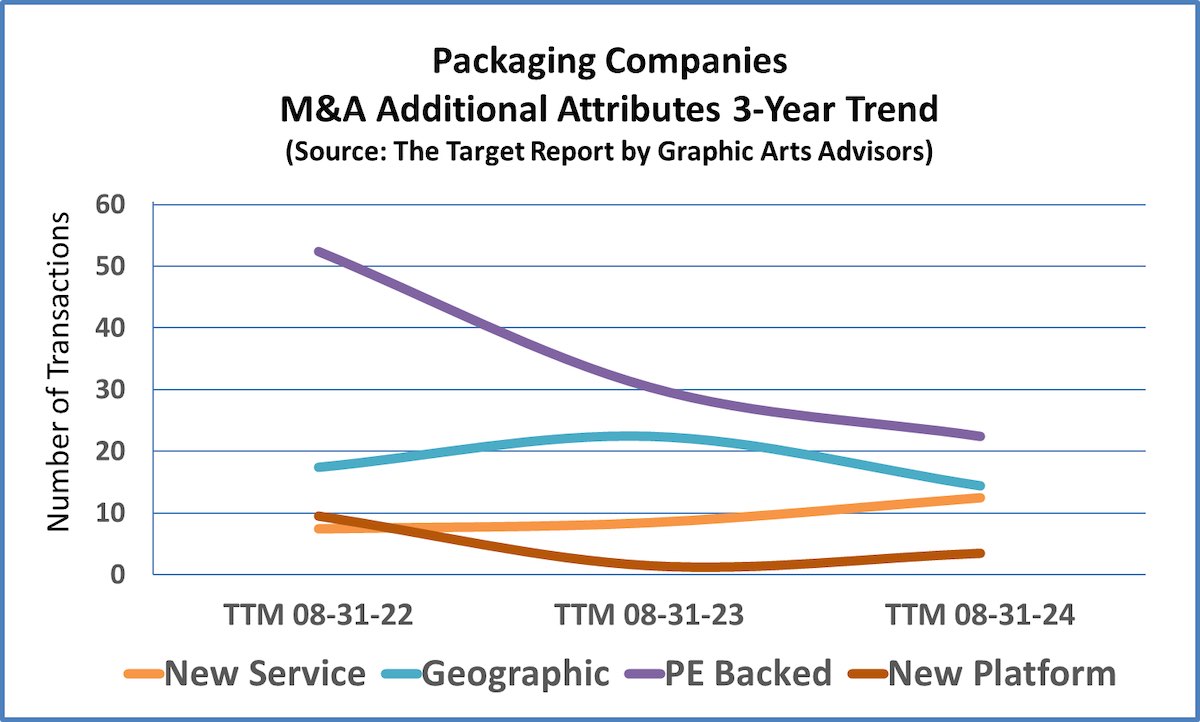

Owners and investors in the packaging industry tell a very different story than those in commercial printing, when they talk about their rationale for completing an acquisition. Of the 43 transactions that we recorded over the past twelve months in the packaging segment, only one was reported to be a tuck-in and that was the consolidation of an older folding carton plant into a nearby existing operation that has capacity from the divestment of its non-packaging business. Similar to all prior years, the majority of the buyers noted that the acquisition of an additional production facility was the critically important reason to complete the deal. Furthermore, the expansion of the company’s geographic footprint was mentioned as very important to the buyer.

Private equity was involved in 22 of the 43 total transactions in packaging, 51% of the total. In absolute terms, private equity’s decrease of eight transactions accounted almost entirely for the total decrease of deal activity in the packaging segment. Five new players entered the packaging business, three of which established brand new investment platforms in packaging.

In 14 instances, geographic expansion or diversity of the acquired locations was noted as a key element in the buyer’s logic. An expanded geographic footprint continues to loom large in buyers’ expressed logic for completing acquisitions.

Our candidate for the most interesting transaction in the packaging segment during the past twelve months was not one specific deal. Rather, the intensive interest in the corrugated box business by players big and small, regional, national and global, proved of interest to many readers of The Target Report. (See The Target Report: Corrugated Consolidation – June 2024.)

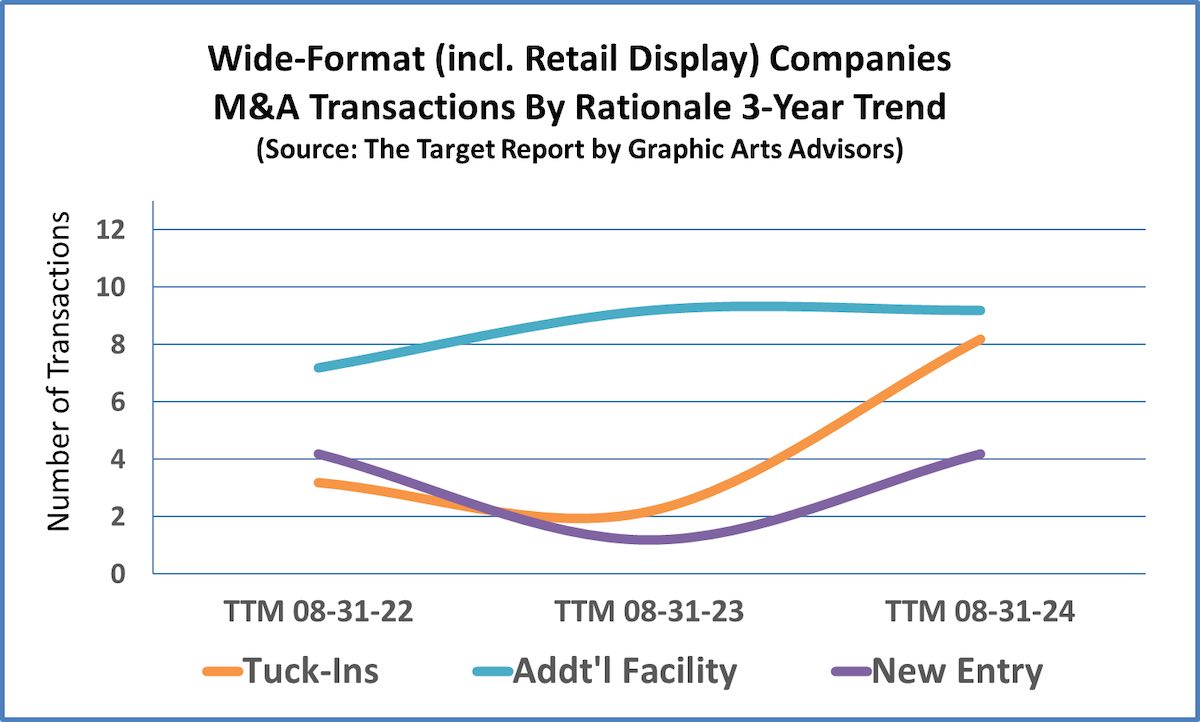

Wide-Format and Related Digital Products

For our purposes in forming a picture of the various market segments that comprise the overall print-centric industries, we separate out companies that produce mostly wide-format and related products from the more generalized commercial printing segment. We include retail display and trade show graphic production in this category, as well as reprographics, indoor architectural environment graphics, and home décor products produced on wide-format equipment.

As we have noted in prior Target Reports, the salad days for wide-format printing are over, and the maturation shows in the transactional activity. Digitally printed banners and wraps are no longer unique, flatbed printing devices are ubiquitous, and the high margins that came with being an early entrant offering large inkjet prints have been compressed by competition. Entry-level equipment is no longer expensive, flatbed cutters and other finishing technology are widely installed. Differentiation in the wide-format business has moved from those that had first-mover advantage to businesses that have perfected more complex online direct-to-customer systems, robust planning and installation capabilities, or value-added services such as printing on canvas for use as home or office décor (and even these attributes are no longer sufficient to provide unique differentiation).

The wide-format business has matured. Company owners are following a path long ago traveled by commercial printing companies; growth via acquisition, driven mostly by the stated desire to add a production facility. What is new this year, and a certain sign that the segment is reaching saturation, is the significant increase in the number of tuck-in transactions.

We noted 21 publicly reported transactions in the wide-format segment during the past twelve months, close to double the number we found last year. Private equity remains active in the wide-format segment, which leads us to expect that deal activity will remain robust over the next several years.

Our candidate for the most interesting transaction in the wide format segment during the past twelve months was Meyer’s back-to-back announced transactions, the acquisition of Johnson Printing & Packaging, followed shortly thereafter by the divestiture of its temporary display and signage business, which it sold to Imagine. The CEO of Meyers noted that the sale “reinforces our commitment to focus on, and grow, our core business strength of packaging and labels” which was clearly demonstrated just two weeks prior with the addition of the Johnson folding carton business. The dual transactions were a classic demonstration of using M&A to advance a strategic plan to fundamentally change a company’s position in the marketplace.

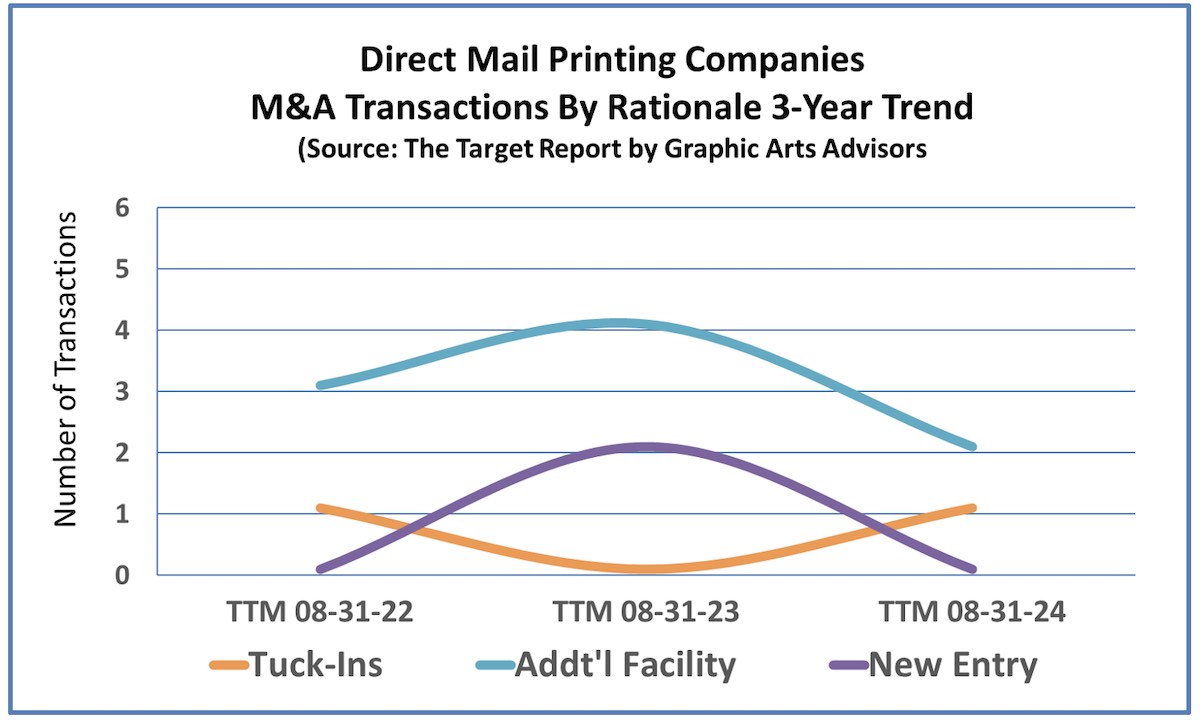

Direct Mail

In our lexicon and analysis, direct mail printing companies are in a class by themselves, apart from the more generalized undifferentiated “job-shop” commercial printing companies that may offer some mailing capabilities. Many direct mail shops also manage, manipulate, store, and utilize data to drive improved results for their customers. Some have expanded into full-service marketing support companies, blending digital communication channels with mail campaigns.

Transactional activity in the direct mail printing segment has fallen steadily over the past several years, with only three transactions noted this past year that we considered to be so purely involved in volume mail as to be broken out from the commercial printing category. The sample size is too small to draw any firm conclusions, but the decline is worth noting, as well as the inclusion of a tuck-in within the count. We also note that four direct mail companies filed for bankruptcy in the past year, double the prior highest number in a segment in which there are no bankruptcy filings in most years.

Two of the three buyers noted that the rationale for the transaction was to expand by adding a facility. One of those two noted an expanded geographic footprint as well. In one of the direct mail transactions, the buyer, the same one that was backed by private equity, mentioned adding a service element as their rationale to move forward with the deal.

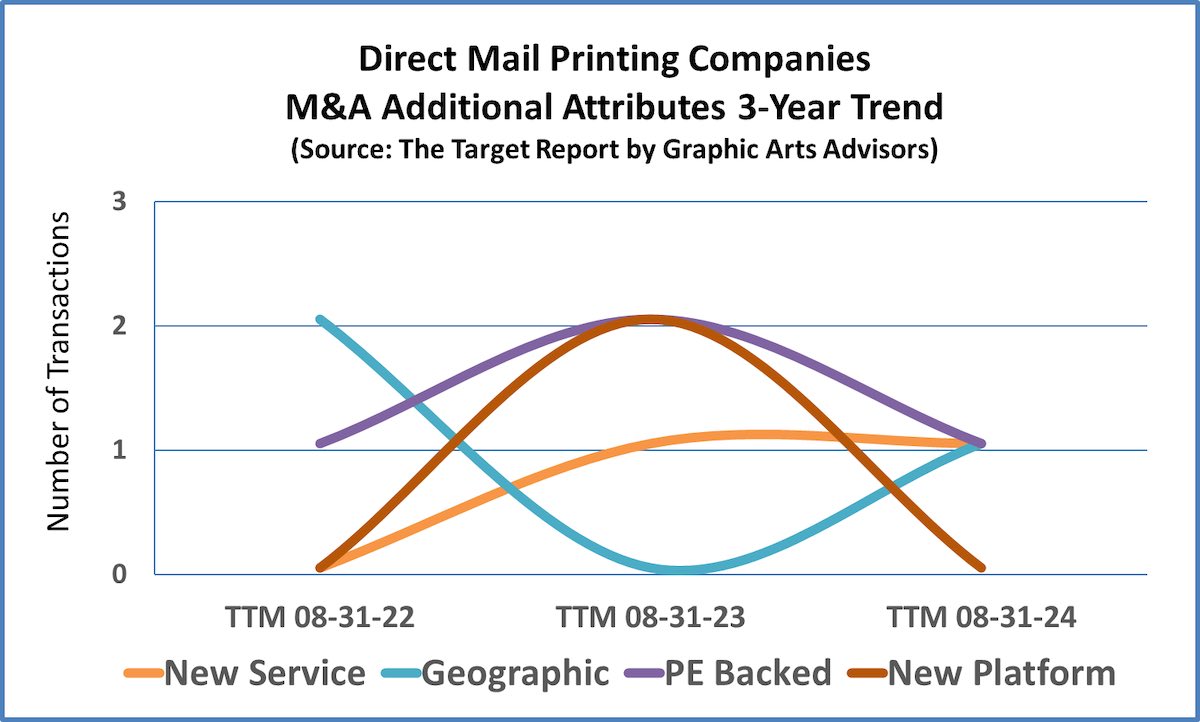

Our candidate for the most interesting transaction in the direct mail segment during the past twelve months was Ironmark’s simultaneously announced acquisitions of Deliver Media and L & D Mail Masters. These moves by the PE-back Ironmark brought data predictive analytics to their clients’ multi-channel marketing campaigns and at the same time expanded the company’s geographic footprint with a secure data management and direct mail production environment. These are the attributes driving acquisitions in direct mail today, moving upstream into data analytics, procuring secure certified facilities, and diversifying mail processing geographically.

Challenged Segments

The transactional activity in an industry segment tells us that the business is changing. However, the simple counting of deals does not tell us if that activity is indicative of positive or negative change. To determine a directional indication, we track the number of bankruptcy filings and non-bankruptcy plant closures and correlate this information with the overall transactional activity. Our thesis, born out over several years and confirmed by industry stats derived from other sources, is that an industry segment with a high number of transactions that is also experiencing closures and bankruptcies is, or will be, in a contraction phase. There will be opportunities for consolidation at bargain prices for those companies that defy the downward trend.

Conversely, segments in which the number of transactions is inversely correlated to closures and bankruptcies are more likely to be expanding. Therefore, consolidation opportunities will come at much higher prices. Virtually all the packaging segments are experiencing steady transactional activity, albeit fewer deals than in prior years, without the corresponding bankruptcy filings and plant closures, indicating that packaging remains a very healthy environment for sellers as the segment continues to consolidate.

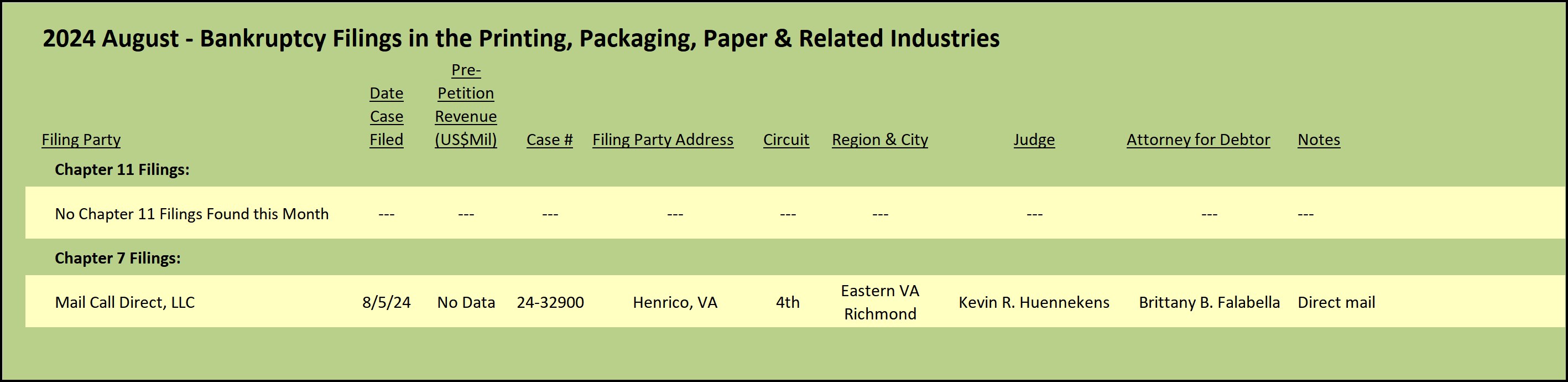

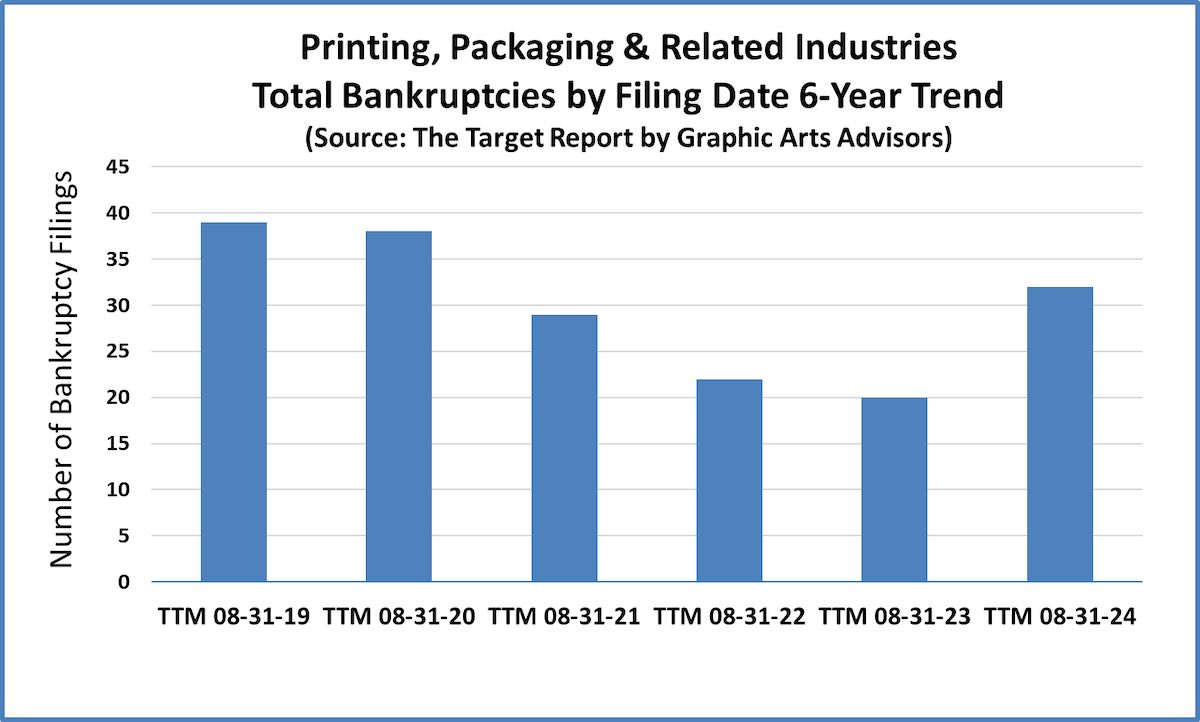

The data on bankruptcy filings is beginning to flash a moderate warning sign. Indicators of financial distress in our industry have mostly trended downwards over the past five years, but during the past twelve months that trend has reversed.

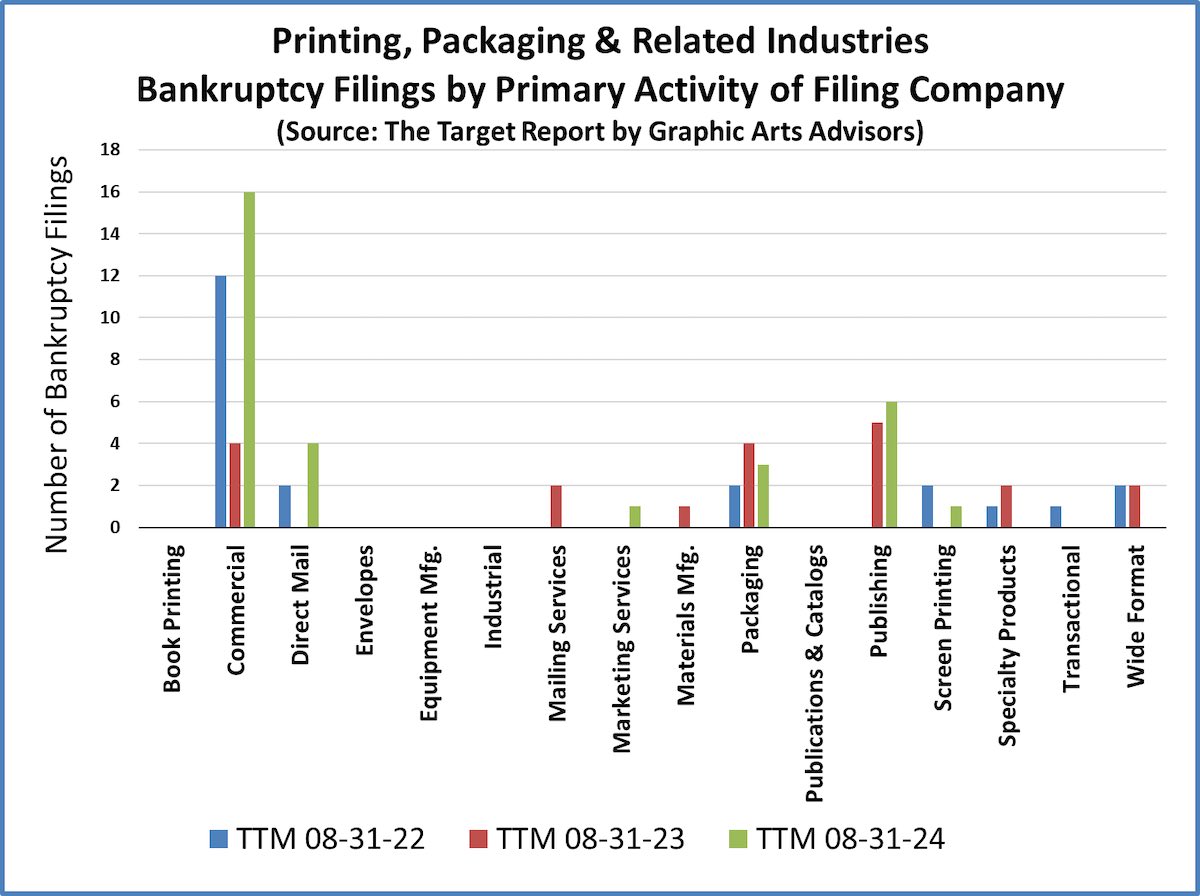

The commercial printing segment once again, after a one-year hiatus, retakes the ignominious position as the leader in the number of bankruptcies filed. Not surprisingly, the publishing of newspapers and magazines is now back in second place. Also notable is the four bankruptcy filings in the direct mail segment.

Our candidate for the most interesting bankruptcy filing during the past twelve months was the failure of a company that showed great promise in the embroidery business. The story is about the failure of Coloreel, the developer of technology that dyed white thread in real time to create multi-color sewn emblems without changing spools or using machines with multiple stitching heads. (See The Target Report: Troubled Times for Graphic Machinery Innovators – July 2024.)

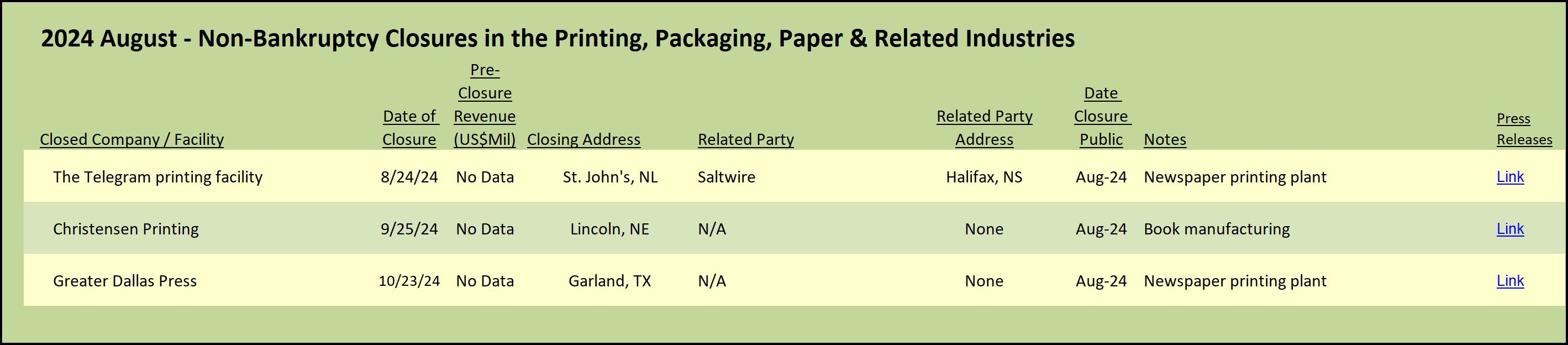

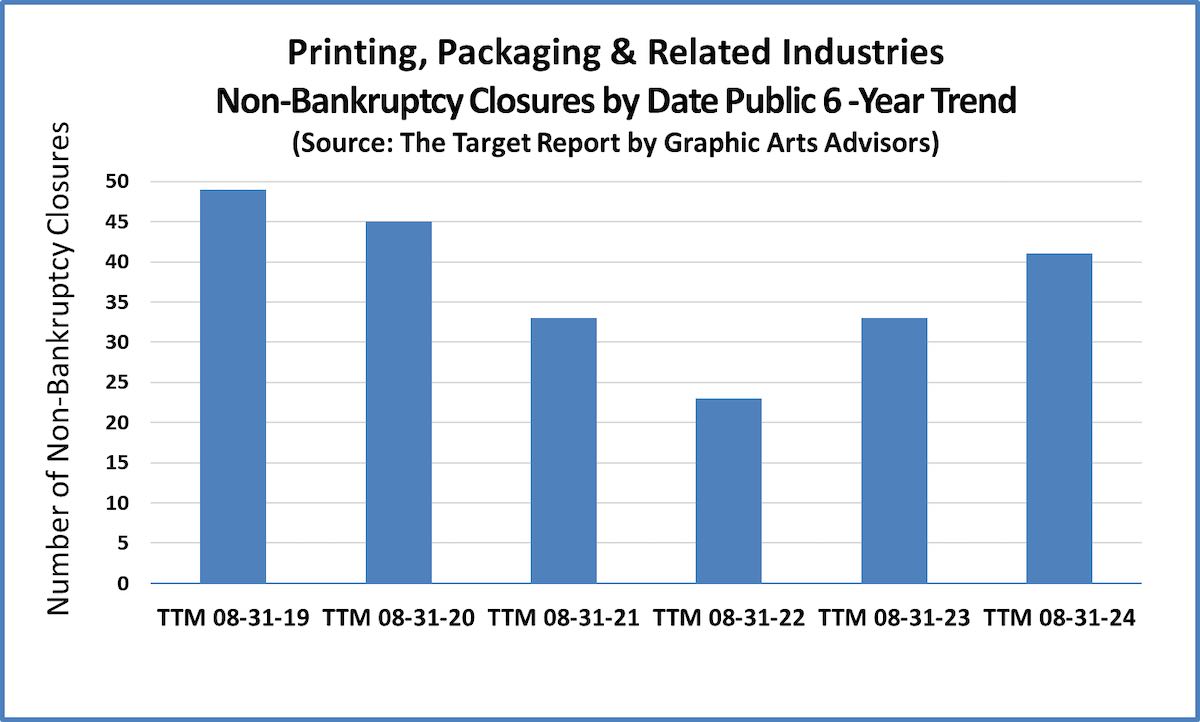

We also track non-bankruptcy plant closures as a good indicator of financial challenges within each industry segment, possibly even a more prescient predictor than the number of bankruptcies. At the lower end of the market in terms of business size, a bankruptcy filing can be the death knell for a company in the printing industry, and in any case, bankruptcy filings are expensive.

While some companies simply close up and just disappear, others find a buyer for the book-of-business and conduct an orderly wind-down process. A closure does not always mean that the company has ceased operating; a closure may simply be due to one of the larger printing firms rationalizing their production capacity. Either way, closures are indicative of change, usually resulting from downward pressure in a market segment.

The number of non-bankruptcy closures began to climb last year and continued that trend in the past twelve months. In absolute terms, we found 41 publicly announced plant closures during the prior year, once again approaching the numbers from 2019 and 2020.

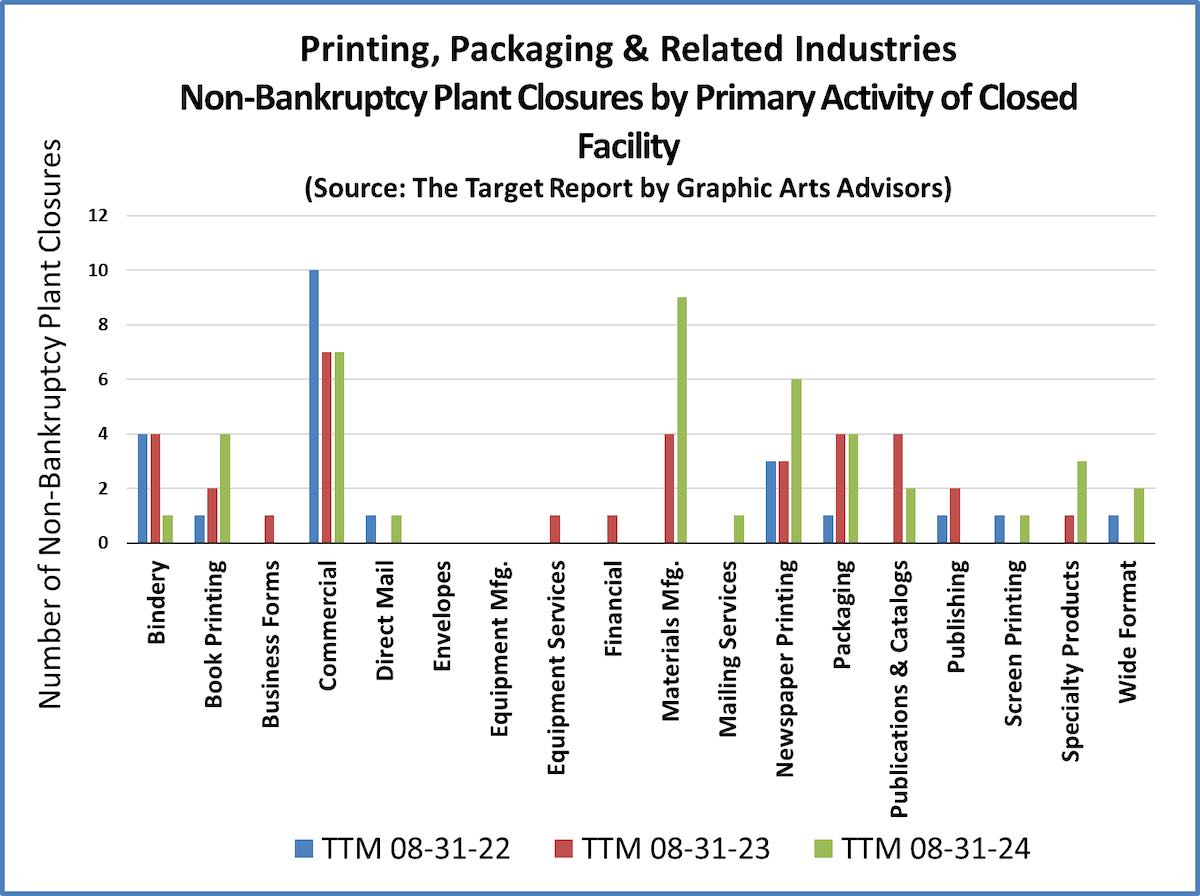

General commercial printing companies once again represent the majority of printing facilities closing up shop in a non-bankruptcy closure or wind-down. Newspaper printing plants also closed in greater numbers than most other segments. Paper mills continued to cease operations and close up, as noted in the materials manufacturing category in the chart below.

We will see, over the next year, if the slight rumblings get louder or the new normal is exactly that, a return to a normal level of transactions with occasional company failures sprinkled in. The trends we heard last year are still prevalent in our conversations with company owners; the money from the government largess has been absorbed, spent, or saved, loans are coming due for refinancing at higher rates, and print-buying customers are exercising price discipline. We will be watching and reporting as we enter our fourteenth year of publishing the monthly issues of The Target Report. Stay tuned.

View The Target Report online, complete with deal logs and source links for August 2023