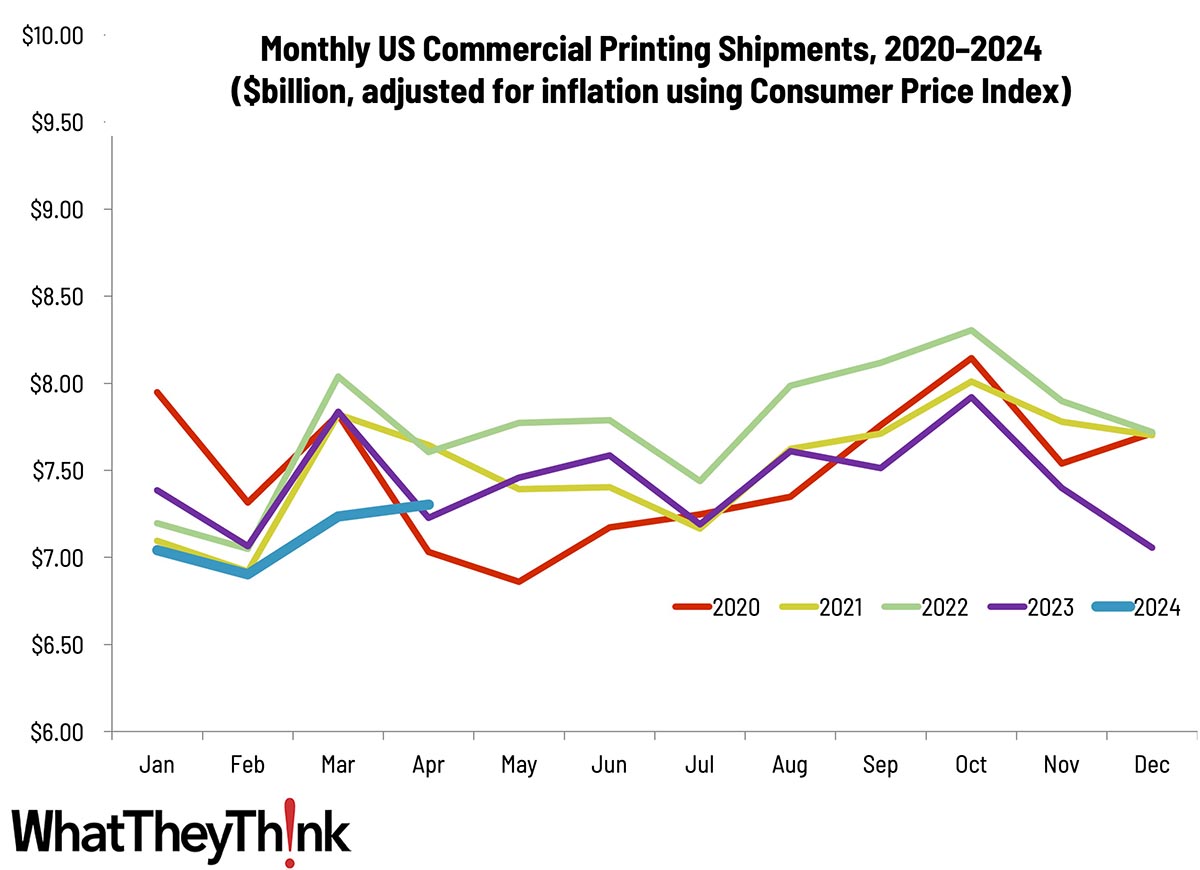

The last shipments report marked the worst March in the last five years, and in fact ever, and while normal seasonality prepared us for a doleful drubbing in April, it turned out to be not so bad. For the first time in (at least) the past five years, April shipments were up from March—from $7.24 to $7.30 billion, and a better April than last year. (It was also better than April 2020 but, well, that’s not hard.) Anecdotally, we know from our own mailbox that direct mail looks to have been up (and yesterday’s Keypoint Intelligence article cited a recent survey that found that marketers “were increasing the use of print marketing because digital marketing alone does not always produce sufficient response rates,” which could account for some of it) and 2024 being an election year there were primaries in the spring, which always spurs direct mail. May traditionally sees an increase from April, so we are cautiously optimistic.

Year-to-date shipments for 2024 are at $28.70 billion, a bit off 2023’s $29.51 billion. If we are hoping to have 2024 shipments come in above 2023’s, there is quite a bit of ground to make up. Can we do it?