Print industry revenues are subject to macroeconomic fluctuations and crisis happening from time to time. There was no crisis in recent history, however, that affected print production as much as the COVID-19 pandemic, when business activity almost came to a halt. Print production statistics indicated a 35% drop, with some recovery and fluctuations afterwards. While overall production statistics have been tracking volume developments in a relatively timely fashion, print application insight follows with some time lag. The German printing industry association (BVDM) recently published its 2021 print industry stats, which includes an overview of print application revenues.

In 2020, overall print revenues in Germany declined by 11.5% from €12.2 billion to €10.8 billion. In 2021, the market stayed exactly flat at €10.8 billion. While this might not have been the recovery we were hoping for, at least revenues stabilized and it should be kept in mind that parts of the shutdown lasted well into 2021. Overall, the graphic arts industry made a slight increase as revenues in pre-media and finishing grew to €1.378 billion, a gain of 3.4%, which followed a hefty decline of 12% in 2020 due to the pandemic.

It should be kept in mind that “non-classic” print producers like packaging, copy shops, in-house print, and data center print are not included in these numbers.

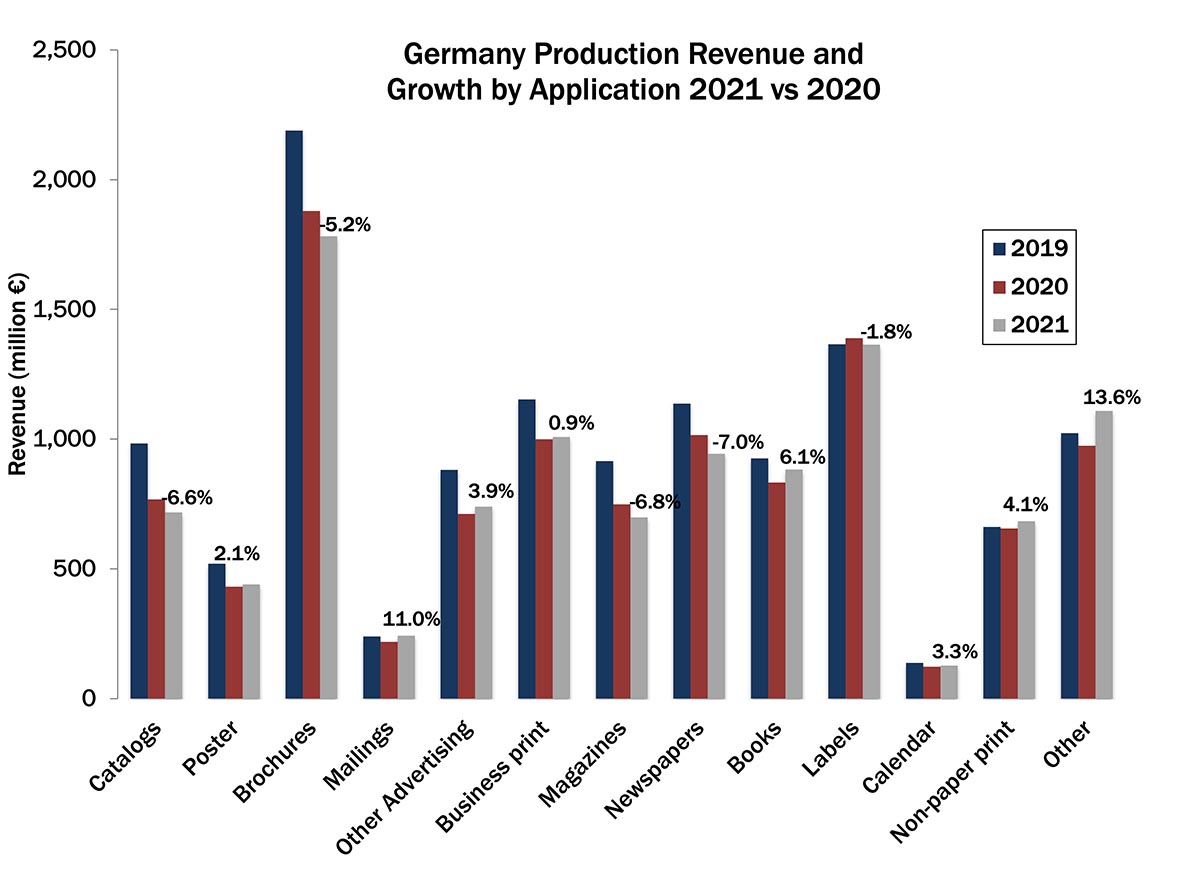

Since the printing industry is application driven, it is important to note that there has been quite some movement among print applications despite a flat top line number.

Source: BVDM Die deutsche Druckindustrie, 2021 & 2020

Advertising Offering a Mixed Picture

In the pandemic, advertising bore the brunt of the declines and advertising applications dropped by a total of 16.8% in 2020. Whole demand sectors going into lockdown took a big toll on advertising spending in 2020, while in 2021 businesses opened again—not always to the full extent, however. Overall advertising print declined by another 2.2% in 2021

Initially, it was expected that catalogs and mailings would have done better during a lockdown, considering that retail stores were closed and consumers spent more time at home. However, both segments dropped noticeably in 2020. It is a relief that activities in mailings resumed and revenues rebounded in 2021—grossing even slightly higher than in 2019. It is a good sign that marketers are (re)discovering the value of print, often as a complement to digital direct marketing.

Catalogs remained on the decline path they have been on for years now. While the market is still substantial, revenues declined by another 6.6% in 2021. This rate is even higher than the downwards trend seen in the years before the pandemic— typically an annual 2% to 3% decline.

Posters were hit hard by the first lockdown. Widespread restrictions on outdoor activity lead to out-of-home advertising effectively coming to a standstill. As expected, the market rebounded somewhat in 2021 with small growth of 2.1%. However, revenues remain noticeably below pre-pandemic levels.

Brochures continued with some decline but remain easily the largest print application in Germany. Again, a structural decline is continuing as electronic media remains a strong competitor. General “other advertising” rebounded and showed a 3.9% growth.

Periodicals

Newspapers and magazines are on a long-term declining trend and while information interest was high during the pandemic, the amount of periodicals printed and sold dropped sharply. The trend continued in 2021 although at a lower rate. Declines in the 7% range nevertheless show a higher decline rate compared to pre-pandemic years. It is likely that the pandemic accelerated the trend towards digital news and media usage. Newspaper print revenue in Germany dropped below the €1 billion mark for the first time in 2021

Books

Book revenues came in unexpectedly low in 2020, although comments by bookshop owners already indicated business losses during the lockdown. Overall book printing in Germany trailed many other countries in 2020. It seems that 2021 made up for that slowdown and helped to replenish stocks as well. A growth of 6.1% in book revenues is higher than the gain in book sales reported by the German book association. Still, book printing revenues remain 4.5% lower than in 2019. While book shops stayed open in 2021, a move to internet channels for book orders remained.

Labels and Non-Paper Print Staying Strong

Labels was the only print segment with growth in 2020, albeit a small one. It comes as a slight surprise that revenues dropped by the same amount again in 2021. Demand should have remained stable, but supply chain issues and delayed market introductions could have driven numbers down. A lack of available label stocks should have impacted revenues as well. Labels is the only portion of packaging print that is reported as part of the BVDM statistics.

Non-paper-based print did relatively well in 2021, as it has in recent years. This indicates an ongoing trend of revenue moving away from “classic” print applications into all kinds of specialty and niche print.

Other Segments

Although under the radar of many industry observers, business print is a sizeable application and ranks fourth by revenue. After a strong drop during the pandemic, with wide-ranging restrictions on business activity, the segment rebounded with a plus of 0.9%. This is the more remarkable as many digital alternatives emerged for business documents. However, users still find value in paper-based products. Calendars, a rather small segment, did grow as well after a 2020 drop.

Unfortunately the “other print” category is not detailed further, although it constitutes the third largest segment by revenue and showed a strong growth of 13.6%. Again, the ongoing trend to specialty applications is driving revenues and printers are finding new purposes for print. Unfortunately, long ranging timelines for the “other print” and “non-paper print” categories are not available, as they have been added only recently, hence the growth trajectories are difficult to quantify.

Moving Into a Post-Pandemic Print World

The German print industry data does represent the peculiarities of the German market, although it can be expected that application trends are similar in many countries.

As mentioned before, 2021 results are still impacted to some extent by the COVID-19 pandemic, although conditions normalized compared to 2020. 2022 will be the first year lockdowns and COVID restrictions play almost no role. Businesses reopened, travel resumed, and trade fairs took place again. Unfortunately, 2022 is plagued by other issues, such as supply chain interruptions, lack of transport, and especially high paper and energy costs and limited paper availability.

As communication and media usage habits are changing, many print applications are impacted. The pandemic accelerated some of those trends. It looks like the paper crisis will have a similar accelerating effect.

Still, even for declining applications, print volumes are huge. Furthermore, there are growing print applications. As the data shows, many growth applications target non-traditional markets, where print is adding value or is difficult to substitute. Not all of these markets are included in the numbers above. Packaging and some specialty print applications like photo print, merchandising print, and décor are produced, at least partially, outside the classical reporting of print industry data.