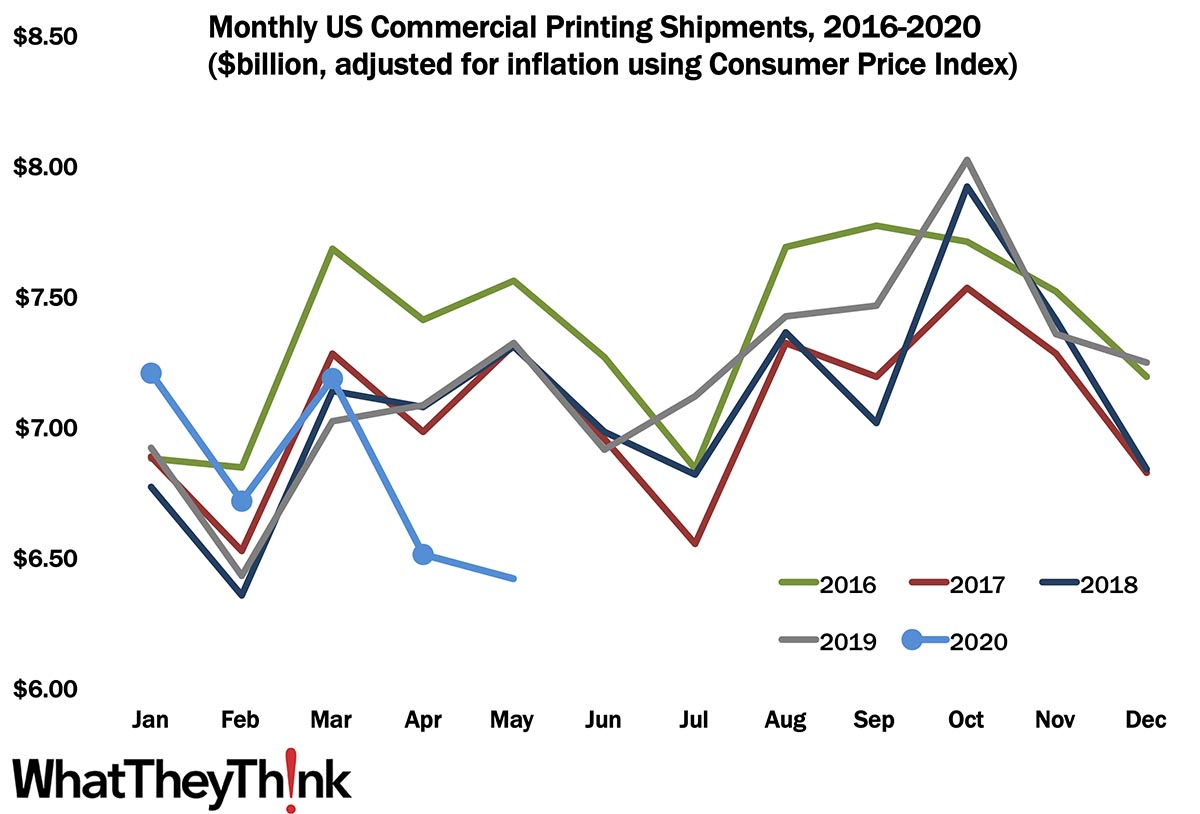

Well, on the plus side, at least we were expecting it... Printing shipments for May 2020 came in at $6.42 billion, down from $6.51 in April and way down from $7.21 billion back in January. On another plus side, it’s still not as bad as February 2018, and back then we didn’t have a global pandemic causing the problem. The natural seasonality to shipments that had been evolving over the past several years is pretty much out the window at this point, so it’s hard to get a sense of what to expect from month to month except on a “businesses are reopening/reclosing” basis. In June, we saw a lot of places start to reopen as the virus was more or less under control (such as in the Northeast), so we have a sense that June shipments data will be up—maybe not dramatically, but not inconsequentially. Hope springs eternal. We may even see an uptick in July, but the big worry now is that as infections spike dramatically in other parts of the country, will businesses need to close again?

We said back in March and April at the start of all this that if we got the virus under control by June or July, we might be able to pivot back to something approaching normal. Unfortunately, we failed to even remotely get the virus under control, and now we run the very real risk that August or September will be the new March. People were predicting a second wave of the pandemic in the fall, but it’s clear that we are still at the crest of the first wave.