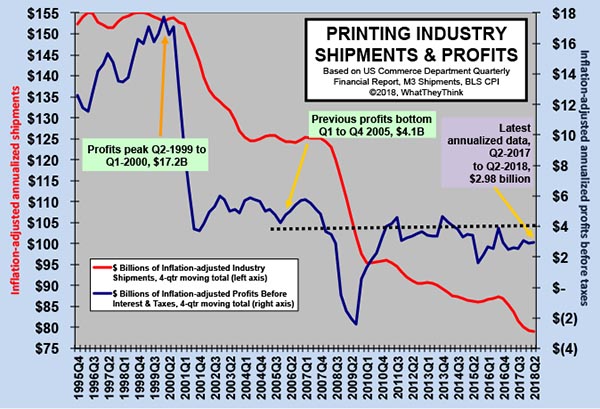

Looking at the most recent industry profits data that came out earlier this week, we continue to tell the “tale of two cities.” In Q2 2018, for the industry on average, profits before taxes were 6.15% of revenues, and for the last six quarters, they’ve averaged 4.16% of revenues. However, averages don’t always say what they mean (as it were). Digging down, we get a better picture of what’s going on beneath the surface. For large printers ($25+million in assets), profits before taxes were 3.60% of revenues, and for the last six quarters they’ve averaged 1.23% of revenues. But look at the “non-large” printers (<$25 million in assets): their Q2 profits before taxes were 8.77% of revenues, and for the last six quarters averaged 7.26% of revenues. This disparity between the “two cities” is not a new story; it’s something we have been seeing for the past couple of years: low profitability of the large printers is dragging down average industry profitability. (In much the same way that if a printing industry writer entered a room of hedge fund managers, the average income in the room would drop substantially.) So for the industry as a whole, cracking $4 billion in profits is proving to be an elusive goal.

On the plus side, Q2 2018 is the first quarter since Q3 2017 that the large printers had a net profit rather than a loss. So there’s that. The cost of investment (for large printers, interest expense was 4.6% of sales, compared to 0.78% for the non-large printers) remains a burden on businesses whose capital investments and acquisitions have not matched the demands of the market. Smaller shops have generally invested more prudently, and quickly adopted digital technologies, putting them in a position to more nimbly adapt to changes in the marketplace.