With pandemics, energy and supply chain crisis, and war in Ukraine, multiple predicaments hit the printing industry in recent years. It is tough to gauge the current impact on the printing industry from anecdotal testimony, however. Unfortunately, full industry data for most European countries is published with a two to three-year delay only by Eurostat. The only pan-European source of short-term industry statistics is the monthly production index. The index tracks volume developments in a number of industries, including the printing industry.

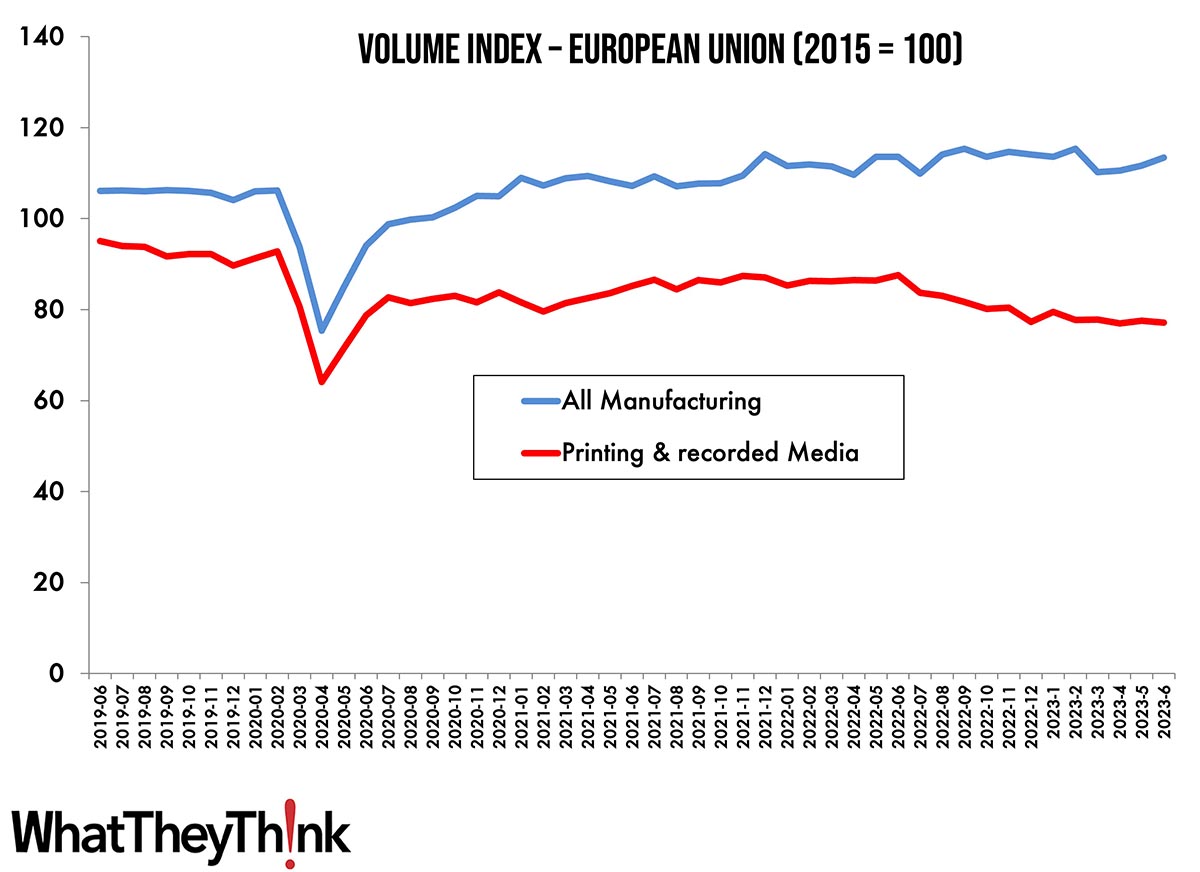

Production index data (with 2015 as a base year) for all manufacturing in the EU shows the enormous dip at the onset of the COVID-19 pandemic followed by a steady recovery. Pre-COVID-19 levels were reached again at the end of 2021. The following months did bring little gain, however. In the last 12 months, up to the latest data point from June 2023, the production volume in all manufacturing industries in the EU remained essentially flat.

Printing and reproduction of recorded media started lower at the onset of the chart, a sign of print falling behind the manufacturing average in the years between 2015 and 2019. Print showed a similar dip at the onset of the pandemic and a recovery in production volumes until mid-2021. However, volumes did not reach the pre-COVID-19 level again, remaining almost 7% below that level. Output remained steady from mid-2021 to mid-2022 with some decline following. In the last 12 months leading up to June 2023, the print production volume in the EU declined by about 12%. It seems that with some delay the effects of rising paper and energy are trickling down into print buying and result in lower print volumes now. In comparison, the effect of paper shortages in 2021/2022 had almost no effect on total volumes.

Source: Eurostat, 2023

The data does show production volumes and not pricing, disregarding the effect of rising prices in print. Revenue declines should be more moderate accordingly.

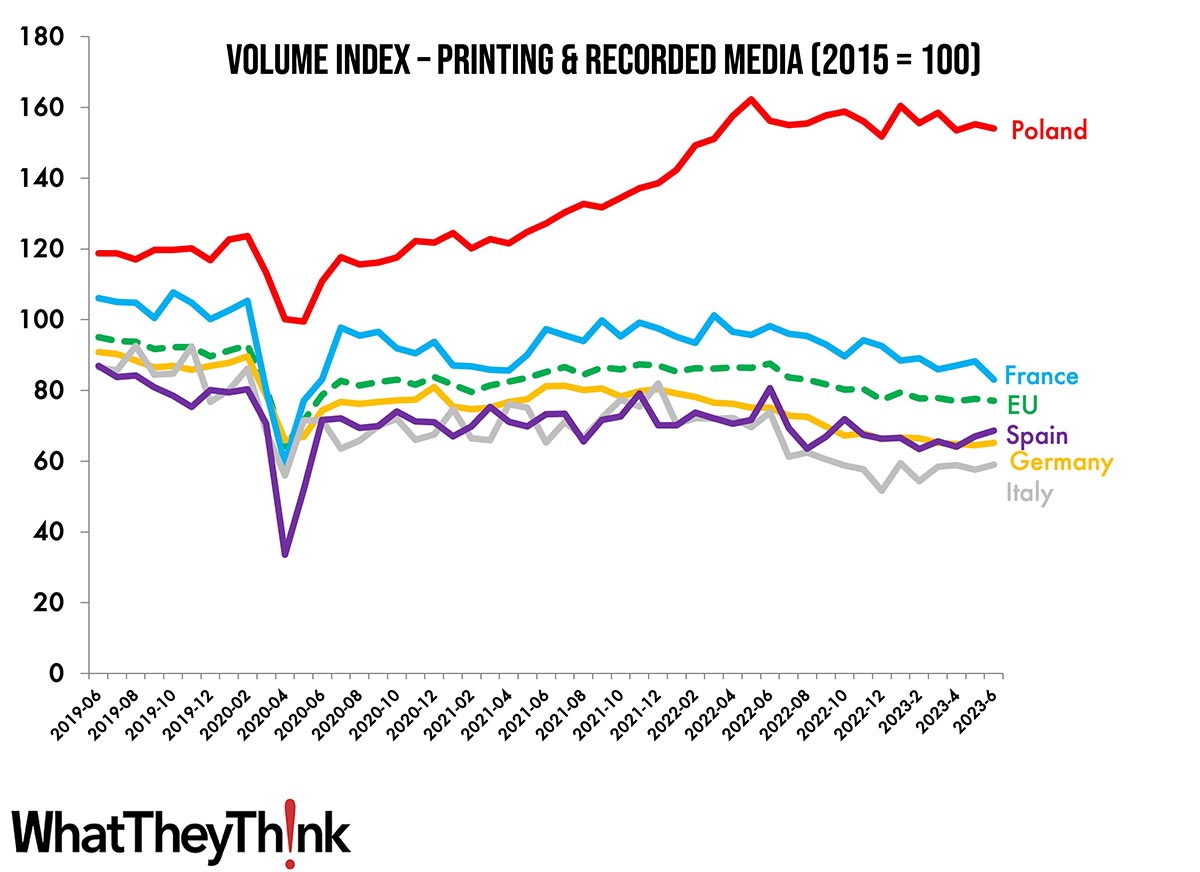

There are differences among the EU countries, however. The chart below indicates the most important countries in terms of print volume, compared to the EU average. Germany, the country with the largest print revenue in the EU, performed less favorably than the EU average. At the end of the post-pandemic recovery, volumes remained about 12% below the pre-pandemic volumes. The last 12 months did see another 13% decline in volumes. Production index data stabilised in the last couple of months pointing to a steadier demand—at least for the time being.

Italy fared even worse. Although production volumes recovered to 13% below the pre-pandemic level as well, the last 12 months brought another drop of 20% in volumes. Traditionally the printing industry in Italy is export-oriented and the data suggests that some of the volume travelled East, for example to Poland. Poland is the only country among the big five to surpass pre-pandemic production levels. By early 2022 volumes were about 30% higher than pre-pandemic. Since spring 2022, volumes remained essentially flat, however.

Volumes in Spain developed in a similar pattern to the production index in Germany, with a recovery to about 13% below pre-pandemic values. In the last 12 months, volumes declined by 15%, with volumes remaining flat since late 2022. With relatively low print volumes in the base year 2015 of the production index, France had an index value above 100 before the onset of the pandemic. After the dip at the start of the pandemic, volumes recovered to about 7% of the former values. Similar to most other countries volumes dipped by 15% in the last 12 months, while numbers in France still seem to be trending downwards.

Source: Eurostat, 2023

Most Western European countries show a similar development with volumes only recovering to a level noticeably below the pre-pandemic output and some additional volume declines in the last 12 months. Some exceptions exist, with Austria and Portugal doing better than the average. Eastern European countries typically were able to recover or even grow volumes until 2022 and volumes in most countries did show little declines afterwards—a sign of print volumes shifting towards Eastern Europe due to lower labor costs. Unfortunately, the UK does not report data to Eurostat anymore.

The data displayed is based on Eurostat numbers for printing and reproduction of recorded media, with the latter only contributing a tiny fraction. As the data is seasonally and calendar adjusted, variations during the year are already accounted for and should not affect the index values. There are some fluctuations to be reckoned with, however. The print volumes consist mainly of commercial and publishing printing volumes, including prepress and finishing companies. That means that packaging, data centre, direct mail print or quick print/copy shops are not included or only on a limited basis. In-house print or CRDs are not included at all. The EU data excludes Norway, Switzerland, and the UK. If you have questions about sizing the European printing industry or need clarification, please contact me at [email protected].

Our regular country-by-country look at turnover and employment will continue with Switzerland.