Having made industry predictions for quite some time on what to expect in the coming year, the last two years proved to be quite unpredictable. When we moved into 2020, nobody expected a pandemic bringing the economy to a grinding halt (although the theories of epidemics do suggest that, with a rising and increasingly mobile global population, a global pandemic was likely to happen at some point). In hindsight, 2021 seemed more predictable. The expectation was that we would get a better handle on the COVID-19 pandemic and move further towards relatively normal business conditions, although, granted, there would be a greater push for digitization and electronic channels. On the start of 2021, however, nobody did expect skyrocketing energy prices, paper shortages, global transportation problems, and increases in prices for almost any raw materials.

Among all the price increase discussions, one should keep in mind that some prices hit rock bottom in 2020, yet the increases were quite unique in recent history. Gas prices in Europe are still five times as high as the year before, even after they dropped from their peak in December (based on EU Dutch TTF spot market prices). Raw materials had hikes in 2021 as well, although the peak seems to have passed. Prices for recovered paper in Germany peaked in October 2021, but they are still double the amount paid the year before. Aluminium prices are 45% higher than a year before, although they peaked in October 2021 as well. Global record price highs were reported in nearly every forest products grade in 2021, with pulp prices already having peaked in May 2021.

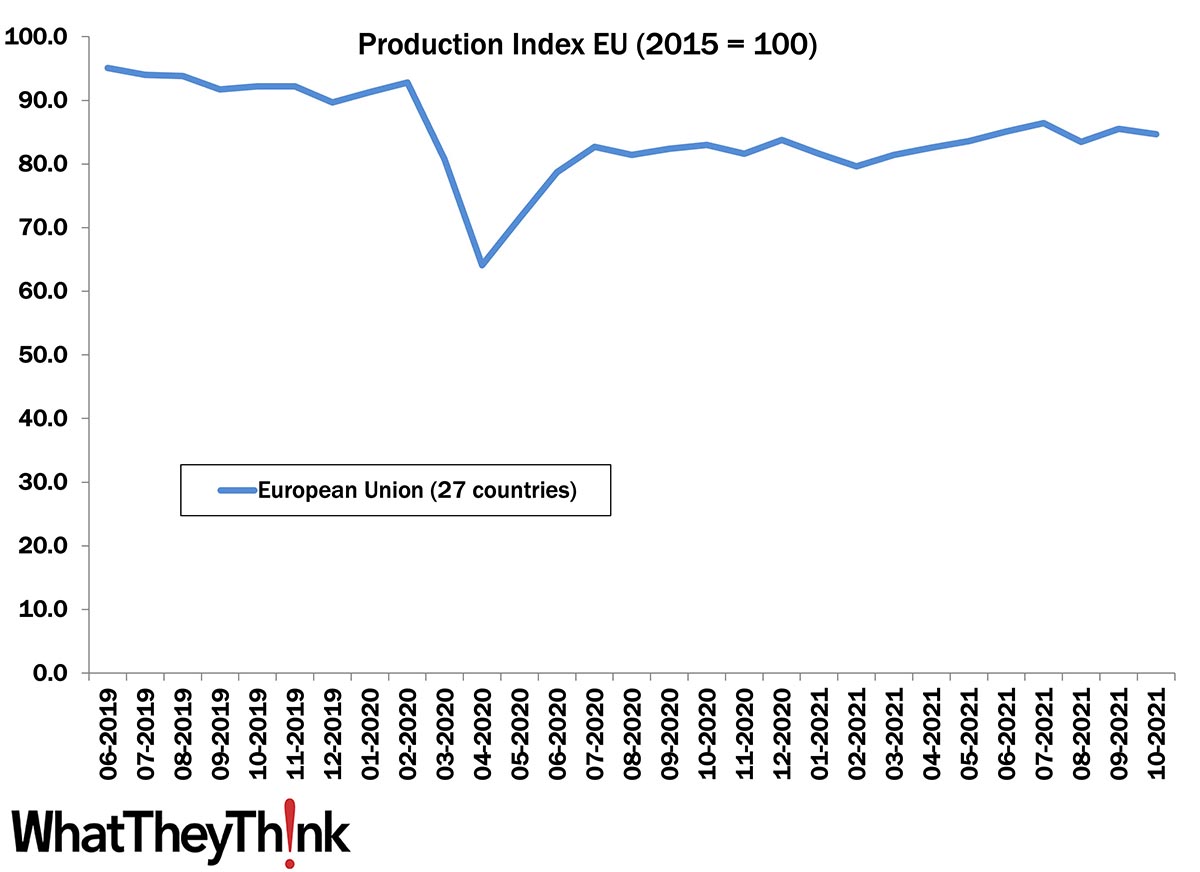

The big price increases, logistics problems, and especially paper shortages started to weigh down on print production in the EU in the second half of 2021—as can be seen in the production index. After the big shutdown plunge in 2020 (with production down by more than 30% compared to the pre-pandemic level), print production volumes recovered somewhat. With the second and third wave hitting EU countries, the recovery stalled again, however, and at the end of 2020 the production output hovered at about 10% below pre-pandemic values. 2021 was supposed to get closer to pre-pandemic levels, and after a slump in February, production levels started to rise nicely until July 2022—with values being only 7% below the pre-pandemic average by then. This recovery did not last, however. August to October saw index values falling back to values around the 85 points mark, which is quite a bit lower than pre-pandemic levels. At least some of this set-back can be attributes to paper, transport, and cost issues.

Index EU Print Production Volumes

2022 might have more unexpected events and hindrances in store for us. Here are some other factors we already should prepare ourselves for:

- Paper shortages to persist but ease up: Paper manufacturers did printers a disservice by slashing capacity without considering a rebound in demand. Although reactivating paper mills is an unlikely scenario, paper shortages will be alleviated somewhat as volumes of low-value applications (newspapers, some types of inserts, and door drops) will shrink faster in 2022 than they might have otherwise. This allows shifting some capacity to paper for higher value applications.

- Energy and material costs: Energy costs have seen their peak late in 2021 and are likely to settle at more moderate, yet higher levels than seen in 2020. Also, prices for raw materials as pulp, collected paper, or aluminium declined after their peak in autumn 2021. Likewise, they will remain at somewhat higher price levels. For processed goods, the increased prices in raw materials have not fully trickled down yet. Therefore for these processed goods (including machinery) most price rises will be felt in 2022. However, they will not reach the magnitude of the rises such as in natural gas, e.g. Rising personnel costs due to COVID-19 restrictions will not help either.

- Logistics problems are more difficult to solve. No surprise that after years of predicting autonomous driving, too few pursued a career in truck driving. Logistics companies will get a better grip on handling limited capacity, but higher prices and some restrictions will remain. Opportunities for printers exist in producing more locally or refreshing distribute and print concepts.

- Staffing: Labor shortages in the printing industry will become even more severe. Printing companies would be well-advised to follow a two-pronged strategy: automation and active and targeted recruitment. Automation will reduce the need for labor and decisions like digital vs. analog print will also be a labor decision. In a competitive labor market, companies will need to step up recruitment efforts. They should take more into consideration what Millennials and Gen Z expect from a workplace (see also my recent article: “Labor Pains: The Challenge of Attracting Young Talent to the Printing Industry”). Interestingly, automation by taking out strenuous and repetitive tasks will make the workplace more attractive as well.

- Environment: With all the challenges we’ve been facing—and the ones that lie ahead—do you expect environmental issues to take second seat? Think again. After years of pondering, sustainability is high on the agenda of many stakeholders now. For example, The Publishers Compact, a voluntary commitment that recognizes the responsibility of the publishing industry to create a sustainable future, will require printers to calculate carbon emissions and have them reduce and possibly offset those. British Mail tied their direct mail postal discounts to the environmental credentials in print production. More companies and organizations will set sustainability targets and printers are well advised to prepare in time.

General market conditions weighed down on print in the last two years, however print remains an important part of the media mix. After EU print volumes stalled in the second half of 2021, there is cautious optimism that 2022 will see a slight volume increase again. December data from the German printing industry association shows that printers are starting to see better conditions in the market. Still, pre-pandemic volume levels will not be reached again. Volumes is only half of the story, however. As volumes shift to higher value add applications revenues should have a more positive trend.

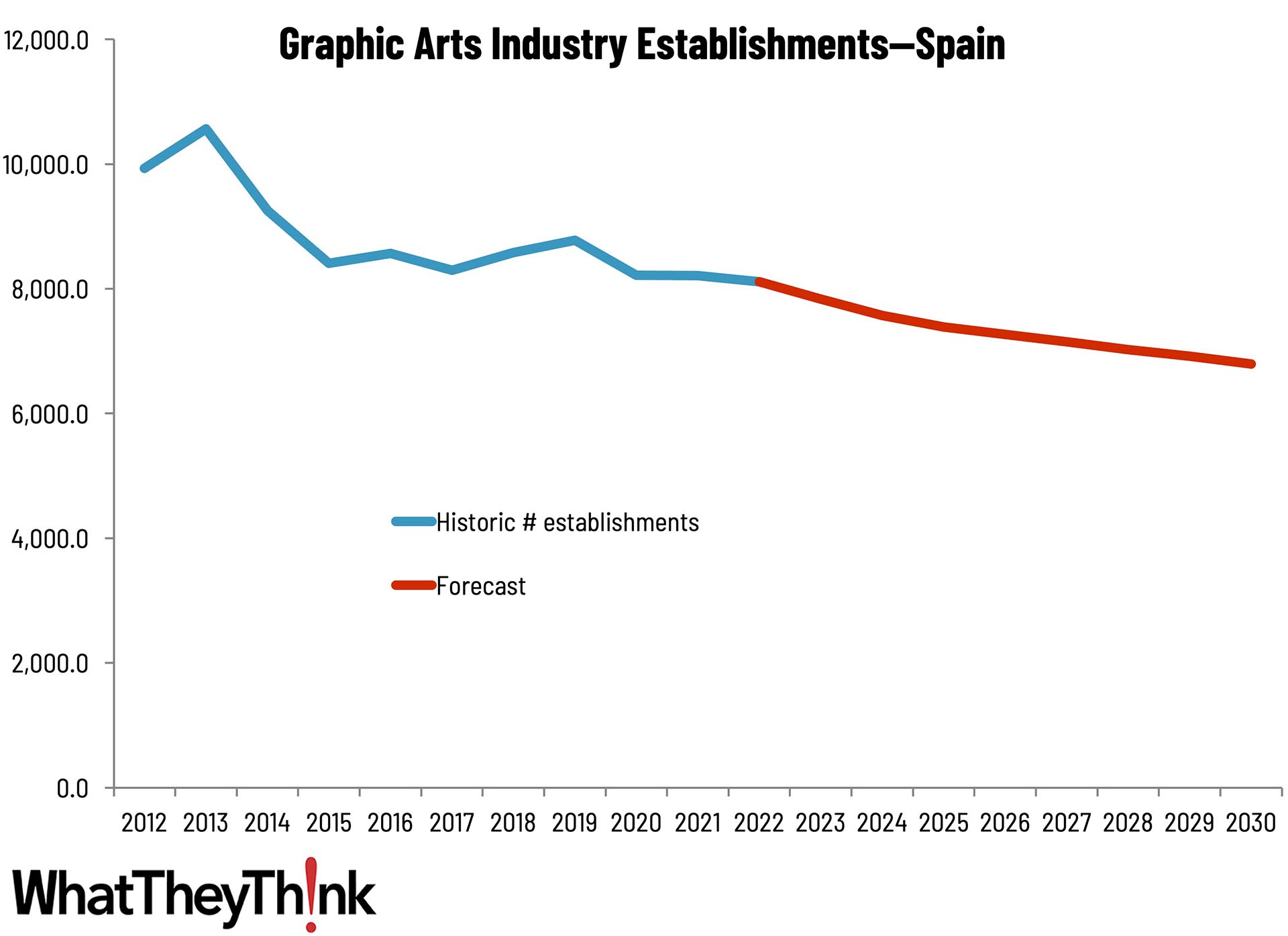

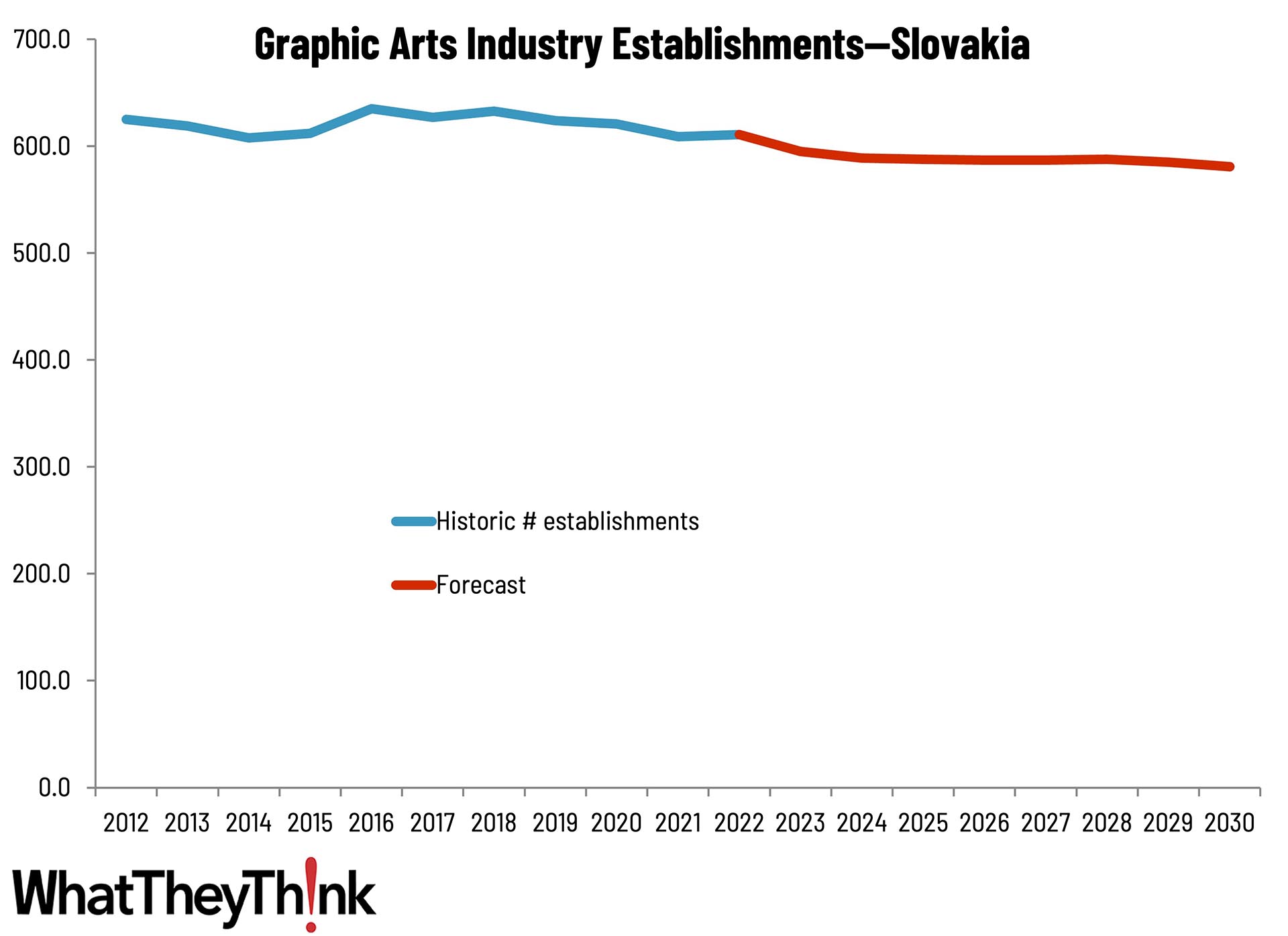

The printing industry is an industry in consolidation, but so are many industries nowadays. Yet there are plenty of opportunities for profitable production, even growth when making the right business decisions now.