The presence of digital print technology has created stellar opportunities for label, folding carton, and flexible packaging.

Throughout the industry, from brand identity and messaging to converting and distribution, digital capabilities cause processes in every part of the packaging supply chain to be re-evaluated. The very innovations that make digital viable in these markets disrupt the process and the rules which drive current packaging needs in a way that has slowed the digital integration into the packaging process.

Digitally printed labels broke through this innovation barrier way before corrugated. Only in the last few years has digital’s innovation made an impact on the corrugated print space, creating new methods for brands to communicate as well as meet their environmental and sustainability goals.

The North American packaging market is a $90 billion market, but has been slow to adopt digital into their processes. Technology innovation must be viable, make money, serve customers, and fill unmet market needs. So where does that next innovation fit in the value chain and where is that product sitting in the life cycle?

I had a chance to discuss these questions and understand the drive for digital packaging innovation and the related integration requirements with two of the most knowledgeable people in the packaging market, Kelly Lawrence, president of Lawrence Innovations, and Jeff Wettersten, president of Karstedt Partners.

Digital Speed Driving Change

Inkjet printheads were first commercialized in the early 1930s. Driven by computer speed, it’s been a continuous iteration in speed and capabilities since then, opening opportunities in industrial markets, wide-format graphics, marking and coding, textiles, ceramics, 3D inkjet direct and garment textiles.

“You see a very broad participation, and you see inkjet penetrated some of these markets beginning in the early 90s, up through 2018, and where the technology is today,” Wettersten said. “So, if you have fears or concerns relative to the technology, the technology is pretty darn stable by this point in time. It has a good track record of success in markets and applications and has proven itself quite versatile and quite complimentary to existing processes.”

Understanding the Value Chain

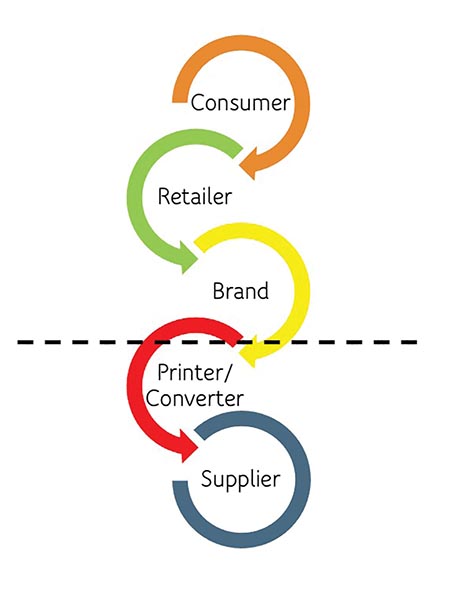

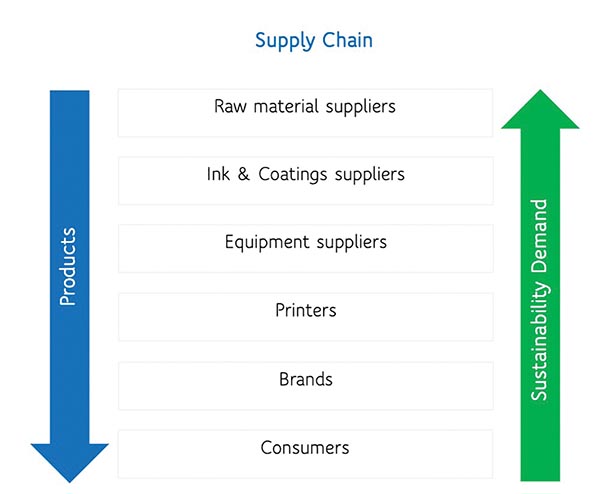

The value chain, as it relates to packaging, starts with consumers as the ultimate decision makers on what they like or dislike, and then through retailers, brands, printers, converting, and suppliers.

While the consumer ultimately is the decision maker, the control is at the brand or the retailer level with little control at the supplier level. Suppliers have little direct contact with brands and retailers. These connections in the complete supply chain are what makes things happen.

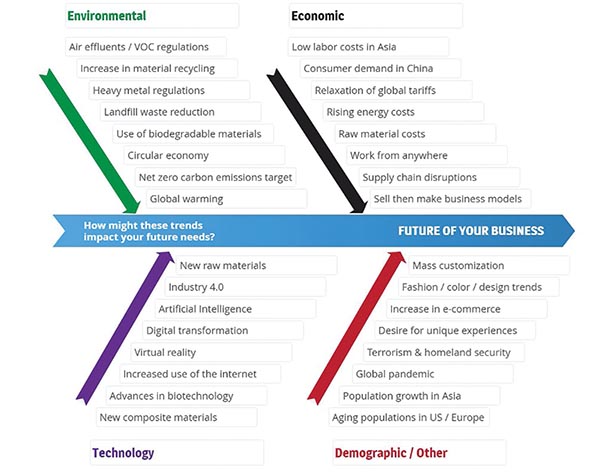

“Consumers have created a large shift in buying habits, and there is a big push for environmental sustainability,” Lawrence said. “Brands are changing their sustainability goals and engaging more in e-commerce to take advantage of the online selling model, changing how we engage consumers.

“In a big-data retail environment, we must also be aware of how data is tracked. Analytics and research are impacting internal business processes as well as the product itself. Core business models are undergoing fundamental change because of the ability to track the customer base. The big challenge we hear on the supply chain level, is that the focus among retailers and big brands has been on the last mile to the consumer.”

The packaging industry is transforming as quickly as the data can be analyzed, necessitating the ability to quickly assess options and make nearly instantaneous changes.

“The pace of change is increasing dramatically with implications at the brand level all the way to a converter,” Wettersten said. “It’s a very difficult environment for the typical converter to operate in because you can’t maintain high volume at low costs if you have continual interruptions in your workflow, and your operation must manage complexity and scope. Small converters particularly, face a dilemma on how they’re going to approach the market and where to focus.”

For packaging suppliers to enable the brands, they need to understand the consumer buying behaviors brands are trying to address as well as knowledge of the solutions that are possible. They cannot be just an endpoint to the supply chain.

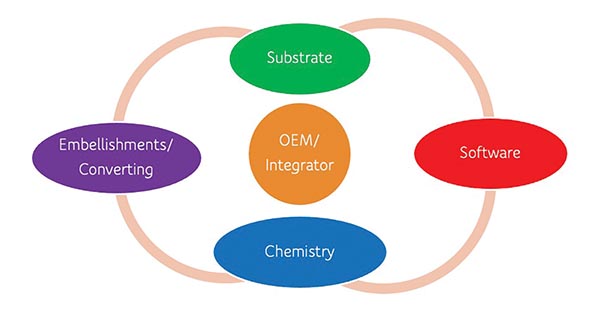

Converters need visibility from the OEMs, ink suppliers and substrate suppliers to really understand what’s possible. They need to drill down to the level of the chemistry, print head and substrate suppliers that enable solutions. By having a more open conversation and engaging different layers of the supply chain, we can make what’s possible a little bit more visible and digestible, reducing the time for technology adoption.

Concentrated Changes

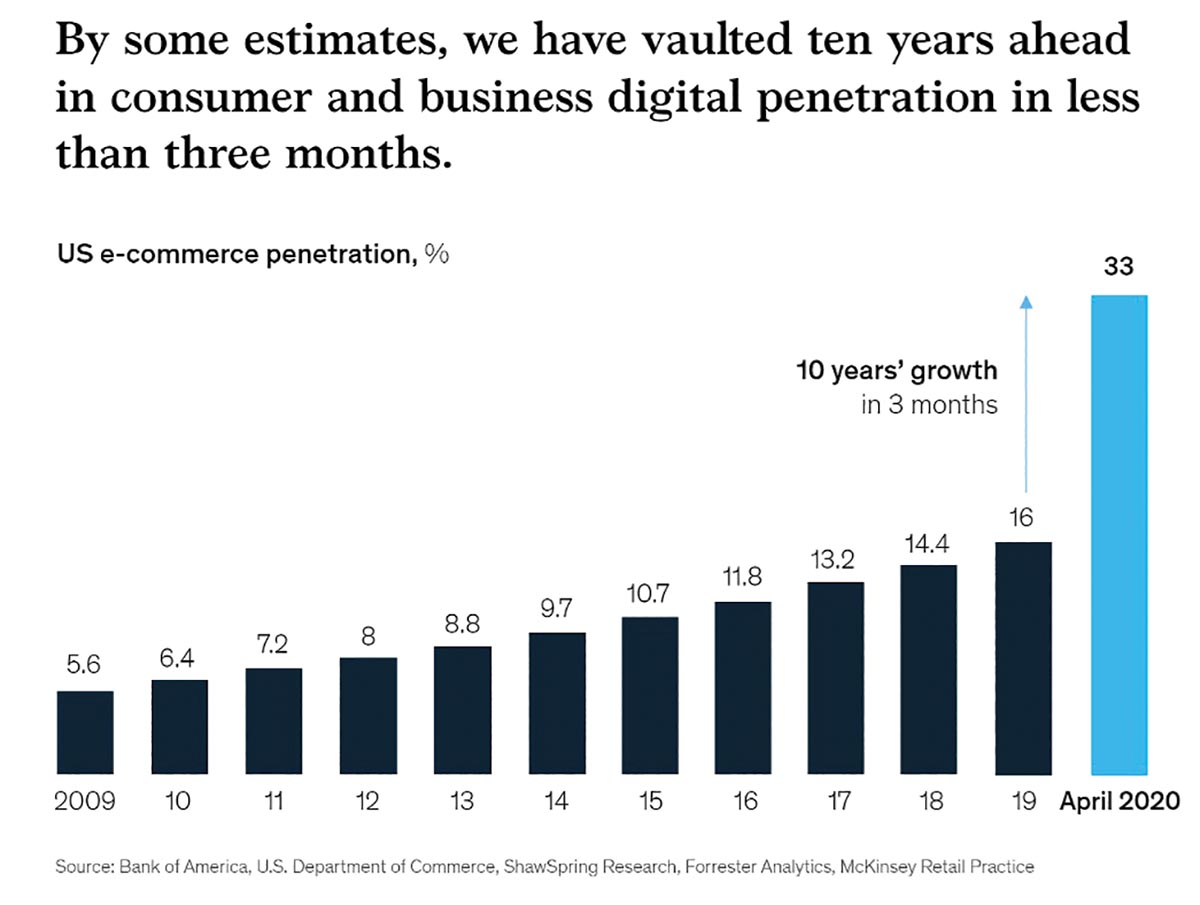

From 2019 to April 2020, we saw over 10 years’ worth of projected growth in e-commerce take place in a compressed timeframe due to a rapid shift in the consumer adoption of on-line commerce during pandemic lockdowns.

“A buying shift has expanded the need for packaging to communicate with the buyer—there is no ‘point of purchase’ advertising in the buyer’s home except the website and the packaging itself,” Lawrence said. “When we talk about digital transformation, it’s not just digital print, it’s the internet of things and the ability to operate effectively in a digital environment driven by big data.

“Consumers’ desire for customization and unique experiences is driving a flip in business models with more brands creating a direct-to-consumer channel. There’s innovation going on at the brand with sales channels and customer engagement.”

Moving the packaging market forward through customer engagement requires personalized one-to-one communications strategies that are not native to this segment. What I like to call “Sticky Packaging” resonates directly with an audience. Digital printing allows brands to create versioned or completely personalized packaging using inkjet driven by data in their process. This personalization extends to advertising and cross-promotion.

Amazon has even started offering a cross-sell option, by printing advertising on packages, which has nothing to do with the product inside. One recent example was an advertorial for Shark Week on The Discovery Channel. Amazon implementing cross promotion on packaging to TV viewers creates an ideal way for other types of media to reach consumers from an advertising standpoint.

“We are seeing more and more promotional elements starting to go into true customization in a high-volume world of packaging,” Wettersten said.

What’s the Fit for Digital?

The value of digital printing technology extends well beyond the ability to print in a typical converting environment.

“It has everything to do with the operational enhancement that digital printing can provide,” Wettersten said. “We work with many companies, and some of them have started bringing outsourced work back in-house and enjoying the cost reduction opportunity. We have seen this same effect in the label industry and are starting to see it more in the corrugated industry and folding carton as well. It impacts business from an operational standpoint, and frequently, it can be around converting, material purchases, or the operation of the corrugator to upstream processes from print, and aggregating orders for productivity improvement. There is a need for continued development around materials, software, and chemistry. They recognize that there are opportunities, but need assistance to position themselves better with the addition of digital.”

Upstream brands and retailers define packaging requirement based on the functional needs of the product. Merchandised brands respond to that, and then converters must build to the predefined specifications. Being last in the chain is not easy for the converters and often is not ideal for optimizing packaging potential. If you’re way back in the supply chain, you’ve really got to work to understand and influence the decisions which impact the packaging converting process. Inkjet effects every part of the supply chain from the brand to end-product. Understanding this, and educating customers, are the biggest hurdles to success in integrating inkjet into this process.

Changing Minds with Digital

It has taken much longer for inkjet to penetrate packaging than other markets.

“There are so many pieces and parts when it comes to package printing that are beyond what production inkjet typically addresses,” Wettersten said. “If we wish to advance inkjet adoption, we have to add more education around the process, which must include the converters.“

OEMs are having conversations with brands, which is great from an inkjet standpoint, but we need to educate the brands on what’s possible beyond just the print stage, as well as the complexity of package design and development.

For example, Colgate Palmolive is a $15 billion-plus company. Changing their branding communication on packaging is not a conversation with one individual within the organization. It requires a process that will change many minds as it disrupts many parts of internal and external processes.

So how do we help brands move digital packaging forward? The industry needs to do a better job of publicizing the marketing wins and the supporting data. Brands as well as the packaging converters need evidence of success.

“We are not hearing enough about that,” Wettersten said. “Where is it working? Why is it working? How is it working? If we can bring to the industry evidence of success, the faster we’ll be able to penetrate.”

Beyond pure marketing success, brands are also influenced by sustainability factors, because it has been proven their customers care about “green” issues. Major brands are focusing on environmental and sustainability goals by committing to meet new 2025 plastic economy commitments. Industries, governments and even United Nations are pushing for regulatory packaging changes forcing the substrate manufactures to design new films and packaging to help brands meet these goals.

By stating that they want 100% recyclable plastics, big players like Colgate Palmolive can shift the industry.

“They have already improved their sustainability profile in 99% of the new products they’re bringing to market,” Lawrence said. “This direction is requiring other industries included in the supply chain to also change or innovate.”

The sustainability direction is creating more opportunity for inkjet. Inkjet manufacturers such as Barbaran and Jetmaster are creating partnerships for corrugated machines, and ink manufacturers like INX are developing jettable bio-based ink for better recyclability.

The value here is that it enables better recyclability of the end printed corrugated.

“Brand sustainability is influencing the substrate and the inkjet innovation and all coming together to help corrugated packaging recyclability,” Lawrence said.

Across all packaging segments, education on the many marketing, efficiency and sustainability benefits of inkjet—along with the realities of implementing new processes are needed to advance the market forward.