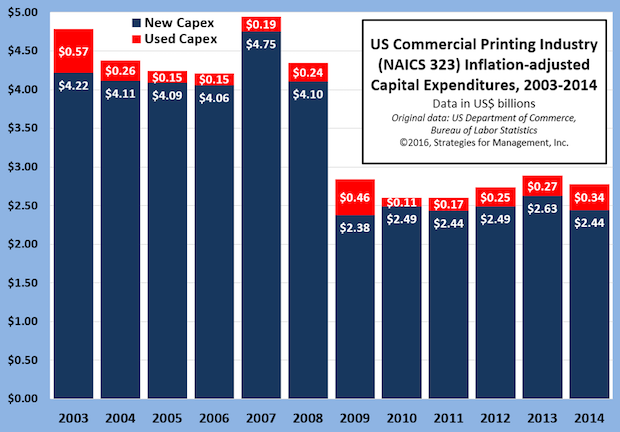

Investments in new equipment and other capital goods fell -7% from $2.63 billion to $2.44 billion after adjustment for inflation. Investment in used equipment and capital goods represented 12% of total capex. The $340 million in purchases was up +26% compared to 2013, and was at the highest level since 2009.

At that time, the used capital equipment and goods were $460 million. The recession flooded the market with used equipment. Much of that equipment was “young” and represented good bargains for many healthy printing businesses. In 2014, it is believed that the amount was bolstered by industry consolidation and especially tuck-ins. That kind of consolidation deal orphans much equipment to auctions and bankruptcy auctions. The second half of 2014 was also the time that industry shipments started their rise with favorable comparisons to the prior year, now going on for 21 months.

Capital investment as a percentage of 2014 industry shipments was only 3.3%. In the 1990s, it was usually about 4.5%. At that time, prepress equipment was an important part of industry purchases. That category is essentially gone, with no other category to replace it. Press sales, except for specialty applications are low. Any of the bright spots for investment, such as wide format printings and digital color production, as usually lower in price than new presses were. With fewer print businesses to make capital investments, it is no surprise that total capital investment was stagnant from 2009 to 2014.

What can change it? Even an interesting drupa cannot make capex increase in 2016 as many of those new product offerings are not available to be shipped this year, and possibly next. If some of the new presses, especially the new ink jet offerings, meet and exceed expectations, the could spark new interest in new production equipment that has been missing from the market in recent years.

There is also another factor, and that of industry consolidation. The pool of capital available for all kinds of investment is a fixed amount at a particular time. Mergers and acquisitions consume part of that pool, directing that capital elsewhere. Most of the time that is a good use of capital because it leads to more efficient use of industry productive capabilities. That capital is put in the hands of more competent enterprises for today’s market. In the long run, that creates a better opportunity for the sellers of the best new technologies. Unfortunately, that is a promise, as the date of such new purchases seems to stay firmly on the horizon for now. What will shake those purchases loose remains to be determined. The industry needs new innovations that change the value of their offerings in competition with digital media, creates new products that capture the attention of new buyers, increase the productivity of workers. Perhaps drupa will reveal what some of those might be.