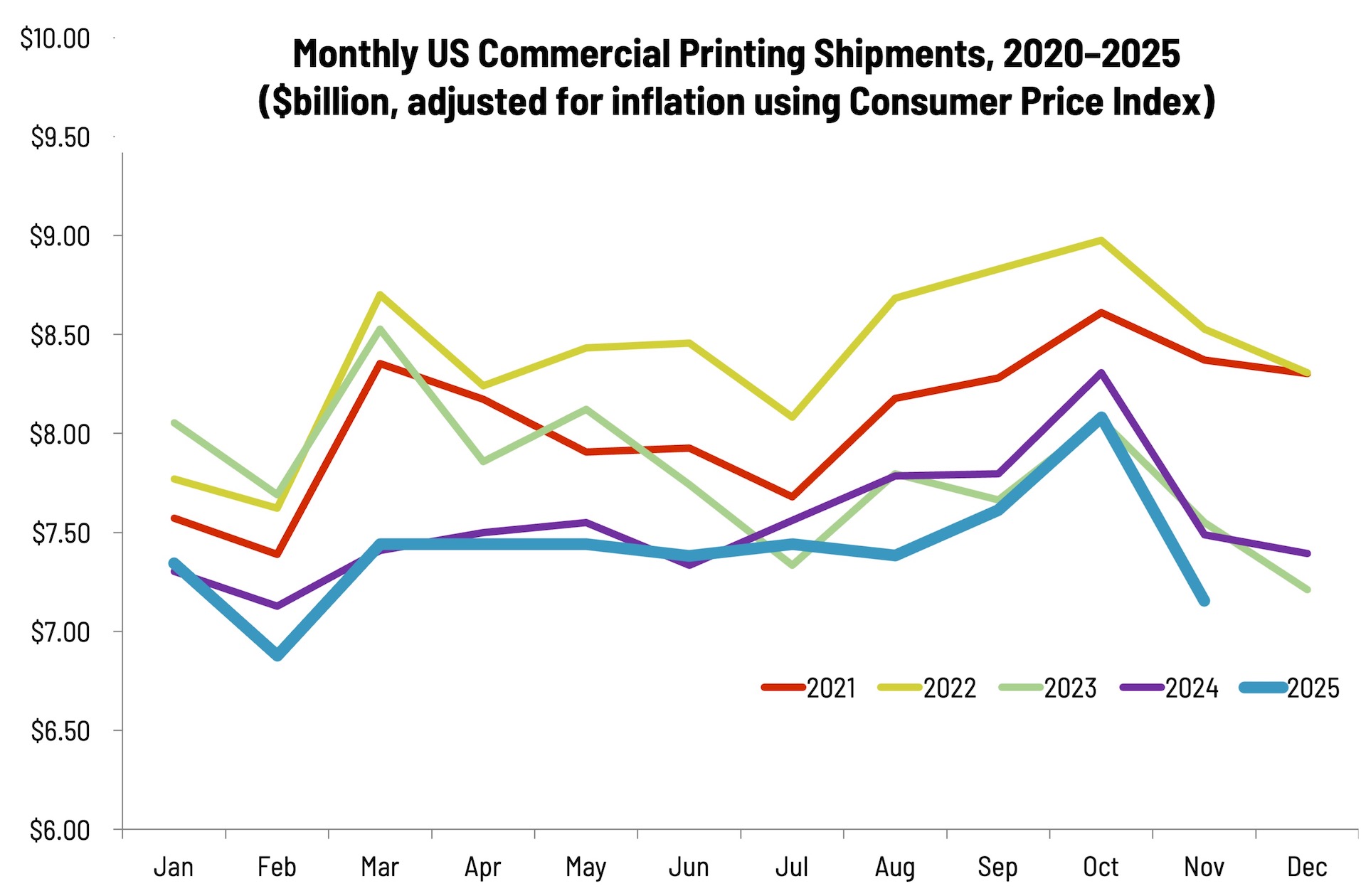

Yowza! What goes up, must come down, we guess. After ramping up to a pretty impressive high in October, printing shipments crashed and burned in November, coming in at $7.15 billion, down from October’s $8.08 billion. A healthy (or unhealthy) chunk of this is the seasonal slowdown as we headed into the holidays. Most of 2025 certainly had its challenges macroeconomically: the tariffopalooza did not help matters (although that had kind of stabilized in the late fall, although the next few months will see the uncertainty increase again), and the employment situation had been (and continues to be) a little concerning, but seems OK. Most of 2025 was not too far off 2024, at least up to the fall, and even November’s precipitous drop parallels November 2024’s drop. Still, it did beat out February 2025 as the single worst month for printing shipments in at least the past five years, but probably ever.

But as we all know, shipments are only half of the story; profitability is the other half, and as costs for just about everything continue to rise (if you have checked your utility bill recently you may have been in for a shock), printers can only pass so much of that onto customers, which means that despite how much shipments (aka revenues) rise, profitability may remain flat, or even decline—and when revenues decline, that makes it even more of a problem.

Year-to-date (January to November) shipments for 2025 are at $81.60 billion, far below last year’s $83.16 billion. So unless we have a truly spectacular December, total shipments for 2025 will be less than those for 2024 or any other year—and, yes, even the COVID year.

We just closed our 2025 Printing Outlook survey so once we go through the results, we’ll have a better idea of what’s been going on—and what we can expect to go on for the remainder of 2026.