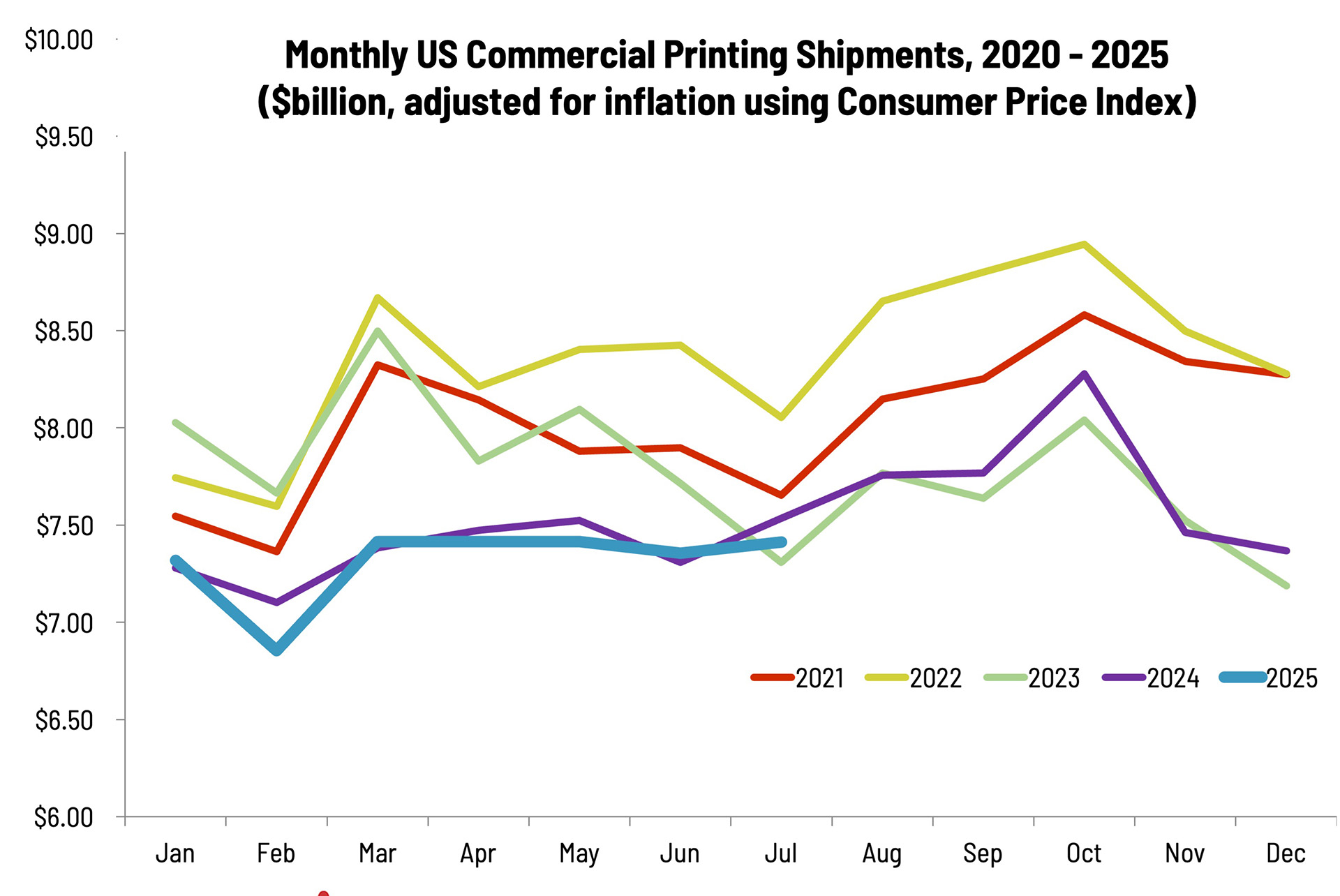

The first two months of the year gave the impression that it was going to be one of “those” years—a rollercoaster ride of dramatic increases and terrifying plunges. However, and make of this what you will, since March, printing shipments have been essentially flat, and certainly flatter than we’ve ever seen them. (Previous WTT economic analysts would likely have used the term “flatlining,” but we’re more of a glass-half-full sort, so we’ll say “steady.”) And while April and May saw the lowest level printing shipments have ever been, June shipments were slightly above June 2024, at $7.36 billion, they were down slightly from May’s $7.42 billion. Shipments usually drop in July, but in this case we saw a slight rise, and shipments were above July 2023’s $7.31 billion. (2024 had been another rare year where July shipments rose—is this a new seasonality in the works?)

Year-to-date (January to July) shipments for 2025 are at $51.19 billion, a bit below last year’s $51.61 billion.

This year has been a challenging one, economically, what with the tariffopalooza and what could be a softening job market. This data set comes before the government shutdown, which, if it lasts for an extended period, will likely adversely affect the overall economy. (The shutdown also means we will have minimal, if any, access to government economic data.) Still, shipments have at least remained steady. We’ll take flat over declining any day. August usually sees a big rebound—is one in the cards this year?