Source: US Census Bureau: Quarterly Services Survey

We haven’t looked at publishing and advertising revenues in a while, but the Q2 2025 Quarterly Services Report was recently released, so we thought we’d have a look at how the creative markets have been faring.

And, well, generally speaking, not so hot.

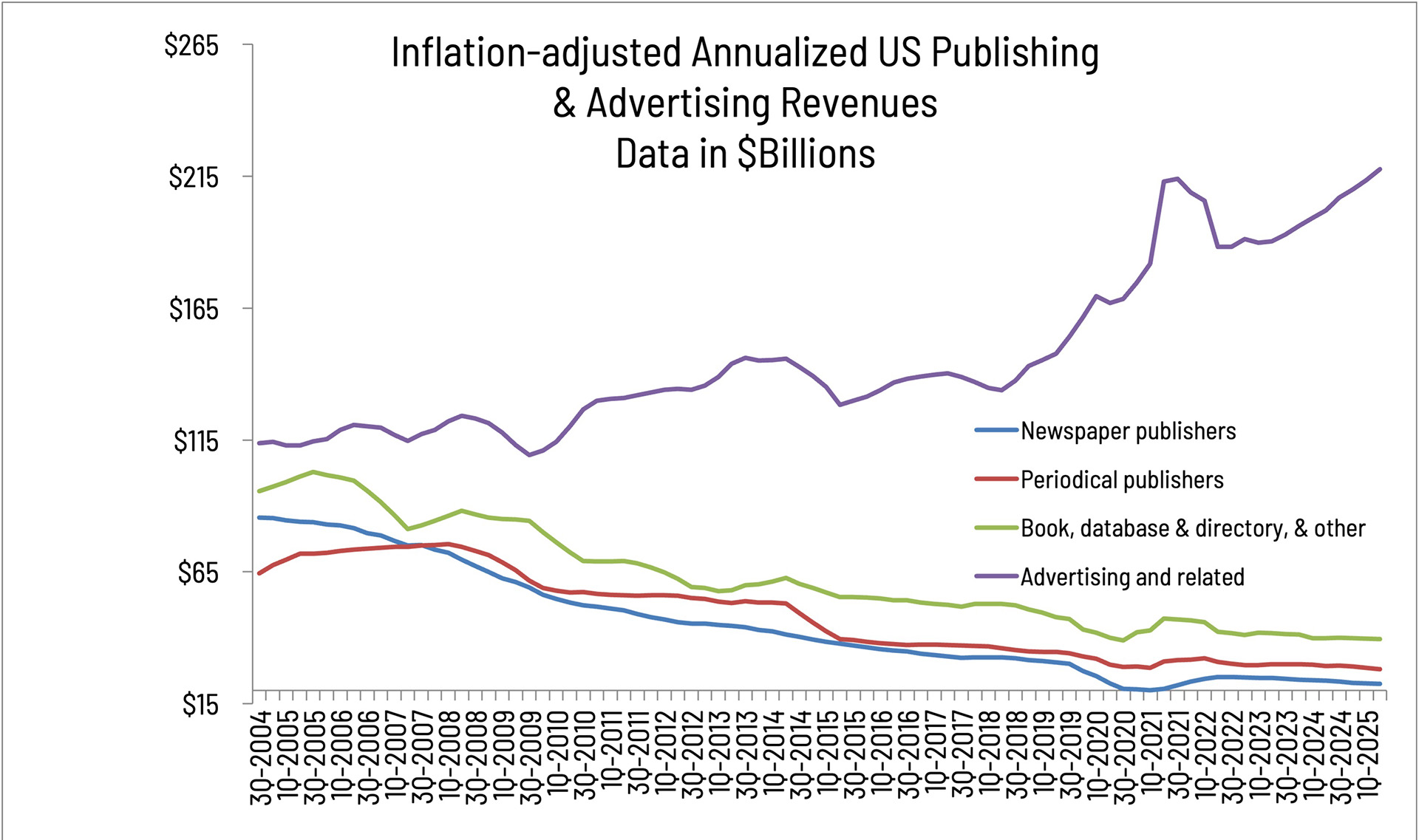

Publishing had a rough time during the pandemic, although all three publishing segments—especially books—saw a rebound afterwards, with a leveling off as revenues returned to trend.

On an annualized basis, since 2004, newspaper publishing revenues have been plummeting—even by 2020 revenues had dropped by more than $50 billion. 2024 saw them continue on a slight downward trend which continued through the first half of 2025.

Periodical publishers aren’t in much better shape; since 2004, revenues have been in a kind “punctuated equilibrium,” with periods of relative flatness followed by steep declines, the first likely caused by the Great Recession, with the second in 2014–2015 likely the result of advertisers adjusting their media spending from publications to social media, streaming services, and other online initiatives. They saw a less dramatic drop than the other segments during the pandemic (by then, the damage had been done) and since the pandemic, revenues have been pretty flat if not down slightly.

Book publishing revenues also declined steadily over the past 20 years, but have also been pretty flat since the pandemic. Over the course of 2024 and 2025, book publishing revenues were essentially unchanged.

Advertising is a whole other matter. Advertising revenues had been relatively flat over the course of the 2000s, and as expected there was a plunge during the onset of the Great Recession. But advertising recovered pretty quickly and during the 2010s there was a continued shift to non-print advertising, as well as to other kinds of marketing initiatives than what we think of as “advertising”—content marketing, social media, and other forms of digital marketing. Cable and TV still exist as viable advertising media, and their replacement, streaming services, have also upped their reliance on advertising, with more ad-based tiers and even stealthily converting ad-free tiers to ad-based.

Those ad-based service tiers have not been a success, and people remain happy to pay a premium to not watch ads. However, as streamers continue to raise subscription fees (often without warning), we suspect people will start reevaluating the services they subscribe to. There is no shortage of advertising on other platforms such as Spotify, YouTube, and other services that have both ad-supported (free) and premium (ad-free) options. There are becoming precious few places where there is no advertising (our Around the Web last week mentioned new Samsung refrigerators that will have built-in ad-displaying screens) and very little of it is actually compelling.

During the Government shutdown, there will be no data releases from the BLS, Census Bureau, etc., so industry data reporting may be spotty until further notice.