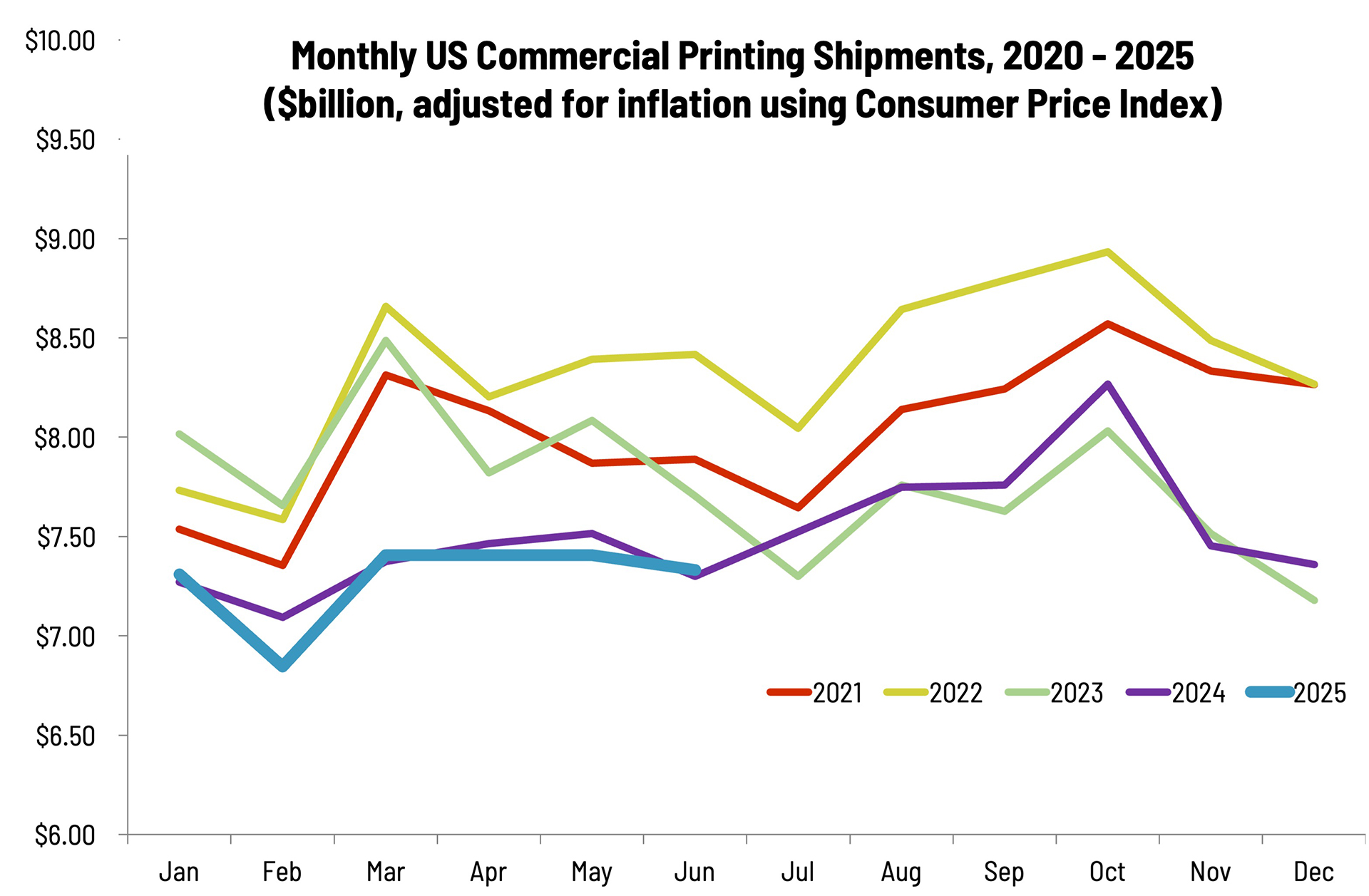

As recently as two months ago, we had remarked on what a roller coaster year it’s been. But since March, printing shipments have been virtually flat, or flatter than we’ve ever seen them. Sure, April and May have seen the lowest level printing shipments have ever been, and while June shipments were slightly above June 2024 shipments, at $7.33 billion, they were down slightly from May’s $7.41 billion. The last two years have seen shipments decline in June, but at least this year saw the smallest decline.

This is interesting because, as we found out yesterday, Q2 GDP actually increased 3.3%, which made up for Q1’s decline. Meanwhile, retail sales were up in June (concurrent with our shipments data) and retail sales in July were up again. Tariffopolooza has been in full force—could that be making print buyers more discretionary?

Trying to make sense out of traditional seasonality is a challenge; July usually sees one of the lowest ebbs of the year—except for last year. Which way will the roller coaster go? Do you feel lucky? Place your bets!