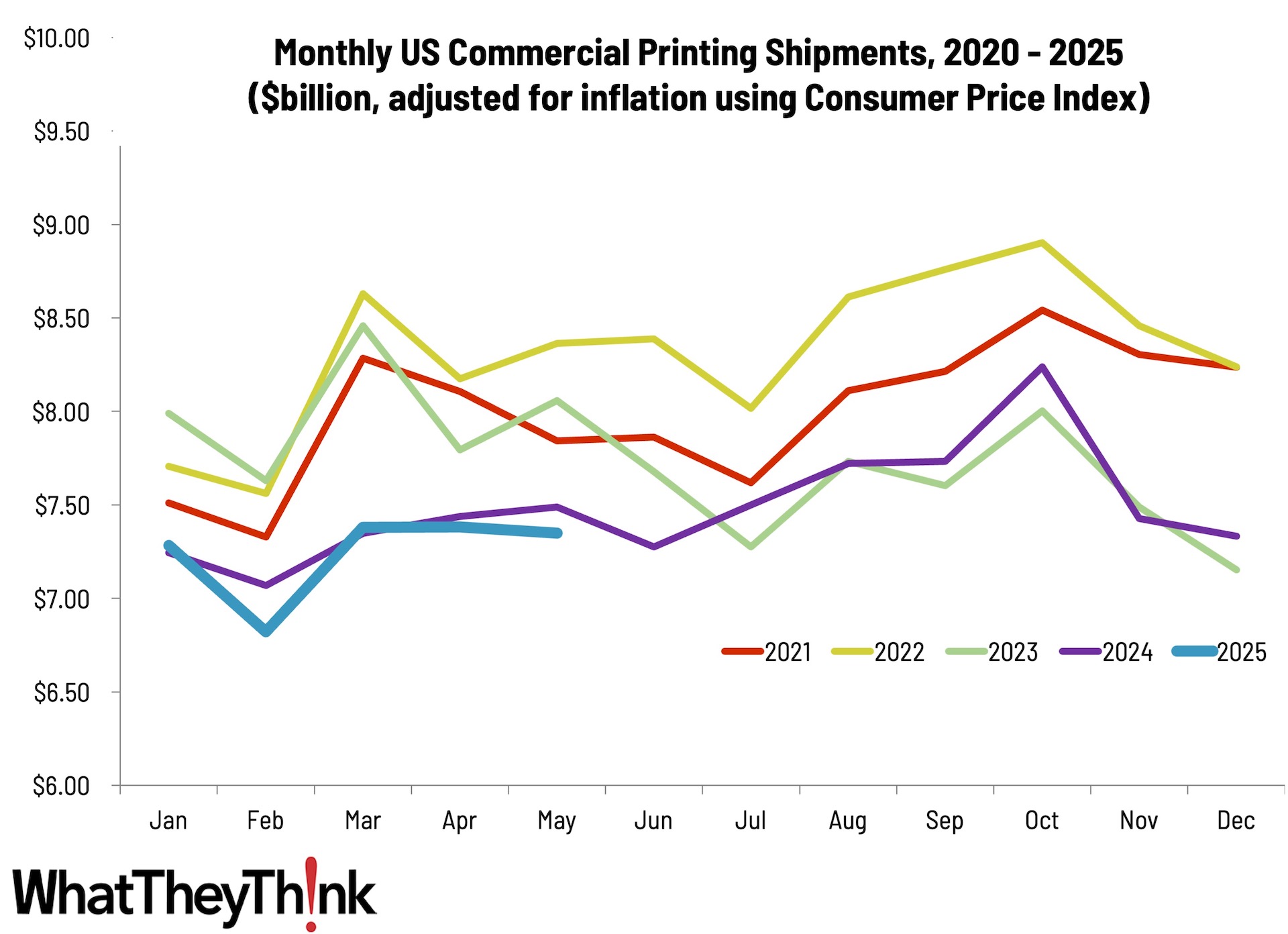

The last time we looked at shipments, we had remarked on what a roller coaster year it’s been. If we want to keep that analogy (for whatever reason), we can probably say that we are in one of those flattish stretches before the peaks and troughs start up again. Anyway, May shipments came in at $7.35 billion, down ever so slightly from April’s $7.38 billion—a little atypical for May, as three of the last four years have seen May shipments increase. This is interesting because, as we found out on Wednesday, Q2 GDP increased 3.0%—making up for Q1’s decline in GDP. Retail sales had been down in May (concurrent with our shipments data) but rebounded in June, which may bode well for June shipments? Tariffopolooza has been in full force—could that be making print buyers more discretionary?

June usually sees a decline in shipments, but maybe we can continue to go against trend. Regardless, “uncertainty” continues to be the word of the year.