Data Analysis

Retail Sales—January 2020

Published: February 28, 2020

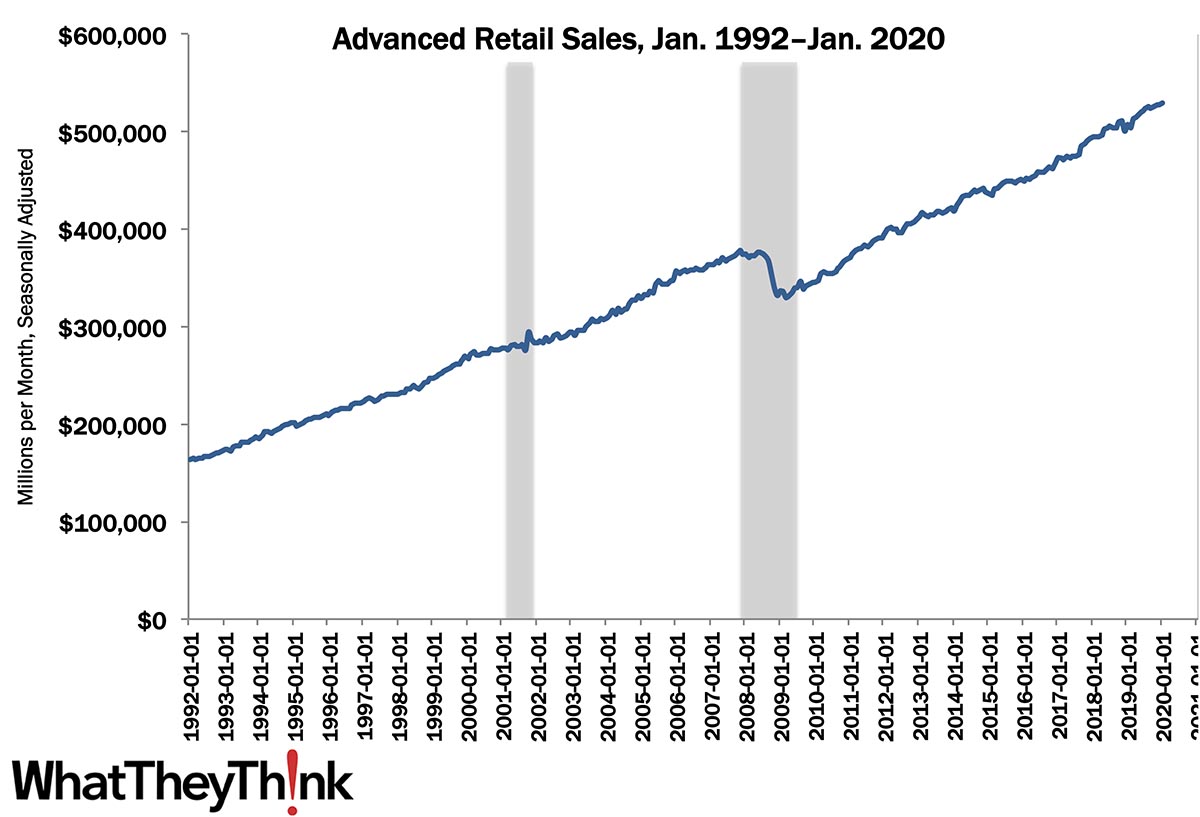

Advance estimates of U.S. retail and food services sales for January 2020, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $529.8 billion, an increase of +0.3% (±0.4%) from the previous month, and +4.4% (±0.7%) above January 2019. Retail drives a lot of printing and packaging volume, so it’s important to keep an eye on that sector. Full Analysis

Book Printers—2017

Published: February 21, 2020

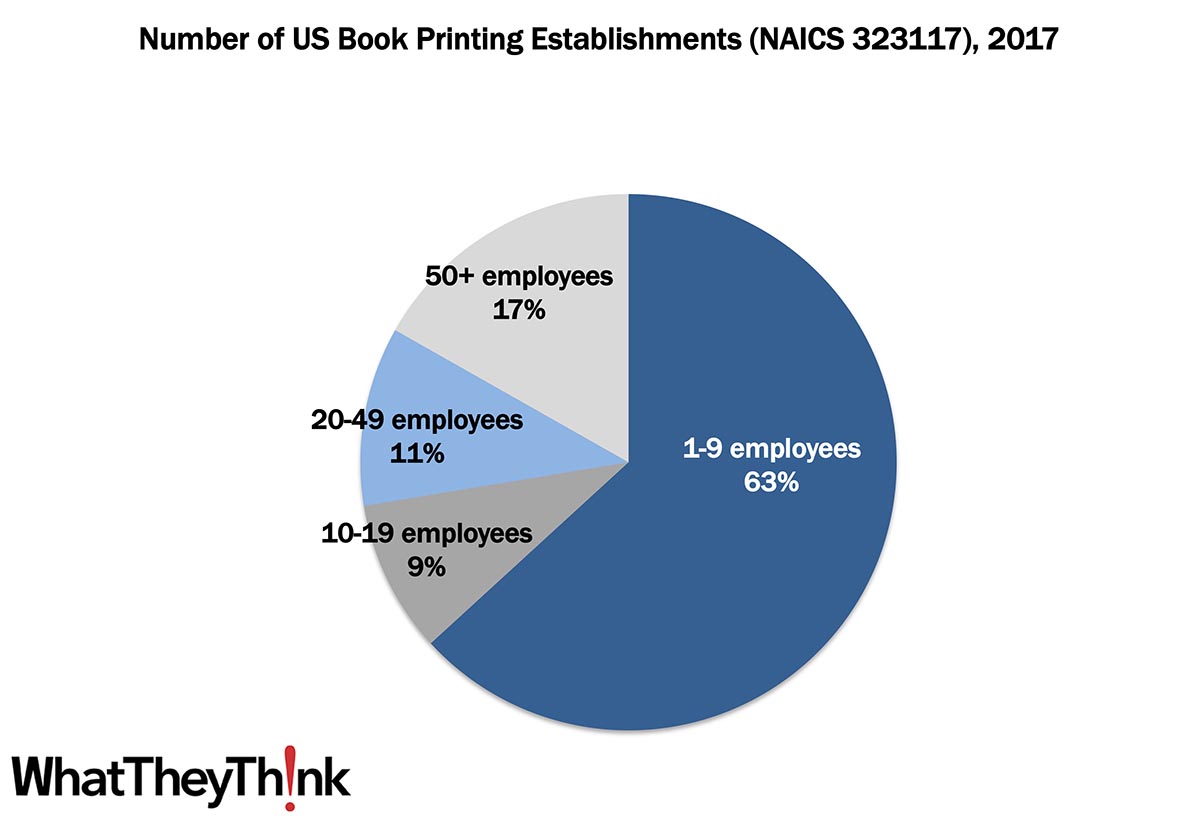

The latest edition of County Business Patterns is out, which updates number of establishments and other data to 2017. In that year, there were 500 establishments in NAICS 323117 (Book Printing). The majority of these establishments (63%) had fewer than 10 employees. Full Analysis

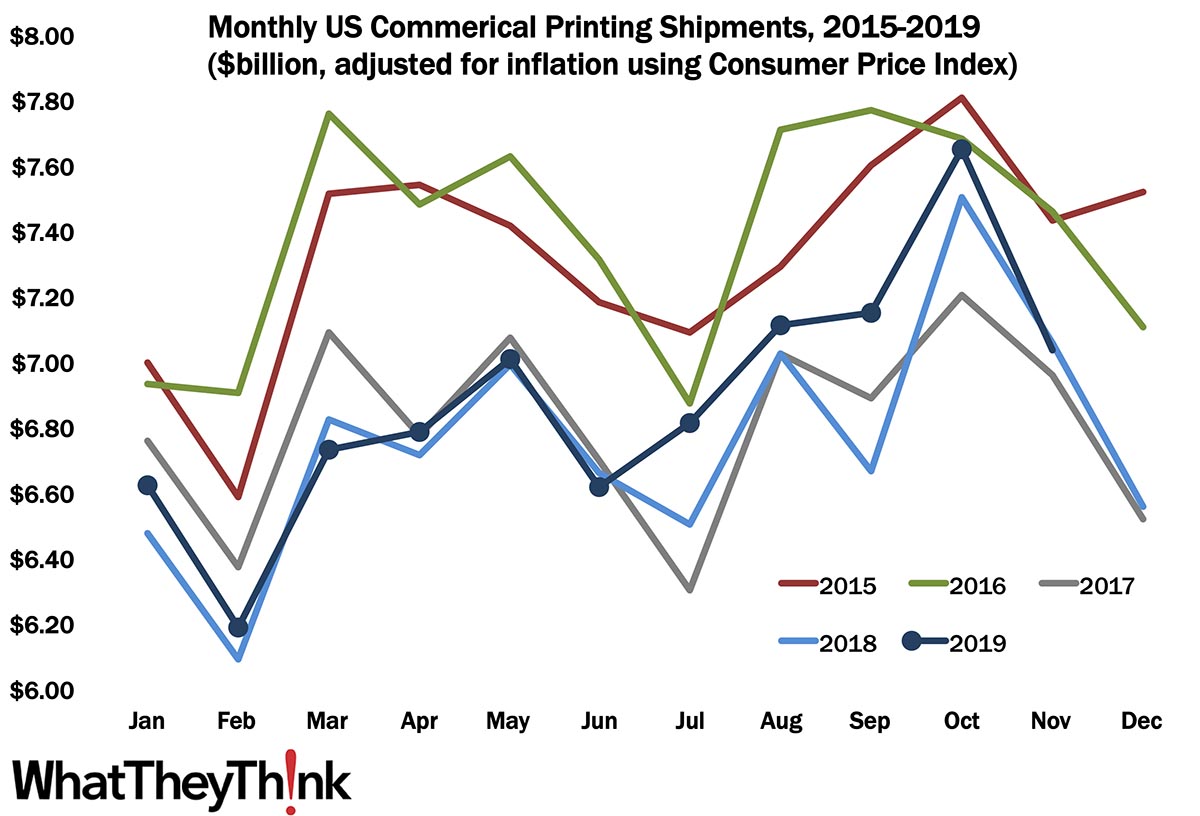

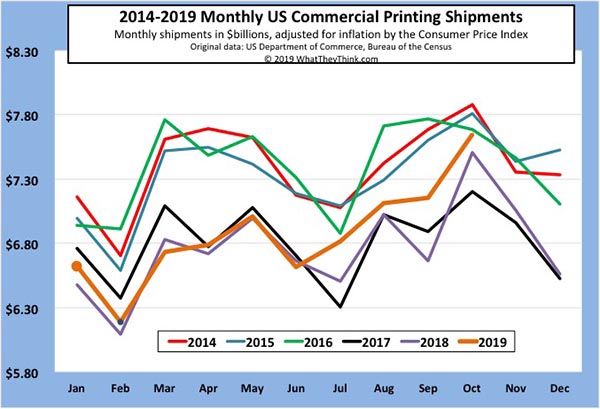

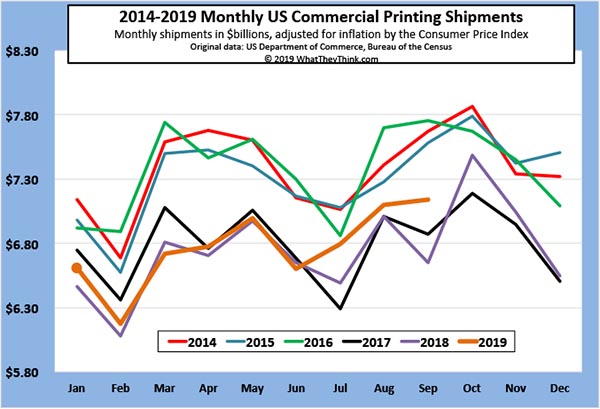

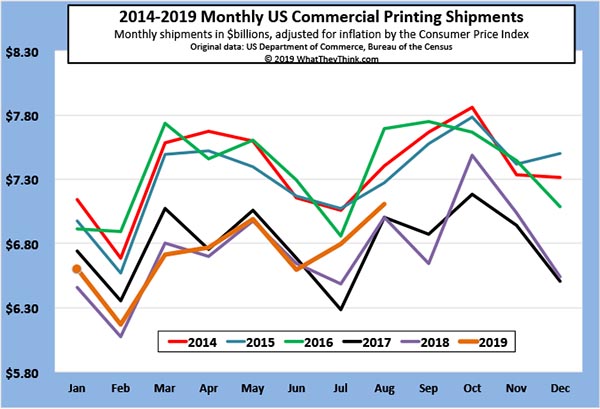

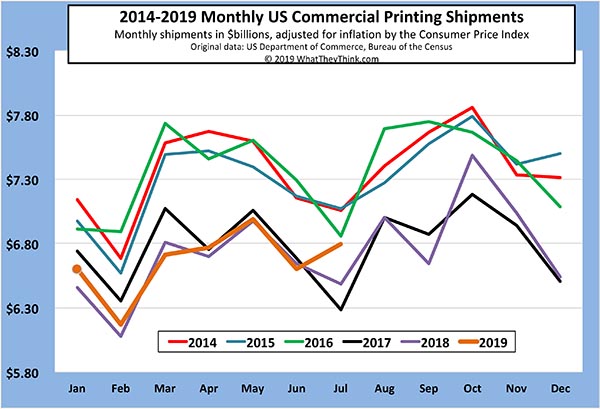

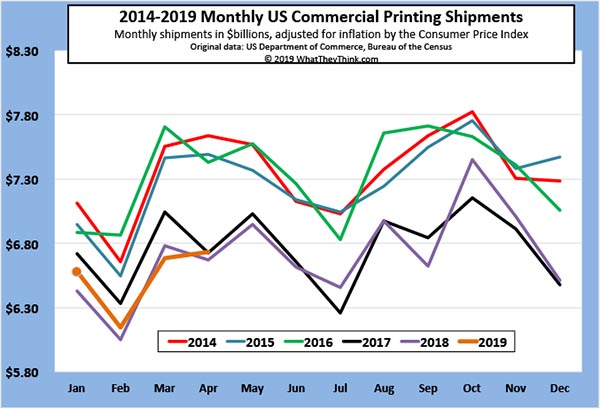

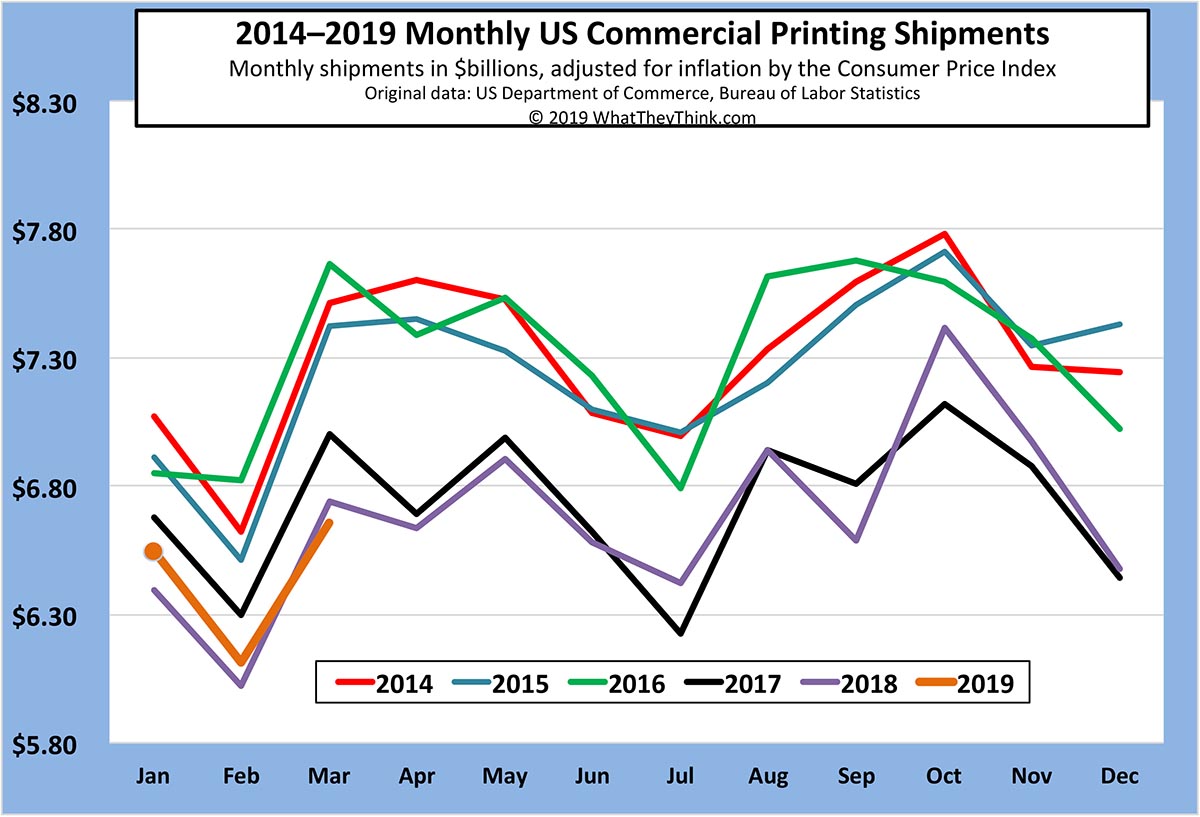

December Shipments: Ending 2019 on a High Note

Published: February 14, 2020

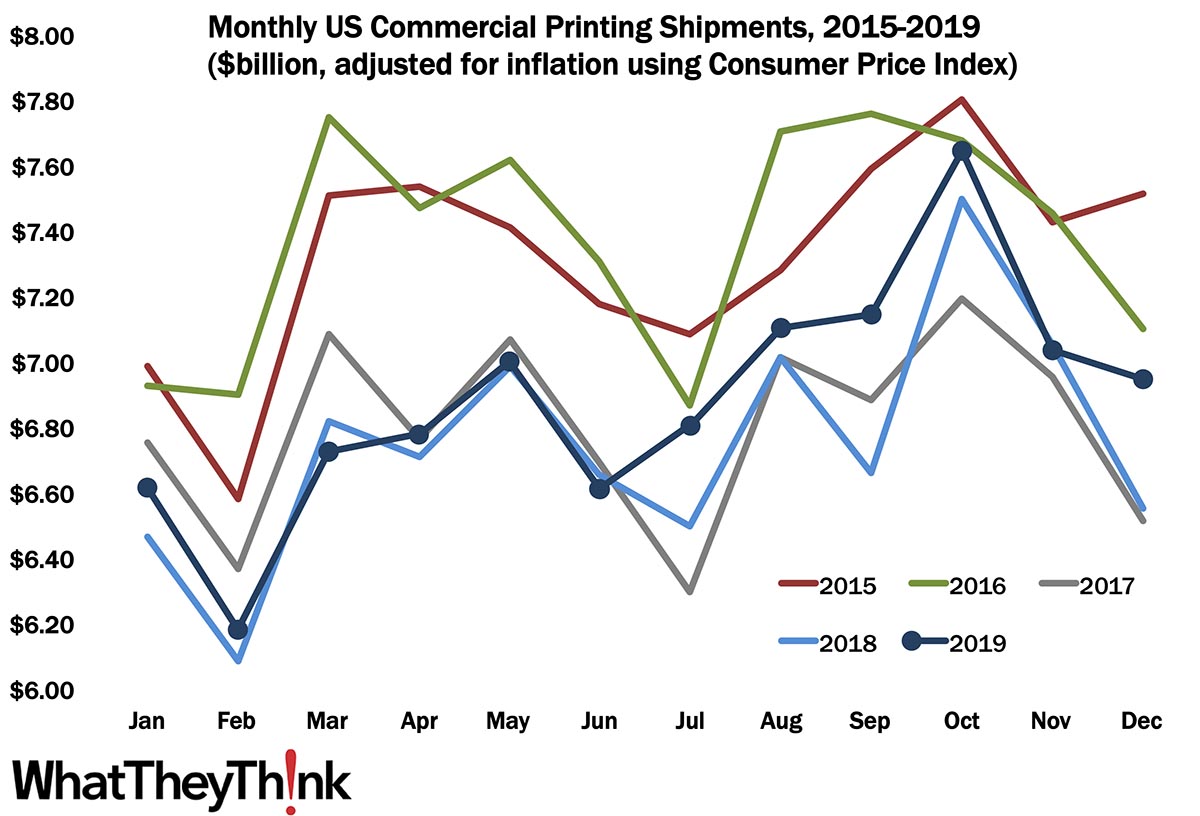

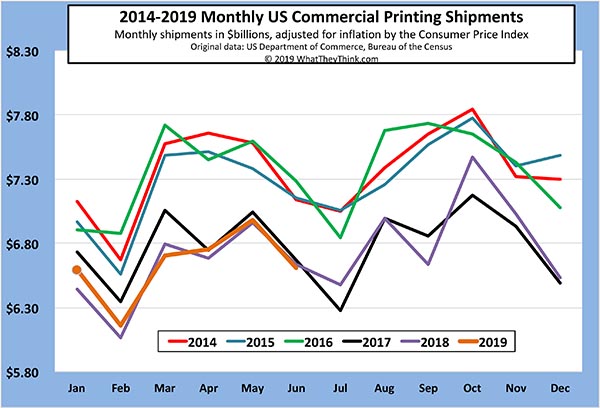

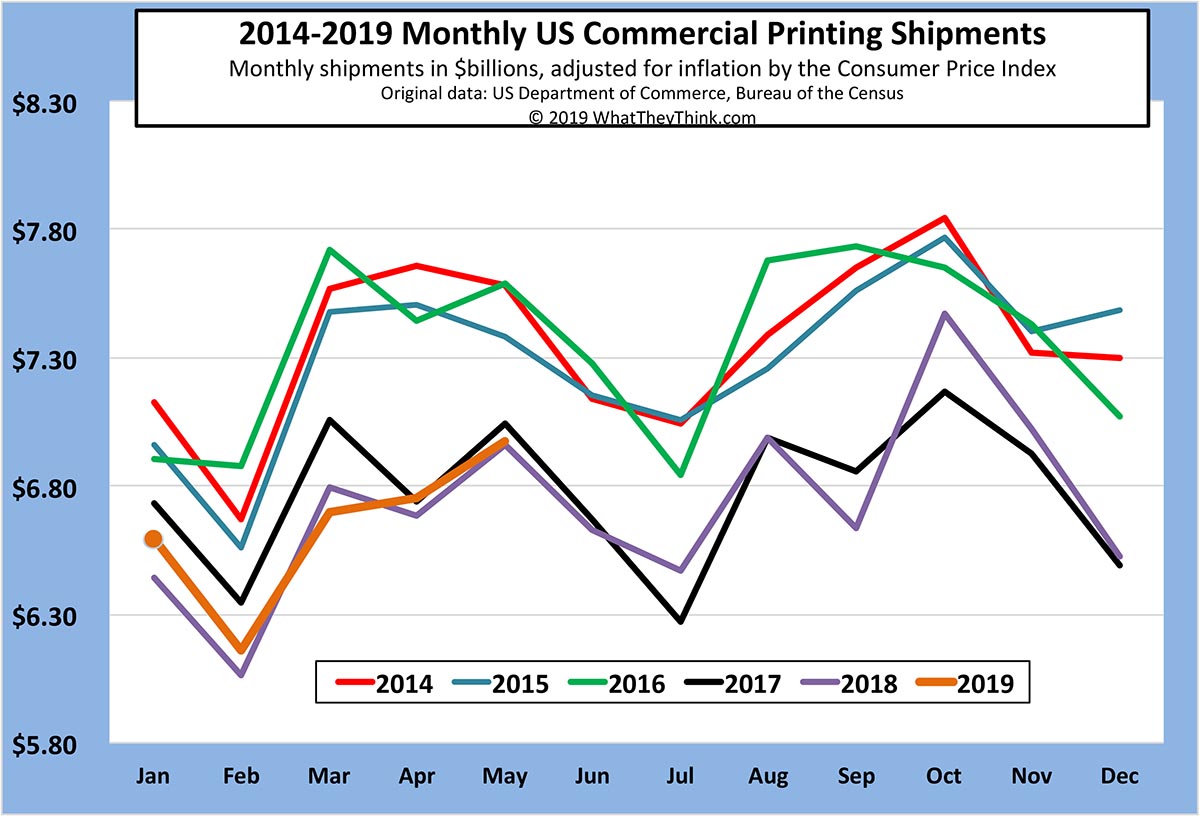

The value of printing shipments for December 2019 was down from November—as we expected it would be—but not down as much as been the case in recent years. At $6.95 billion, December shipments were down from November’s $7.03 billion, but far above the depths of 2017 and 2018. Full Analysis

Screen Printing Establishments—2017

Published: February 7, 2020

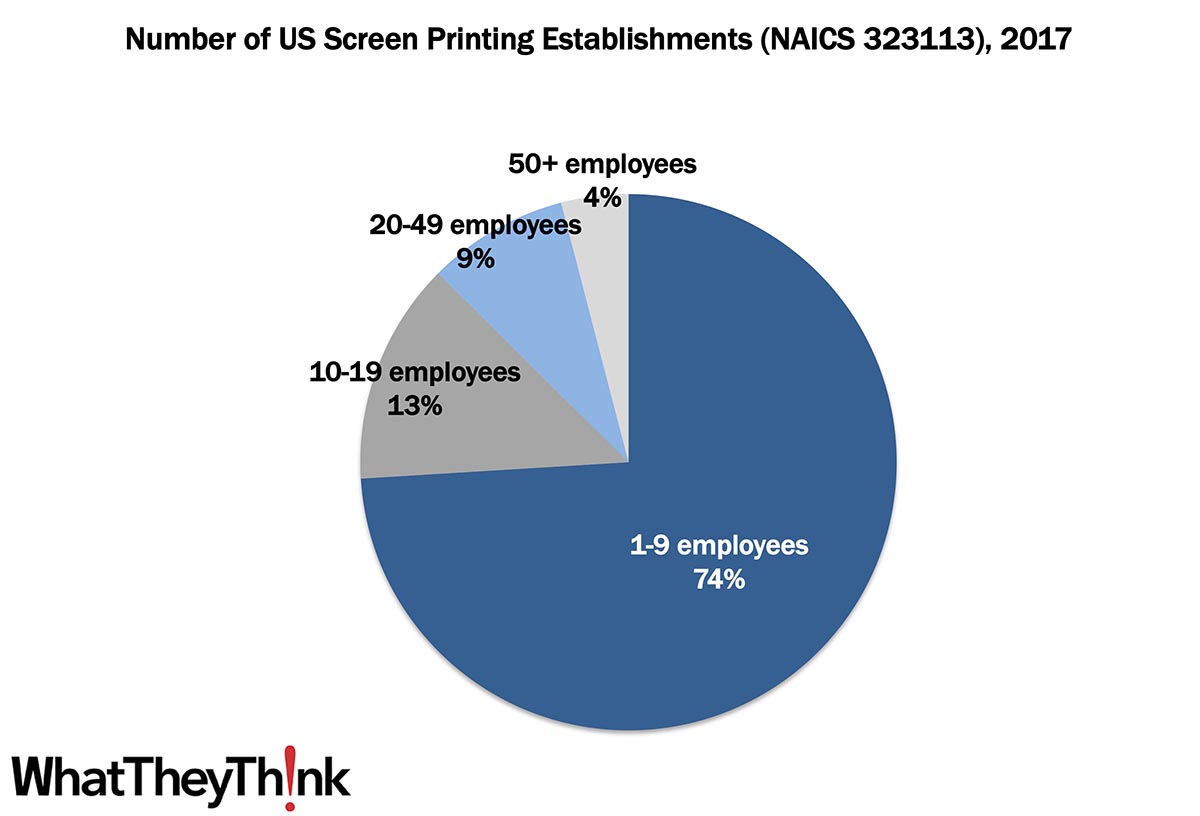

The latest edition of County Business Patterns is out, which updates number of establishments and other data to 2017. In that year, there were 5,186 establishments in NAICS 323113 (Commercial Screen Printing). The majority of these establishments (74%) had fewer than 10 employees. Full Analysis

Graphic Arts Employment—December 2019

Published: January 31, 2020

In December 2019, overall printing employment dropped -0.2% from November, and on a year-over-year basis, it is down -2.4%. Production employment was down -0.5% from November to December (and -4.4% Y/Y) while non-production employment was down -0.1% from November to December—but actually up +1.7% Y/Y. Full Analysis

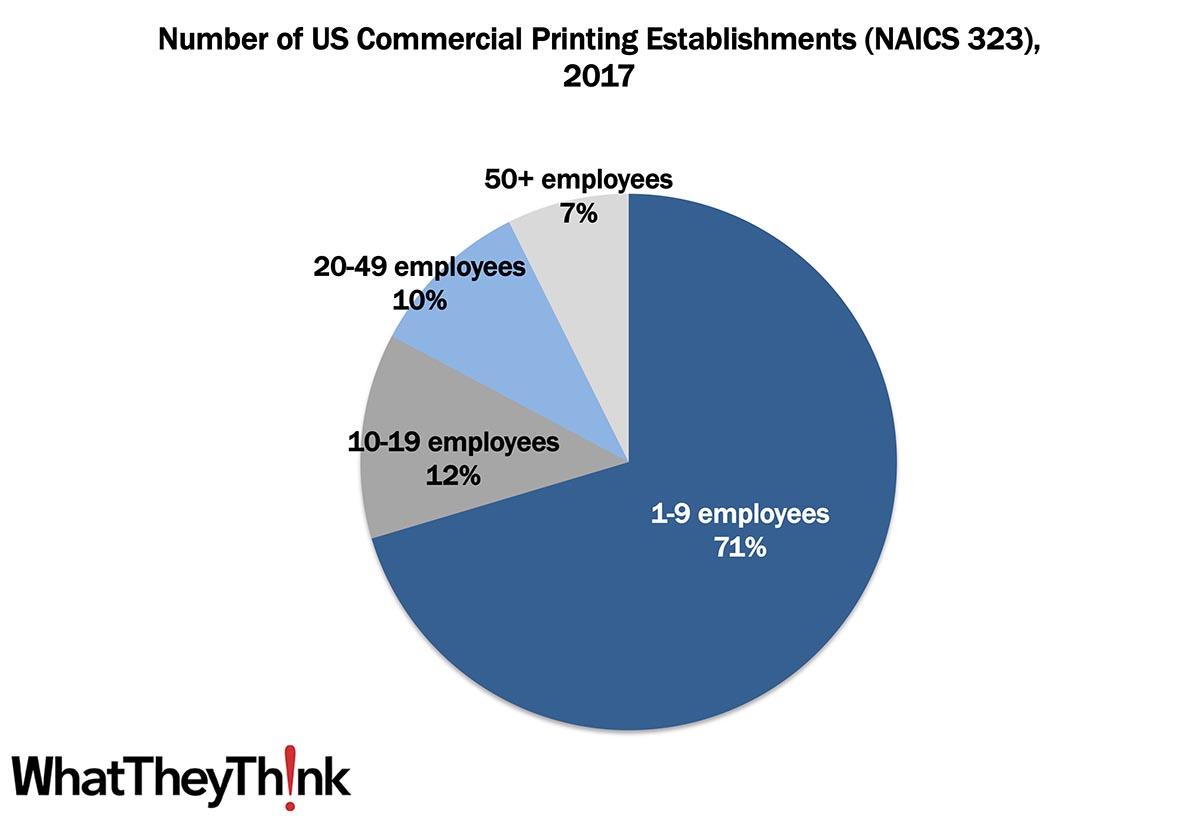

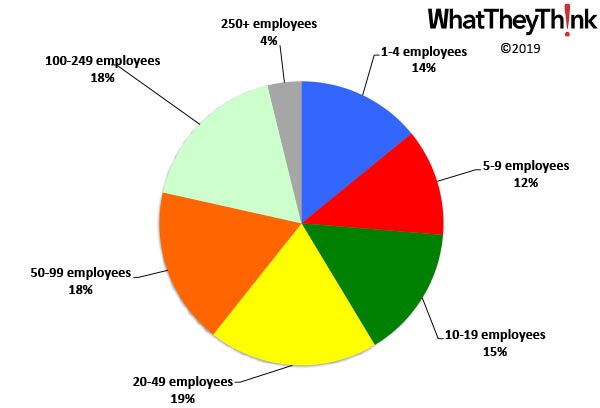

Commercial Printing Establishments—2017

Published: January 24, 2020

The latest edition of County Business Patterns is out, which updates the number of establishments and other data. In 2017, there were 25,256 establishments in NAICS 323 (Printing and Related Support Activities). The majority of these establishments (71%) have fewer than 10 employees. Full Analysis

November Printing Shipments: Off for the Holidays

Published: January 17, 2020

The value of printing shipments for November 2019 was $7.03 billion—a pretty big drop from October’s $7.65 billion, but we kind of expected it, as November and December see business slow down for the holidays. Full Analysis

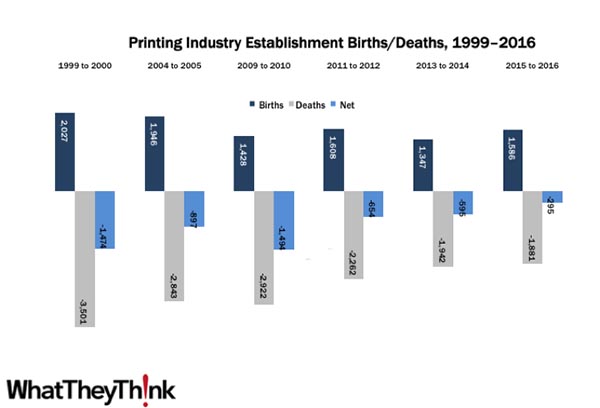

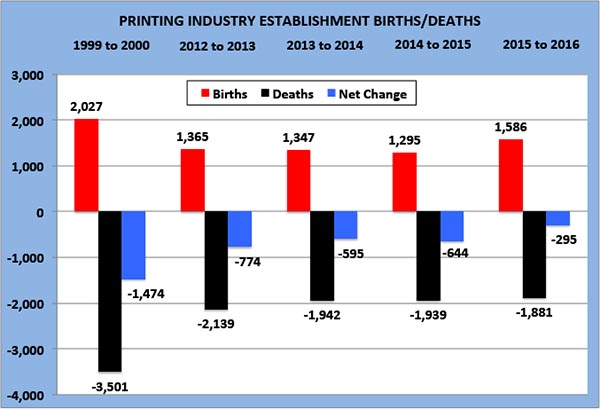

Establishment Births/Deaths: Industry Attrition Continues to Slow

Published: January 10, 2020

From 2015 to 2016, there had been an increase of 1,586 establishments, but a decrease of -1,881 establishments, for a net loss of -295 establishments. That’s a smaller percentage change than previous years, which reflects somewhat of a deceleration in industry consolidation. Full Analysis

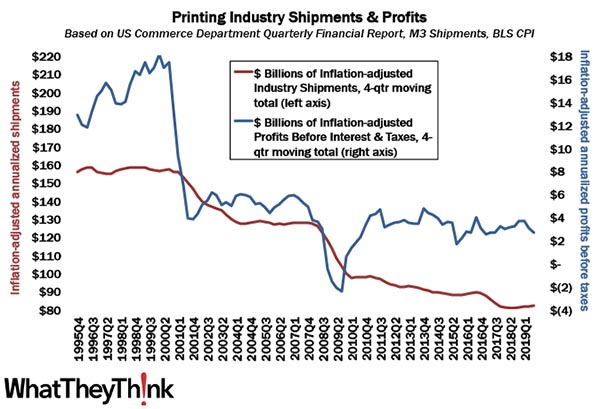

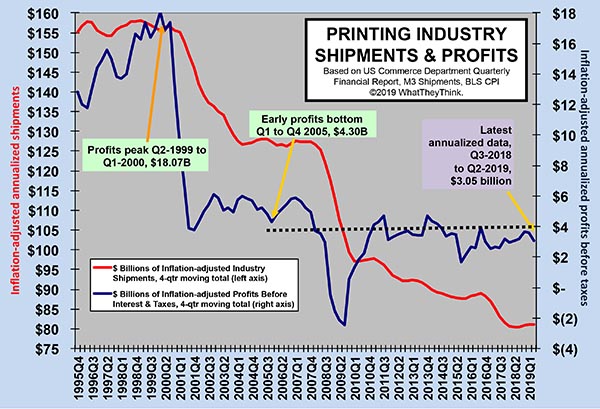

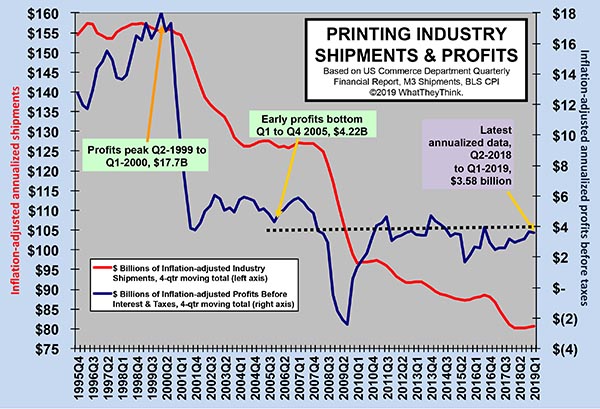

The Next Chapter in the Printing Profits “Tale of Two Cities”

Published: December 20, 2019

Industry profits data for the third quarter of 2019 were down from $3.05 billion in Q2 to $2.65 billion. Large printers continue to be the trouble spot. Full Analysis

October Printing Shipments: Raise a Glass of Holiday Cheer

Published: December 13, 2019

The value of printing shipments for October 2019 was $7.65 billion—a pretty big jump from September’s $7.14 billion. October has become the biggest month of the year, and this is the best October the industry has had since 2016. Full Analysis

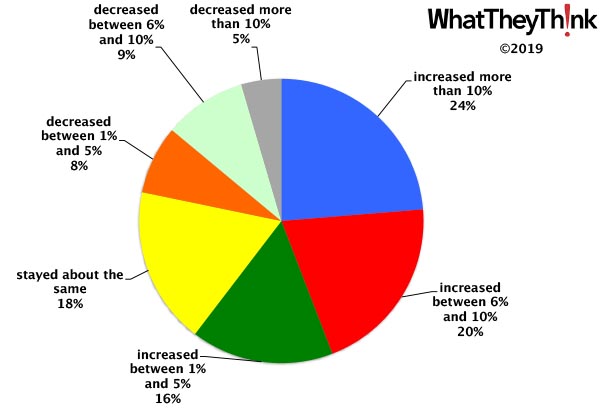

First Look: Industry Business Conditions 2019

Published: December 6, 2019

Preliminary results from our 2019 Business Outlook Survey show that one-fourth (24%) of survey respondents reported that, compared to 2018, revenues for 2019 were up more than 10%. That’s the highest this has been since we started our annual survey in 2015. Elsewhere, though, things are a bit more muted. Full Analysis

October Jobs: Production Down, Managerial Up

Published: November 22, 2019

In October, overall printing employment dropped -0.3% from September. On a year-over-year basis, though, it was down -2.4%. Production employment was down -0.7% from September to October, but year-over-year was down -4.8%. On the other hand, non-production employment was up +0.7% from September to October, and year-over-year was up +2.9%. Full Analysis

Paperboard Container Manufacturing Establishments—2016

Published: November 15, 2019

In 2016, there were 1,971 establishments in NAICS 32221 (Paperboard Container Manufacturing). One-half of these establishments have 50 or more employees, and three-fourths have 20 or more employees. Full Analysis

No Fall for Printing Shipments

Published: November 8, 2019

Heading into Fall 2019, the value of printing shipments for September 2019 was $7.14 billion—up from August’s $7.10 billion. It’s not a huge rise, but given that for the last few years September shipments declined from August’s, we’ll take it. Full Analysis

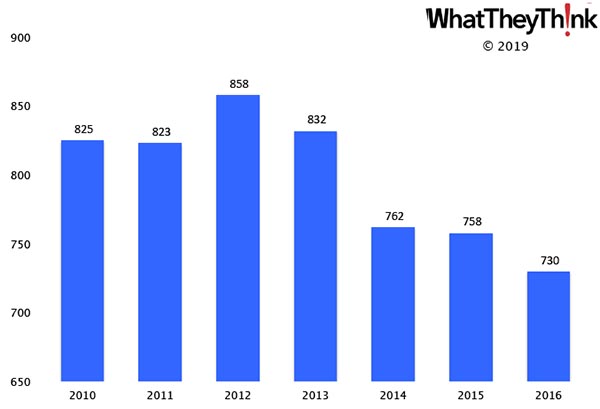

Paper Bag and Coated and Treated Paper Manufacturing—2010–2016

Published: November 1, 2019

In 2010, there were 825 establishments in NAICS 32222 (Paper Bag and Coated and Treated Paper Manufacturing). By 2016, that number had declined for a net loss of -12% to 730. Full Analysis

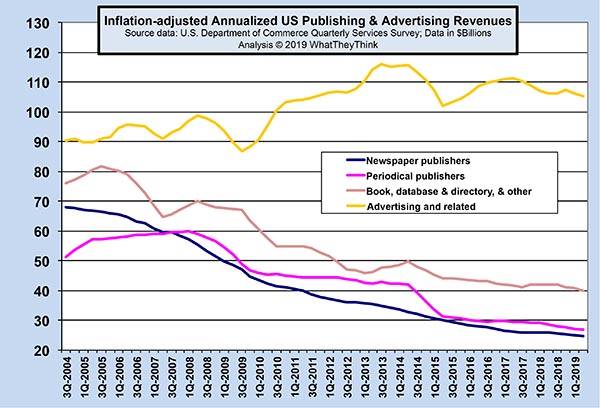

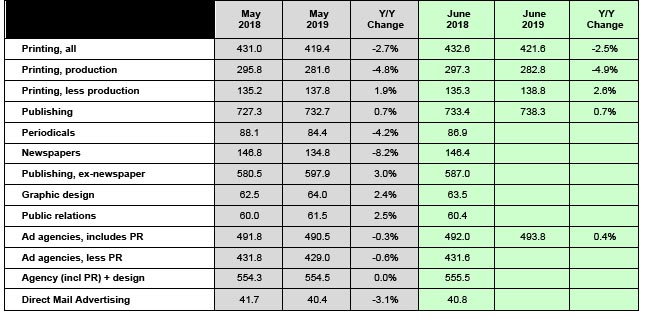

The View from the Other Side: Print Buyers’ Revenues

Published: October 25, 2019

Publishing and advertising are among the biggest print-buying markets. Last month, the Census Bureau released its Quarterly Services Survey, which reported revenues for these markets. Publishers’ revenues continue their long decline, while the up-and-down of advertising revenues indicate the extent to which the nature of advertising is changing. Full Analysis

Paper Bag and Coated and Treated Paper Manufacturing Establishments—2016

Published: October 18, 2019

In 2016, there were 730 establishments in NAICS 32222 (Paper Bag and Coated and Treated Paper Manufacturing). Nearly four out of 10 (39%) have 50 or more employees, and 59% have 20 or more employees. Full Analysis

Printing Shipments: The Dog Days of Summer Didn’t Bite

Published: October 11, 2019

The value of printing shipments for August 2019 was $7.1 billion—up from July’s $6.8 billion. As we head into the autumn, 2019 is shaping up to be the best year for the industry in three years. Full Analysis

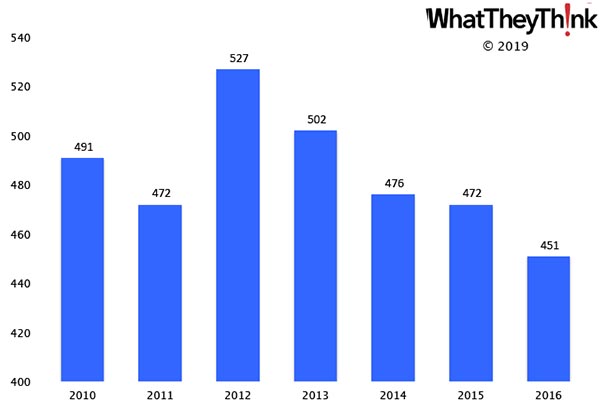

Folding Paperboard Box Manufacturing Establishments—2010–2016

Published: October 4, 2019

In 2010, there were 491 establishments in NAICS 322212 (Folding Paperboard Box Manufacturing). By 2016, that number had declined for a net loss of -8% to 451. Full Analysis

Printing Shipments: Summer Surprise

Published: September 27, 2019

The value of printing shipments for July 2019 was $6.8 billion—up from June’s $6.6 billion. Breaking with seasonality, what has typically been one of the lowest months of the year for printing shipments actually came in pretty good. Full Analysis

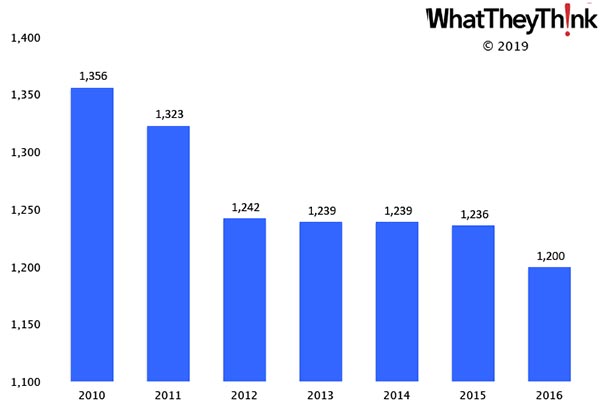

Corrugated and Solid Fiber Box Manufacturing Establishments—2010–2016

Published: September 20, 2019

In 2010, there were 1,356 establishments in NAICS 322211 (Corrugated and Solid Fiber Box Manufacturing). By 2016, that number had declined -12% to 1,200. Full Analysis

Industry Profits: Mind the Gap

Published: September 13, 2019

Annualized profits for the second quarter of 2019 were down from $3.61 billion in Q1 to $3.05 billion. However, the gap between large and small printers has only narrowed very slightly. Full Analysis

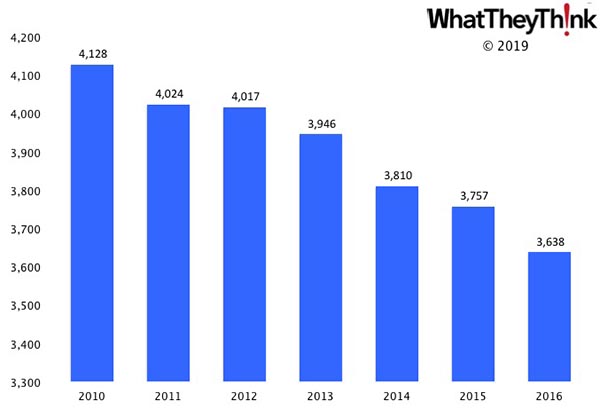

Converted Paper Product Manufacturing Establishments—2010–2016

Published: September 6, 2019

In 2010, there were 4,128 establishments in NAICS 3222 (Converted Paper Product Manufacturing). By 2016, that number had declined -12% to 3,638. Full Analysis

Printing Establishment Births and Deaths

Published: August 30, 2019

From 2015 to 2016, there was an increase of +1,586 printing establishments and a decrease of -1,881 establishments, for a net loss of -295 establishments. Full Analysis

Folding Paperboard Box Manufacturing Establishments—2016

Published: August 23, 2019

In 2016, there were 451 establishments in NAICS 322212 (Folding Paperboard Box Manufacturing). More than half of these establishments (57%) have 50 or more employees and more than three-fourths (79%) have 20 or more employees. Full Analysis

June Printing Shipments: The Dog Days of Summer Begin

Published: August 16, 2019

Printing shipments for June 2019 were—as expected—down from May, and came in slightly below June 2018. Full Analysis

Corrugated and Solid Fiber Box Manufacturing Establishments—2016

Published: August 9, 2019

in 2016, there were 1,200 establishments in NAICS 322211 (Corrugated and Solid Fiber Box Manufacturing). About half of these establishments (49%) have 50 or more employees and more than two-thirds (71%) have 20 or more employees. Full Analysis

June Jobs: Up in the Short Term, Down in the Long Term

Published: August 2, 2019

In June, overall printing employment grew +0.5% from May to June 2019. On a year-over-year basis, it is down -2.5%. Production employment was up +0.4% from May to June, but year-over-year was down -4.9%. Non-production employment was up +0.7% from May to June, and year-over-year was up +2.6%. Full Analysis

Converted Paper Product Manufacturing Establishments—2016

Published: July 26, 2019

in 2016, there were 3,638 establishments in NAICS 3222 (Converted Paper Product Manufacturing). More than four out of 10 of these establishments (42%) have 50 or more employees and two-thirds (65%) have 20 or more employees. Full Analysis

May Printing Shipments Up from April

Published: July 19, 2019

Printing shipments for May 2019 were up from April—and even came in above May 2018 shipments, albeit only very slightly. Full Analysis

PR Agency Employees—2010–2016

Published: July 12, 2019

In 2016, there were 58,489 employees in establishments in NAICS 54182 (Public Relations Agencies). Employment in this category has grown +17% from 2010 to 2016. Full Analysis

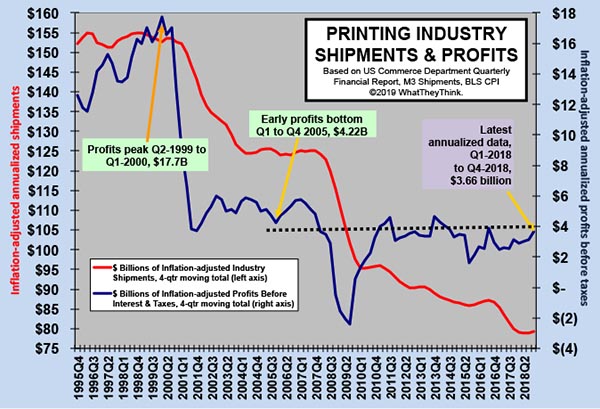

Printing Industry Profits: What Goes Up...

Published: June 28, 2019

Industry profits data came out earlier this month, and overall profits slipped a little. Annualized profits for Q1 2019 were $3.58 billion, down slightly from $3.66 billion in Q4 of last year. Again, it’s the large printers that are dragging down overall industry profitability. Full Analysis

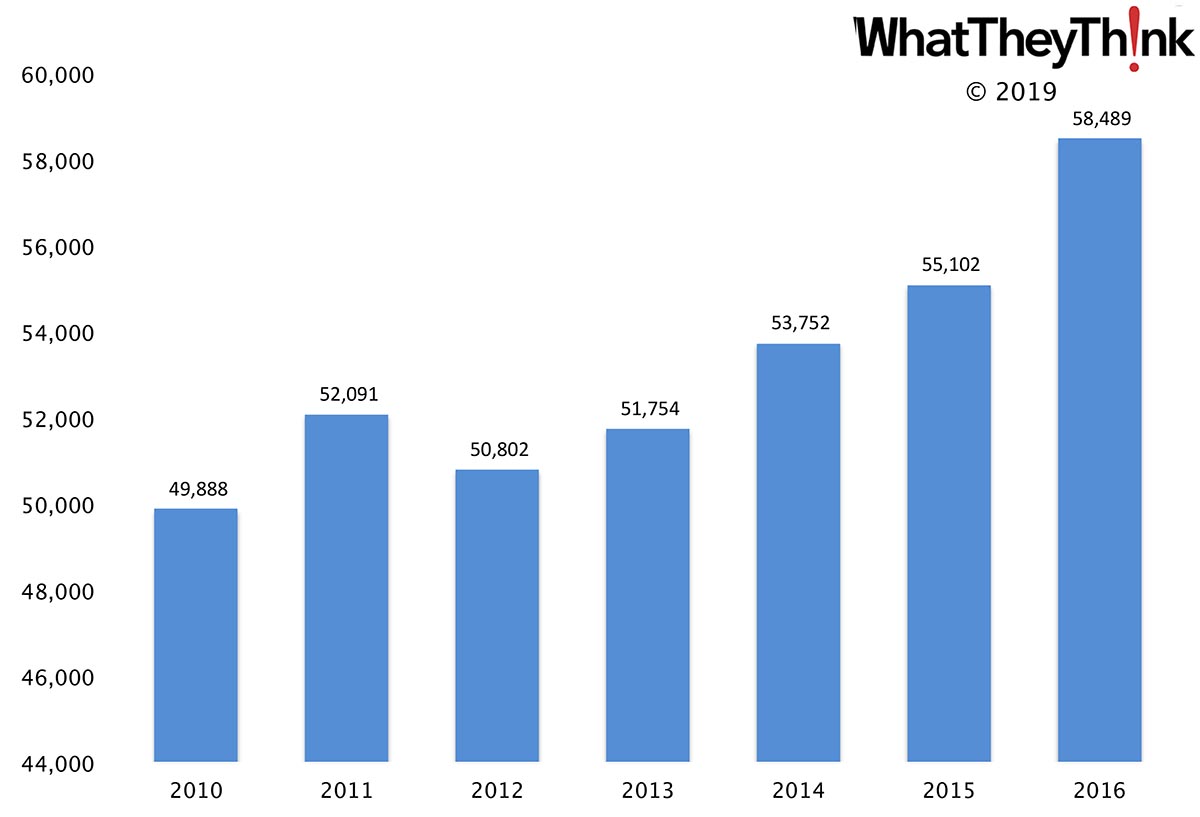

Advertising Agency Employees—2010–2016

Published: June 21, 2019

In 2016, there were 194,792 employees in establishments in NAICS 54181 (Advertising Agencies). Employment in this category has grown +31% from 2010 to 2016. Full Analysis

April Printing Shipments—A New Season?

Published: June 14, 2019

Printing shipments for April were up from March, happily disrupting what has become the usual seasonal pattern. Even better, April 2019 shipments came in above April 2018 shipments. Full Analysis

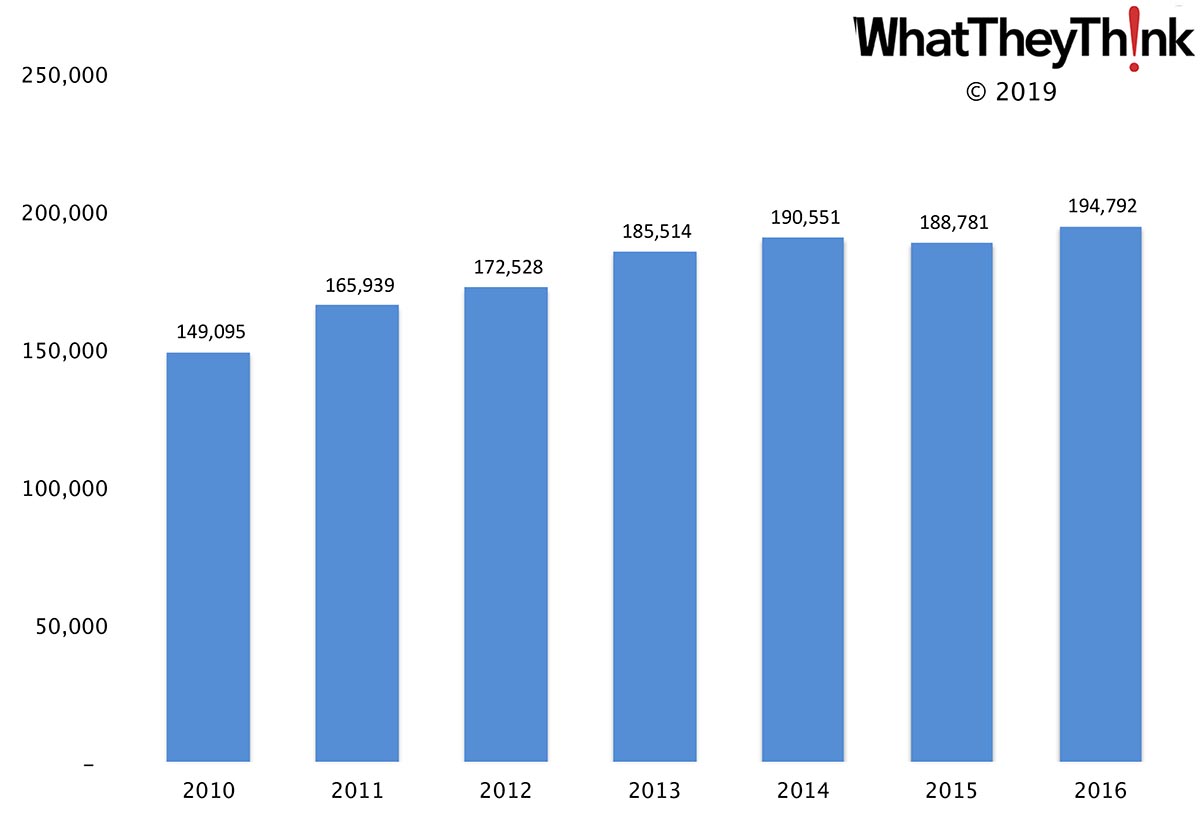

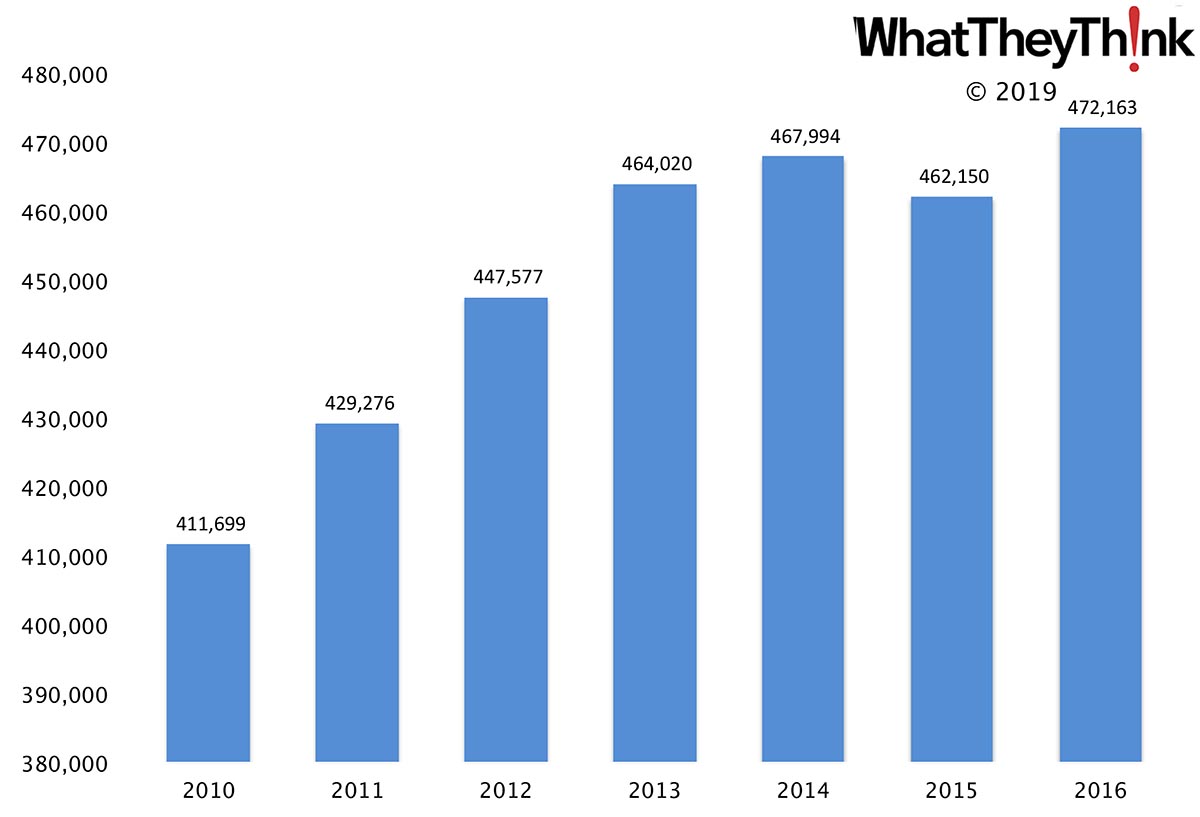

Advertising, Public Relations, and Related Services Employees—2010–2016

Published: June 7, 2019

In 2016, there were 472,163 employees in establishments in NAICS 5418 (Advertising, Public Relations, and Related Services). Employment in this category has grown +15% from 2010 to 2016. Full Analysis

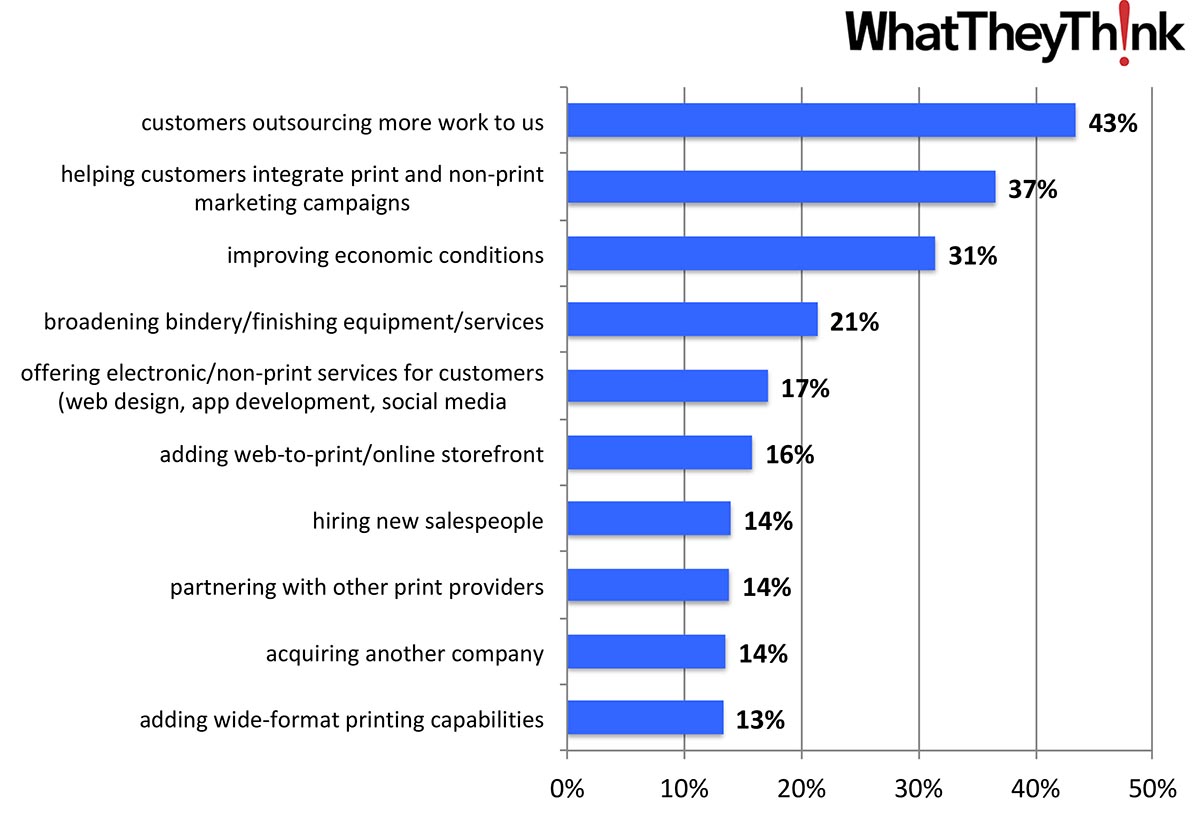

The Changing Face of Print Business Opportunities

Published: May 31, 2019

In our annual Print Business Outlook Survey, we found that the top opportunities for print businesses included some newer, proactive items, with some of the old chestnuts falling off the tree. As we saw with recent Business Challenges, could this reflect a “changing of the guard” of print business management? Full Analysis

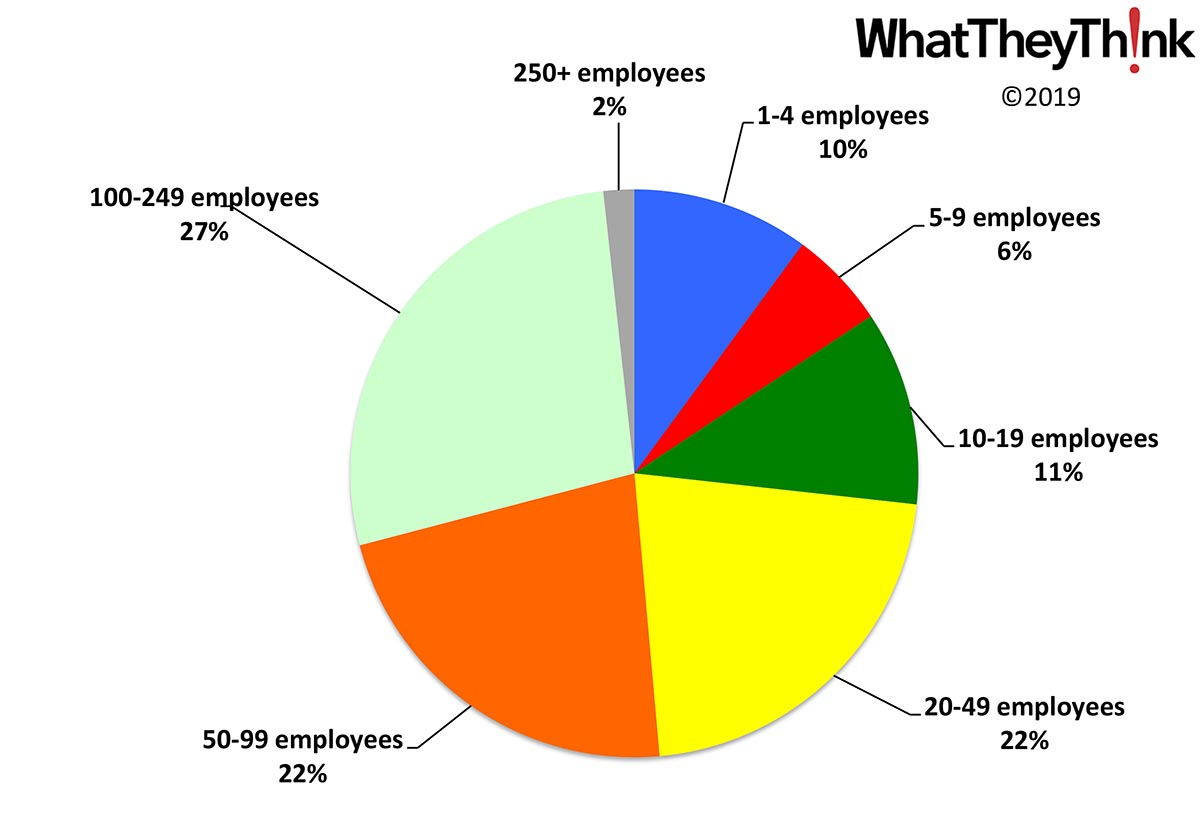

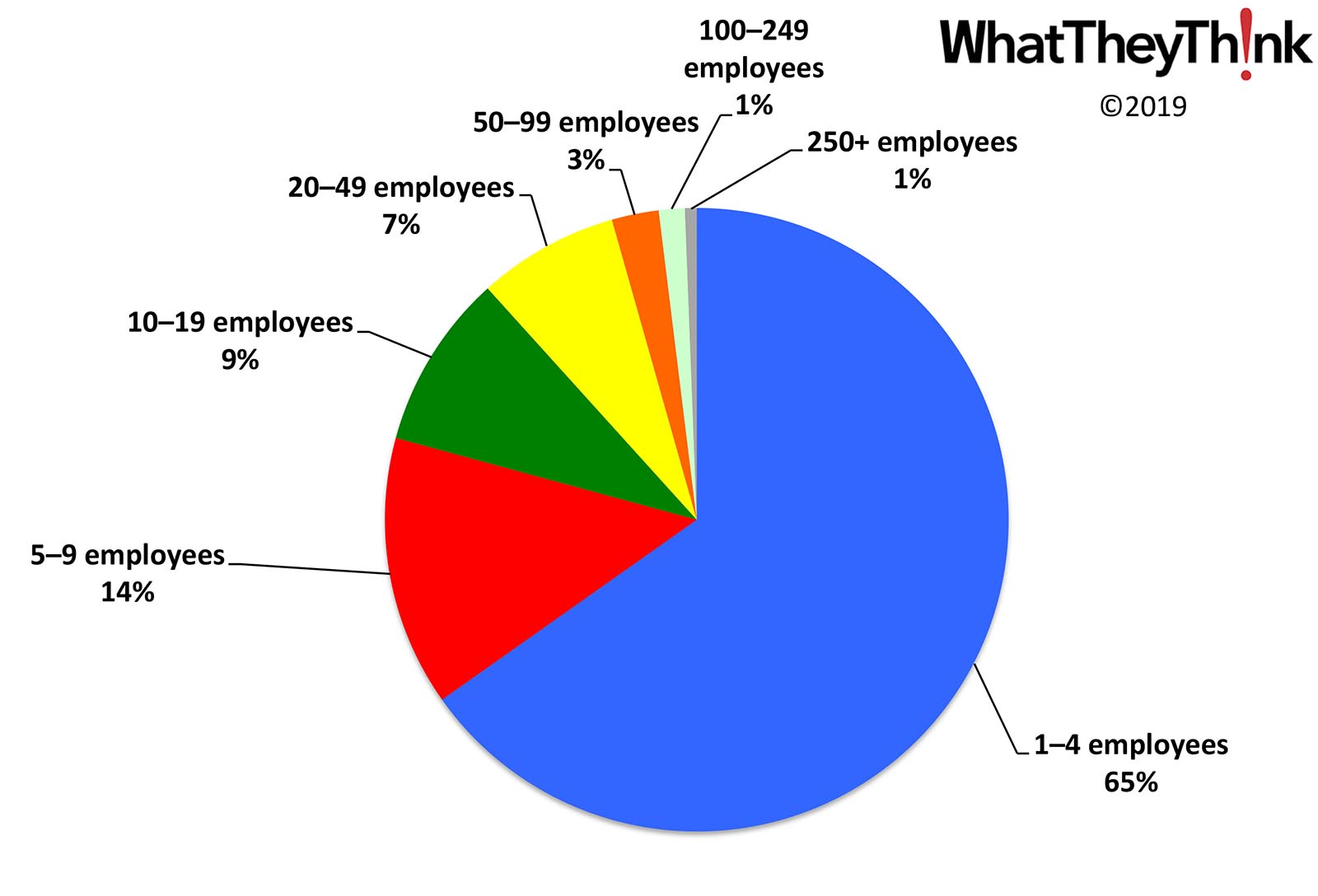

Advertising, Public Relations, and Related Services Establishments—2016

Published: May 24, 2019

in 2016, there were 37,875 establishments in NAICS 5418 (Advertising, Public Relations, and Related Services). Two-thirds of these establishments (65%) have under four employees, 79% have under 10 employees, and 88% have under 20 employees. The largest agencies (100 or more employees) only account for 2% of all establishments. Full Analysis

March Printing Shipments: A Day at the Races

Published: May 17, 2019

The value of printing shipments for March were up from February. However, at $6.66 billion, March 2019 shipments came in below March 2018’s $6.74 billion. That’s not a huge disappointment, but we were hoping for a better month. Full Analysis

Printing’s Labor's Lost?

Published: May 10, 2019

Overall printing employment dropped -0.7% from March to April 2019 and on a year-over-year basis is down -2.9%. Production employment dropped a tad from March to April, and is down -4.5% from April 2018. Non-production employment was up +0.6% from April 2018 to April 2019. Full Analysis

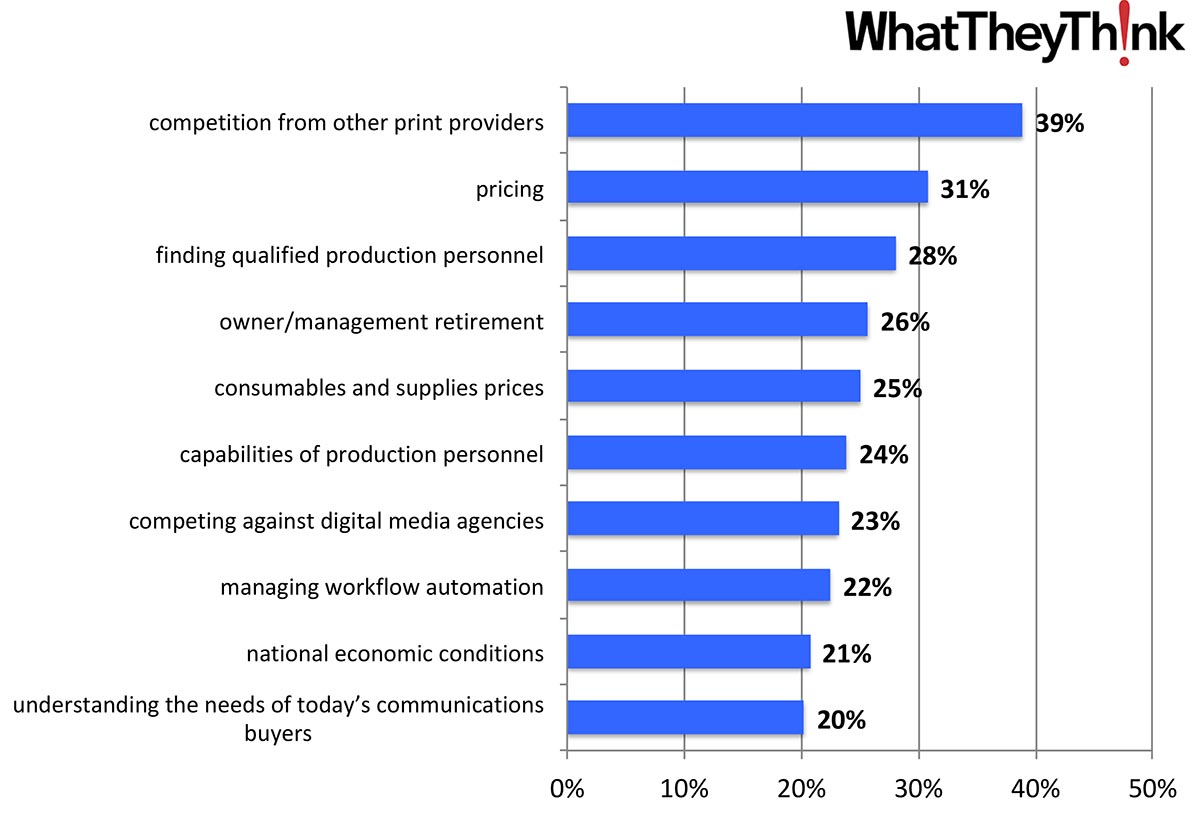

Print Business Challenges: Some Old Cares, Some New Concerns

Published: May 3, 2019

In Winter 2018/2019, we conducted our annual Print Business Outlook Survey and found that the top challenges for print businesses included some new cares and concerns with some of the old challenges falling by the wayside. Could this reflect a “changing of the guard” of print business management? Full Analysis

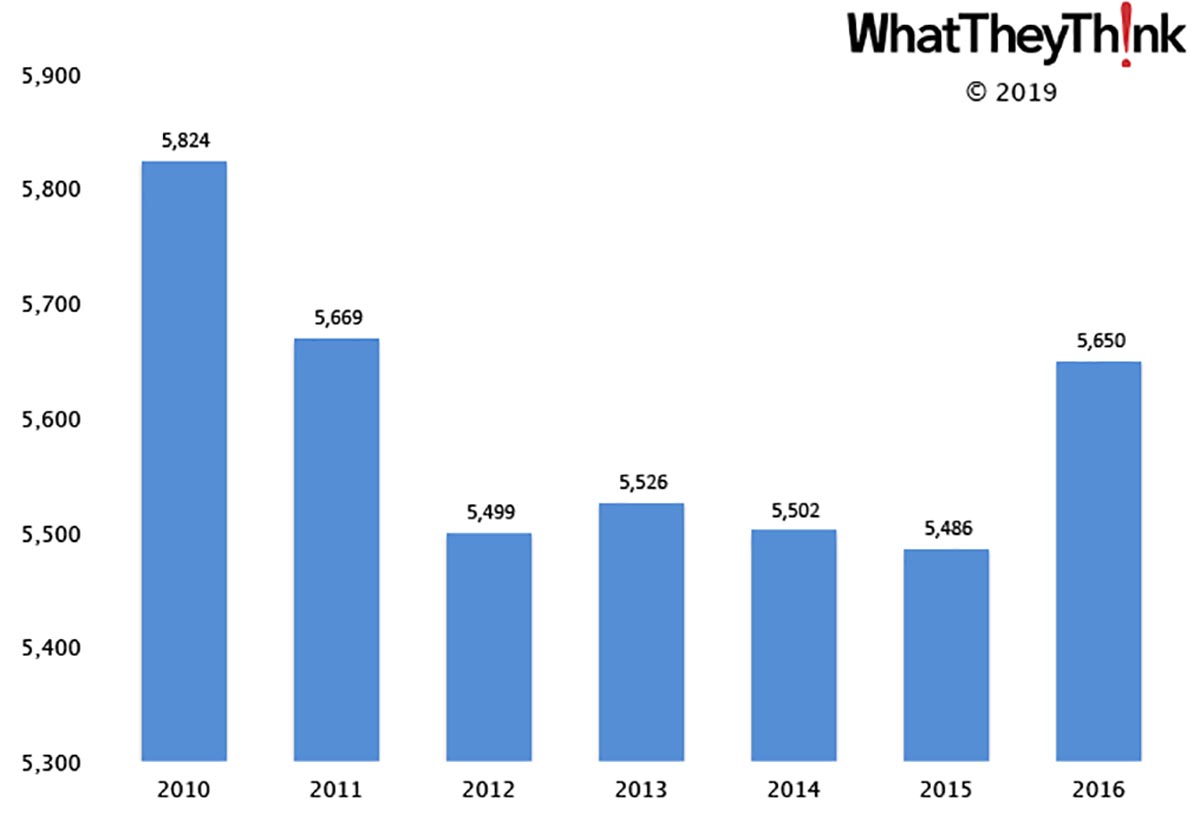

Sign Manufacturers—2010–2016

Published: April 26, 2019

In 2016, there were 5,650 Sign Manufacturing establishments (NAICS 33995). The decline and rise of sign manufacturing over the course of the 2010s reflects the impact of the Great Recession, as well as the recovery and the growth of digital printing into traditional signmaking. Full Analysis

February 2019 Printing Shipments: Starting the Year Off on the Right Foot

Published: April 19, 2019

Printing shipments for February 2019 came in at $6.08 billion. In keeping with the industry’s seasonality, it’s down from January, but so far 2019 shipments are higher than 2018’s. Full Analysis

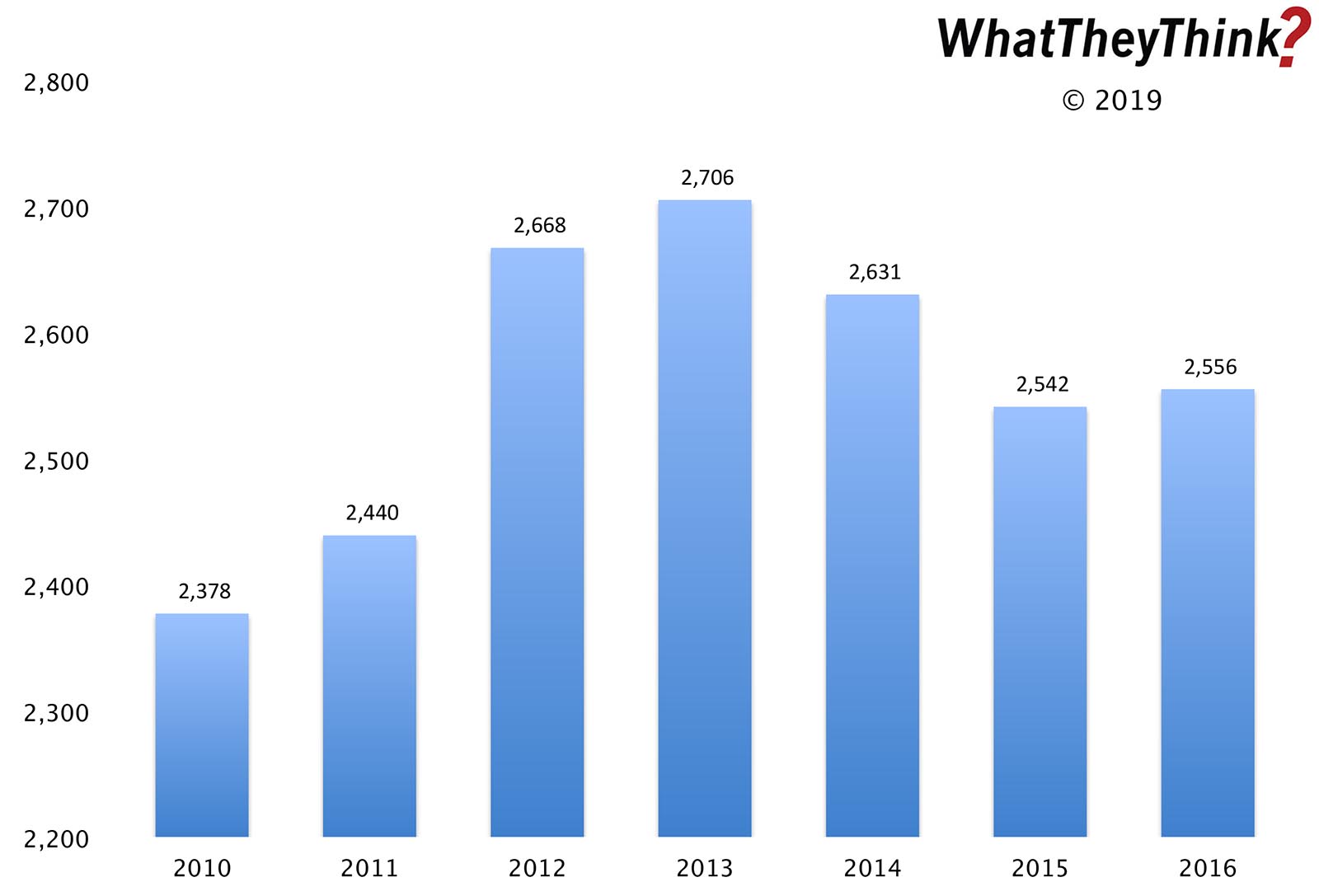

Outdoor Advertising Establishments—2010–2016

Published: April 12, 2019

In 2016, there were 2,556 establishments classified as Outdoor Advertising (NAICS 54185). In 2010, NAICS 54185 comprised 2,378 establishments—but note that the Census Bureau changed the name of this category in 2012. Full Analysis

Business Conditions: Up in 2018, Optimism High for 2019

Published: April 5, 2019

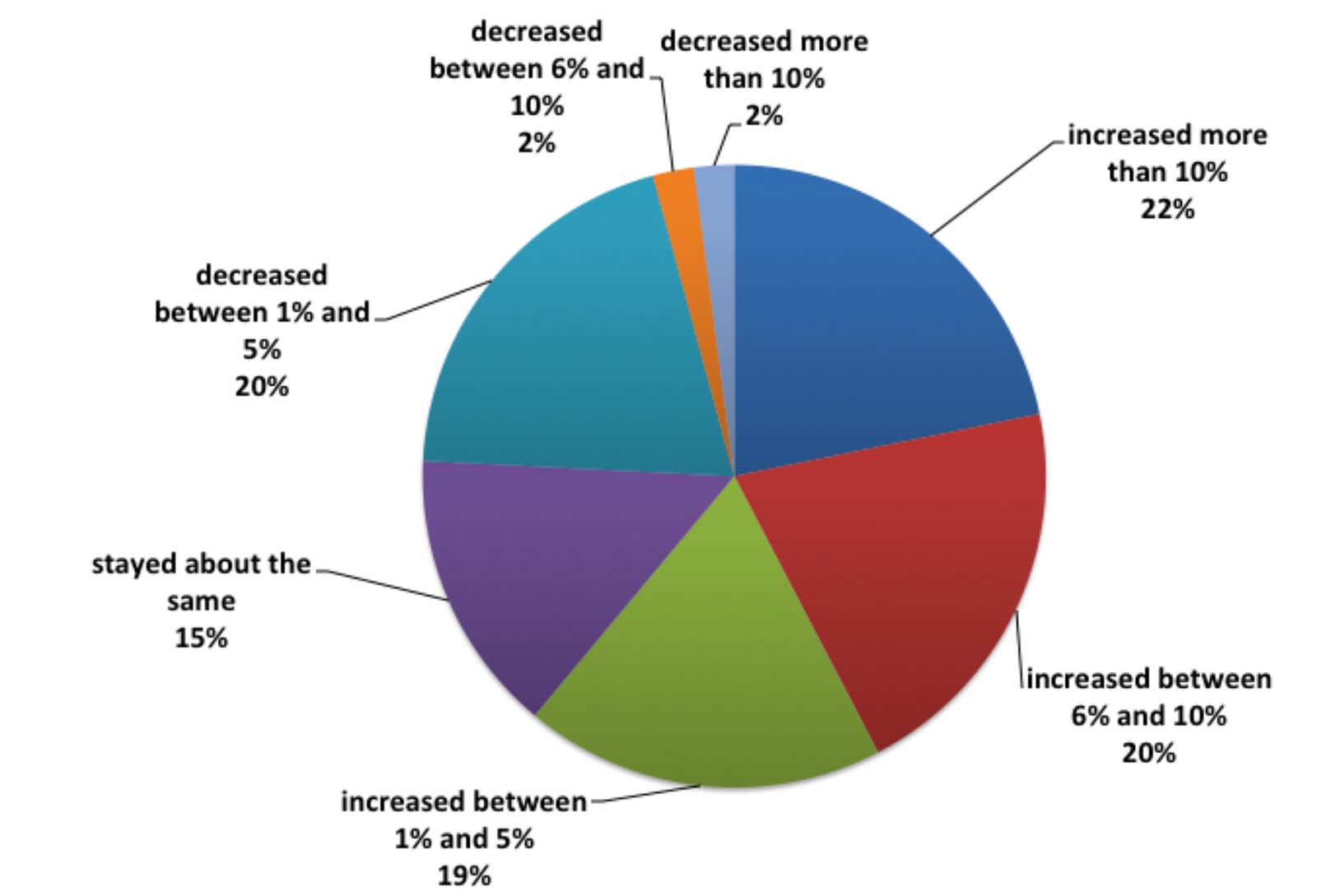

In Winter 2018/2019, we conducted our annual Print Business Outlook Survey and found that business in 2018 was perceived by survey respondents as overall pretty good: 42% said that revenues had increased by six percent or more compared to 2017. Full Analysis

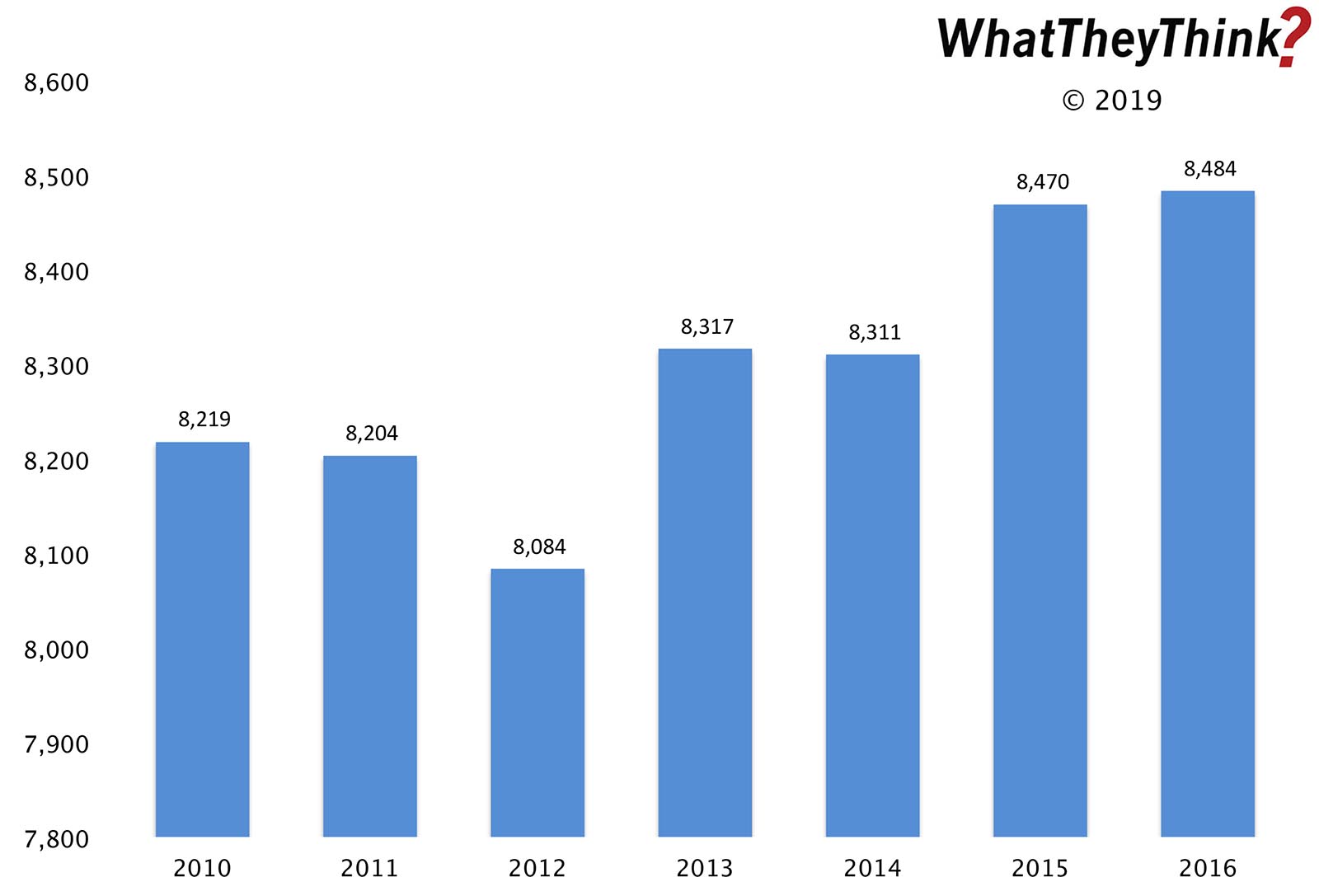

PR Establishments—2010–2016

Published: March 29, 2019

In 2010, there were 8,219 establishments classified as PR Agencies. By 2016, there had been a net gain of +3.2%. Full Analysis

Printing Industry Profits: Urban Sprawl in the Tale of Two Cities

Published: March 22, 2019

Overall, annualized printing industry profits for Q4 2018 were $3.66 billion—not a massive gain from Q3 but a gain nonetheless (we’ll take it). It also appears that the “tale of two cities” trend is—at least temporarily—on hold. Full Analysis

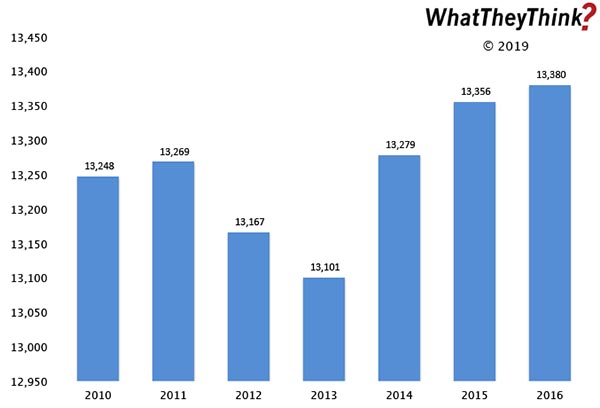

Advertising Agency Establishments—2010–2016

Published: March 15, 2019

In 2010, there were 13,248 establishments classified as Advertising Agencies. By 2016, there had been a net gain of +1.0%, the ups and downs reflecting the changing role of the ad agency. Full Analysis

December 2018 Printing Shipments: Ending 2018 on a High(ish) Note

Published: March 8, 2019

Printing shipments for December 2018 came in at $6.40 billion. In keeping with the industry’s new seasonality, that’s down from November, but higher than December 2017—but just barely. Full Analysis

Advertising and Related Establishments—2010–2016

Published: March 1, 2019

In 2010, there were 38,335 establishments classified as Advertising, Public Relations, and Related Services. By 2016, there had been a net loss of -1.2%. This is a very broad industry classification, comprising a disparate bunch of business types, each of which has its own unique dynamics. Full Analysis

Printing Shipments as a Percentage of GDP

Published: February 22, 2019

Since 1997, the value of printing shipments went from around 0.75% of GDP all the way down to about 0.35%. So we should not be surprised that parts of the printing industry are falling off the government’s radar. Full Analysis

![]()

- New RISO Printing Unit Offers Easy Integration for Package Printing

- March 2024 Inkjet Installation Roundup

- Inkjet Integrator Profiles: Integrity Industrial Inkjet

- Revisiting the Samba printhead

- 2024 Inkjet Shopping Guide for Folding Carton Presses

- The Future of AI In Packaging

- Inkjet Integrator Profiles: DJM

- Spring Inkjet Update – Webinar

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.