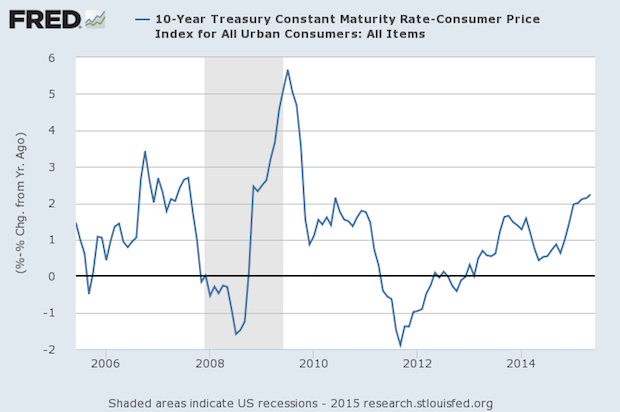

We all know how the markets seem to panic when the Fed hints that rates will be rising soon, but they already have. That is, the markets have been pushing up the inflation-adjusted 10-year US Treasury since September 2011 by 420 basis points (4.2 percentage points).

The rate is now the highest since June 2010, at 2.33%. This measure can be volatile because of the inflation adjustment. We used the year-to-year inflation rate as measured by the Consumer Price Index for that reason. There are Fed governors who believe that they have great latitude to be patient with a rise in inflation since their target of +2% annual inflation has not been met. This means that they believe they have a cushion of “banked” uncreated inflation that they can use up before they move aggressively.

Whatever the case, a 25 basis point rise in short term rates is not much, as they might actually be catching up to the marketplace that has already moved and the Fed is already lagging well behind it. They miss an important point. The CPI does not measure inflation in a practical way. If wages are stagnant (though a little better lately), a “mild” 2% rise can be a burden.

Median household income is still 4% lower than its peak just after the recession started. A 2% rise in inflation plus the 4% lower income is a 6% difference. That's something that's rarely mentioned in the business press.

We all know how the markets seem to panic when the Fed hints that rates will be rising soon, but they already have. That is, the markets have been pushing up the inflation-adjusted 10-year US Treasury since September 2011 by 420 basis points (4.2 percentage points).

The rate is now the highest since June 2010, at 2.33%. This measure can be volatile because of the inflation adjustment. We used the year-to-year inflation rate as measured by the Consumer Price Index for that reason. There are Fed governors who believe that they have great latitude to be patient with a rise in inflation since their target of +2% annual inflation has not been met. This means that they believe they have a cushion of “banked” uncreated inflation that they can use up before they move aggressively.

Whatever the case, a 25 basis point rise in short term rates is not much, as they might actually be catching up to the marketplace that has already moved and the Fed is already lagging well behind it. They miss an important point. The CPI does not measure inflation in a practical way. If wages are stagnant (though a little better lately), a “mild” 2% rise can be a burden.

Median household income is still 4% lower than its peak just after the recession started. A 2% rise in inflation plus the 4% lower income is a 6% difference. That's something that's rarely mentioned in the business press.

{kind=link}