# # #

# # #

Commentary & Analysis

June to October US Commercial Printing Shipments Up +$1 Billion Versus 2013

The industry had another good month compared to last year,

The industry had another good month compared to last year, with October shipments more than $7.1 billion, up $274 million (+4.0%, +$167 million or +2.4% after adjusting for inflation).

June through October shipments are up +$1.05 billion (+$404 million with inflation adjustment). September shipments were revised higher by $45 million. The industry has had positive comparisons to 2013 for four of the last five months, even after adjusting for inflation.

Shipments remain below 2012 levels.

This recent change in shipments direction should be used by printers as breathing room to continue to reconfigure their product offerings and increase their relevance in the communications strategies of their clients. Digital technologies are still declining in cost, increasing in speed, and improving in ease of use. While there are concerns about the effectiveness of many digital formats, the pendulum is likely to swing back. Printers should do their best to get out of the way of that pendulum and avoid what happened to many shops in 2008 and 2009.

The USPS recently reported better results in October, and it is likely that these printing data benefited from the increase in standard mail of more than 1 billion pieces more than October 2013. Personally, we have noticed an increase in mailing from retailers, but with smaller pieces with lower page counts, or no page counts at all, as they are often large post cards. Please see our post about those changes.

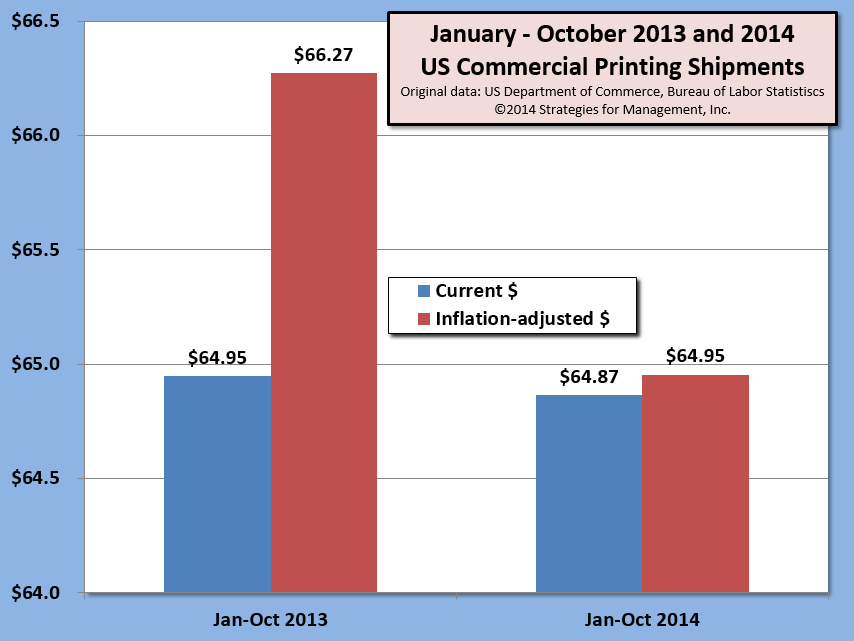

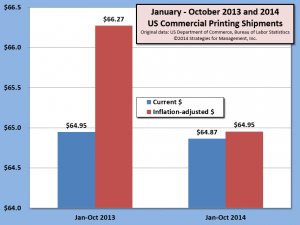

For January through October, current dollar revenues for the printing industry are down -1.0% and -2.7% after inflation. If recent trends prevail, current revenues may surpass 2013's level and inflation-adjusted revenues may pull even with last year. (click to enlarge)

# # #

# # #

# # #

About Dr. Joe Webb

Dr. Joe Webb is one of the graphic arts industry's best-known consultants, forecasters, and commentators. He is the director of WhatTheyThink's Economics and Research Center.

Video Center

![]()

- New RISO Printing Unit Offers Easy Integration for Package Printing

- March 2024 Inkjet Installation Roundup

- Inkjet Integrator Profiles: Integrity Industrial Inkjet

- Revisiting the Samba printhead

- 2024 Inkjet Shopping Guide for Folding Carton Presses

- The Future of AI In Packaging

- Inkjet Integrator Profiles: DJM

- Spring Inkjet Update – Webinar

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.