Commentary & Analysis

July 2014 Printing Shipments up +2.6%, Two Consecutive Months of Growth

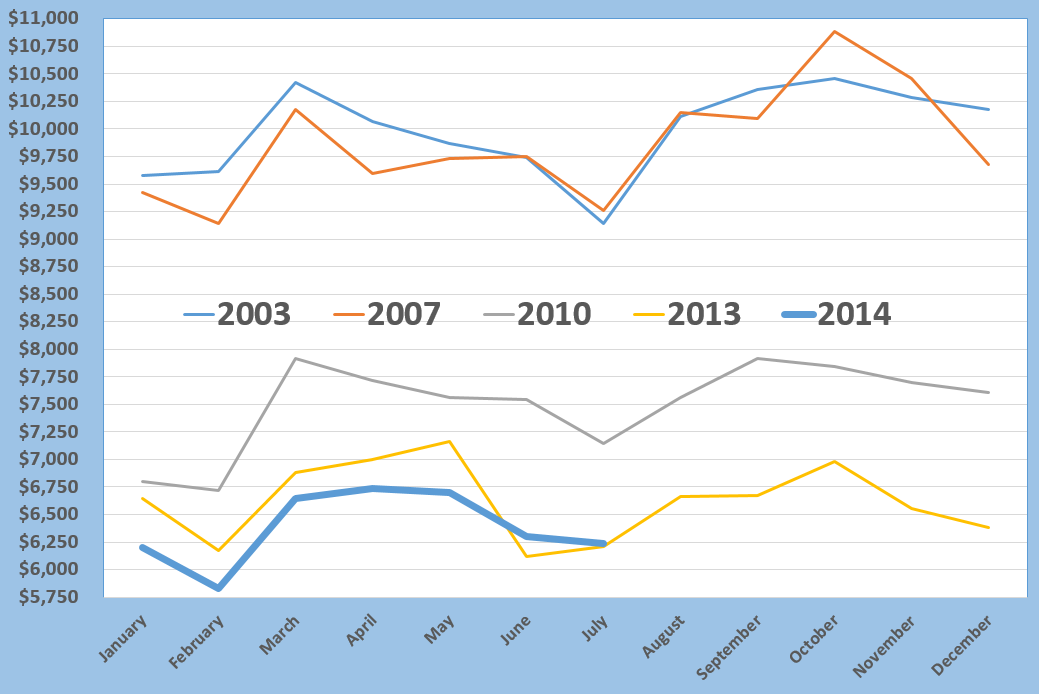

July 2014 US commercial printing shipments were $

July 2014 US commercial printing shipments were $6.24 billion, up +$157 million (+2.6%) compared to 2013 on a current dollar basis, and up +$27 million (+0.4%) on an inflation-adjusted basis.

This is the second month of gains, and it was in what is typically the slowest month of the printing year because of scheduled plant shutdowns for vacations and maintenance.

June's increased shipments were revised up +$73 million, and are now reported as +$325 million compared to 2013 (+5.4%).

June 2013 was a very weak month, and unlike the historical pattern was the worst month of 2013.

For the first seven months of 2014, the industry is down -$647 million on a current dollar basis and -$1.5 billion after inflation adjustment. The past two months, however have been up +$482 million and +$211 million on current and inflation adjusted bases, respectively.

The last time there were two consecutive months of growth on a current dollar basis was February and March 2011, which was the end of an eight month run of positive prior year comparisons that started in August 2010 and averaged +2.3% per month.

The last inflation-adjusted positive pair was January and February 2011, the end of a seven month positive run that also started in August 2010. That run averaged +0.7% per month.

Our advice remains the same: positive months are breathing room for the industry, much as we advised in 2007, 2008, and also 2010, a chance to recover from difficult periods and make investments and restructurings for continuing media shifts ahead. Consolidations that add new capabilities rather than combining similar ones are especially important now. It has been 21 months since the industry booked more than $7 billion in sales, which is a level that was once commonplace.

The chart below shows the inflation-adjusted monthly shipments for selected years (click to enlarge). Shipments data can be found at the Economics & Research Center page.

About Dr. Joe Webb

Dr. Joe Webb is one of the graphic arts industry's best-known consultants, forecasters, and commentators. He is the director of WhatTheyThink's Economics and Research Center.

Video Center

![]()

- New RISO Printing Unit Offers Easy Integration for Package Printing

- March 2024 Inkjet Installation Roundup

- Inkjet Integrator Profiles: Integrity Industrial Inkjet

- Revisiting the Samba printhead

- 2024 Inkjet Shopping Guide for Folding Carton Presses

- The Future of AI In Packaging

- Inkjet Integrator Profiles: DJM

- Spring Inkjet Update – Webinar

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.