Commentary & Analysis

Recovery Indicators Perk Up, But Two are Still Below Recession Levels

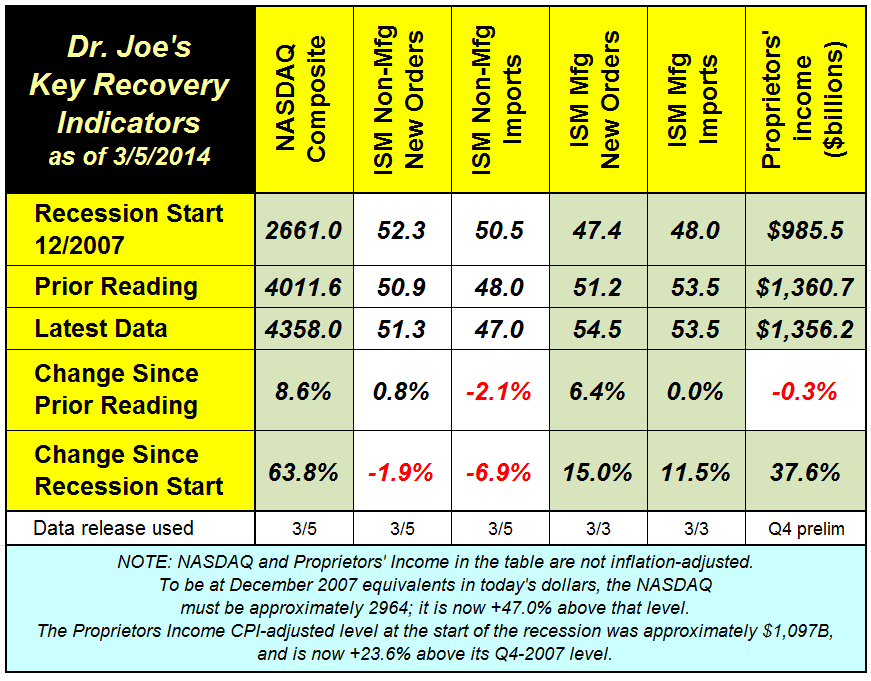

The NASDAQ'

The NASDAQ's disastrous January has been balanced by a strong February, up almost 9% since the recovery indicators were published last month. (click to enlarge)

About Dr. Joe Webb

Dr. Joe Webb is one of the graphic arts industry's best-known consultants, forecasters, and commentators. He is the director of WhatTheyThink's Economics and Research Center.

Video Center

![]()

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.