Commentary & Analysis

Q4-2013 GDP Revised Down from +3.2% to +2.4%, Consistent with Last Month's Analysis

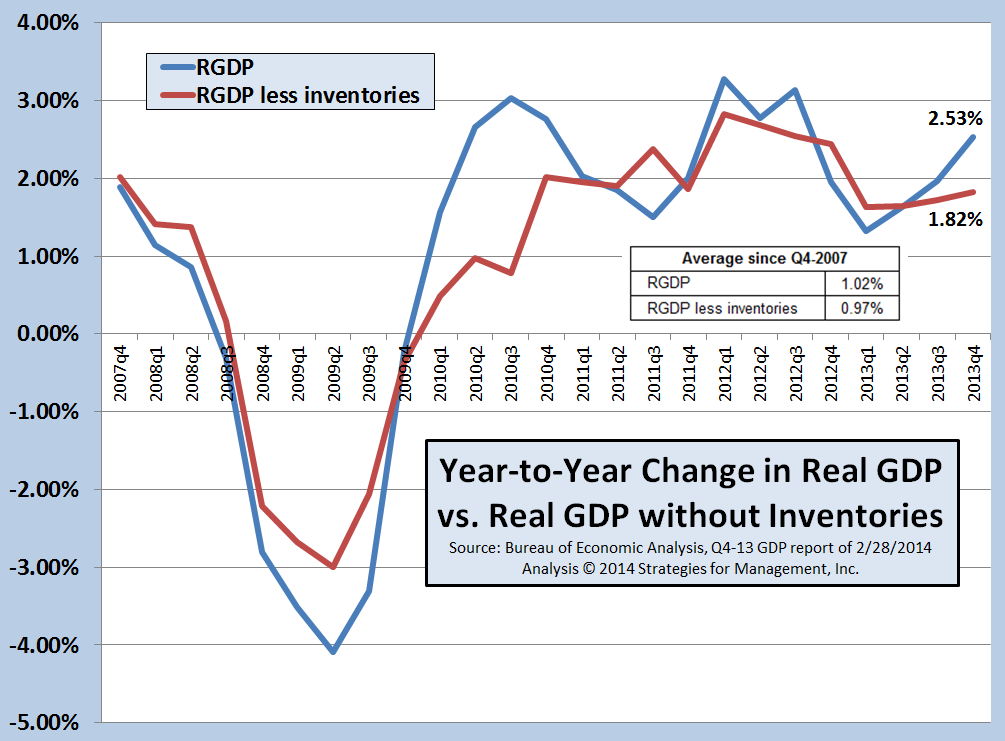

Quarterly GDP data are released three times,

Quarterly GDP data are released three times, and are referred to as "advance," "preliminary," and "final." Advance reports are based on some real data plus a very large portion of estimated data. As time passes, those estimates are replaced by reports of actual data. There are estimates in the final report, but they represent a much smaller portion than in the earlier two reports. There is usually nothing final about statistics, of course. Every Spring, GDP history is revised going back multiple years.

Last month's GDP report was overstated, and was generally understood as such. One of the peculiar aspects of it was a repeat of Q3's increase in inventories. Q4's inventory buildup was reduced to about the same level as Q3. In last month's analysis, we stated that the buildup may have been business executives acting on two certainties, as they saw it, that interest rates would be rising sharply in 2014 as the Fed unwound its QE3 efforts, and per unit labor costs would be rising sharply because of ACA implementation. They seemed like good bets at the time, but they're not turning out that way. The Fed will be moving more cautiously than generally believed in those quarters, and ACA implementation has been delayed for many businesses. This means the disparity in labor costs between Q4-2013 and Q1-2014 will be much less than originally thought.

Unsold inventories look like they are a becoming problem in Q1-2014. Much of the latest data for retail sales, durable goods, and other indicators appear to be weakening. We will have more details and commentary next week when we publish the next set of recovery indicators. Below is an updated chart of real GDP with and without inventories since the beginning of the recession. (click to enlarge)

About Dr. Joe Webb

Dr. Joe Webb is one of the graphic arts industry's best-known consultants, forecasters, and commentators. He is the director of WhatTheyThink's Economics and Research Center.

Video Center

![]()

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.