Commentary & Analysis

Statistical Trends in Print, or, Dr. Joe's Mixed Media Message

The trends in commercial printing demand are often up to debate,

The trends in commercial printing demand are often up to debate, but sometimes statistical analysis can be helpful in understanding them better. Economic events are often the reasons given for shifts in demand and shipments, but that's much to nebulous. We know there are more specific issues, and there is too much general evidence that strong economic growth only makes the adoption rate of digital technologies and media stronger.

In some recent analysis, the regression model of real GDP and CPI-adjusted printing shipments shows that for every billion dollar increase in real GDP results in a -$19.4 million change in commercial print shipments. This regression equation has r²= 71.9%, which is a strong statistical relationship, no matter how unsatisfying (or confusing) the thought is that a growing economy might actually hurt an industry rather than benefit it.

Now is a good time to make the point that statistical relationships change over time. There was a time when this relationship between print and the economy was positive. Also, depending on the starting year of the data series, you can create different results. I can't get a positive result to appear unless I ignore the last decade or more. But I can make the r² change and the dollar relationship to GDP change. The bigger problem with statistical data is that models can only detect change after the change has occurred and been evident for a while. It is a warning sign to managers when models don't reflect reality any longer. When the models say one thing and reality says something else, that's not a problem with the model, it's a problem with management clinging to a model rather than relying on their experience and ability to interpret what they see and experience first hand. Models are intended to help us see new things or to give order to things that seem disordered. Models that don't work tell us as much or sometime more than models that do. (Statistical soapbox time is now finished).

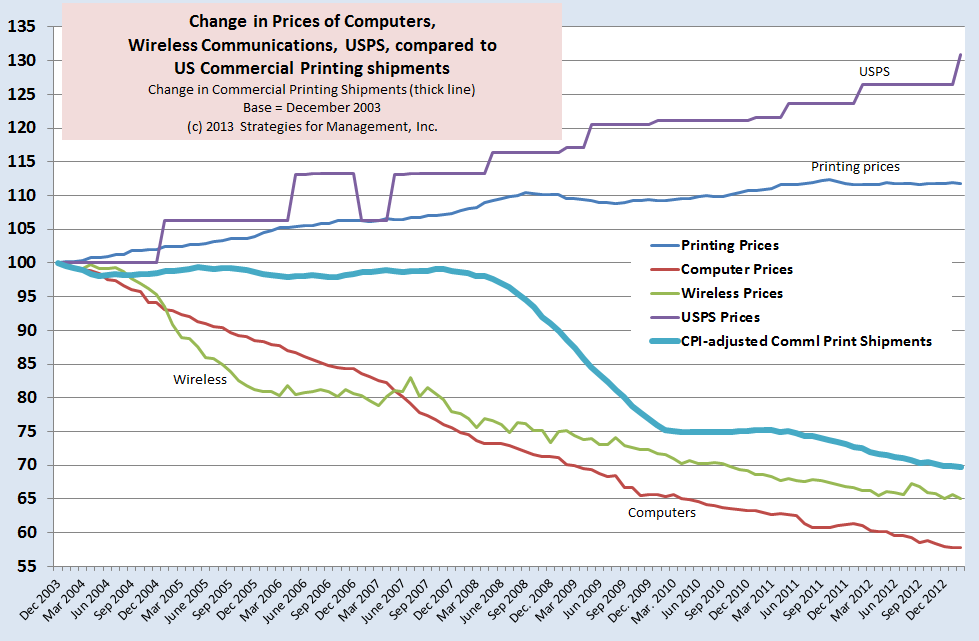

There are other factors that affect demand, notably the prices of other goods, notably computer equipment, wireless communications, and the costs of postage. We compared these data series with printing shipments. The Producer Price Index for computer equipment has an r²=76.9%, and it means that every 1-point positive change in the index equals $337 million more print sales. The only problem is that the PPI for computing equipment keeps going down, so every 1-point negative change is a $337 million decline in print shipments. Since 2000, the PPI for computers has fallen by 58%. If we could just repeal Moore's Law (you know, that computing power doubles every 18 months while the price decreases by half) things would be okay. (click chart to enlarge)

About Dr. Joe Webb

Dr. Joe Webb is one of the graphic arts industry's best-known consultants, forecasters, and commentators. He is the director of WhatTheyThink's Economics and Research Center.

Video Center

![]()

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.