Commentary & Analysis

Latest Commercial Printing Demographics Show 1,200 Fewer Establishments

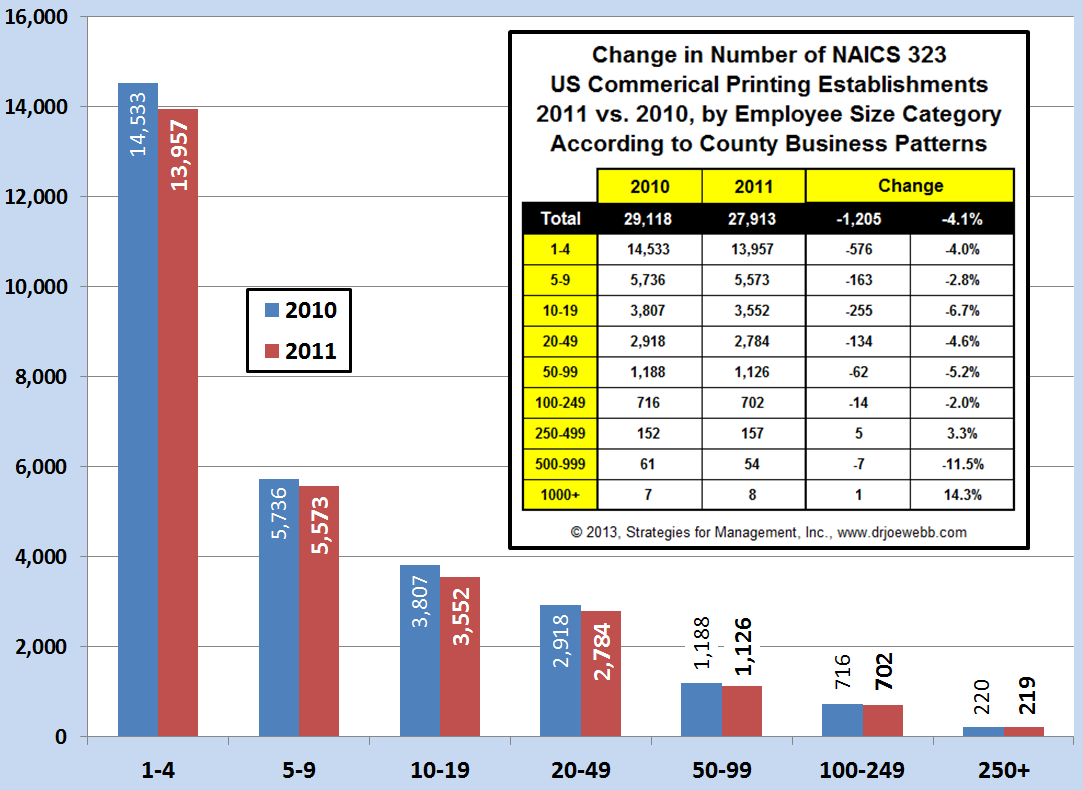

The Commerce Department recently released the latest edition of County Business Patterns data about the number of US business establishments in 2011.

The Commerce Department recently released the latest edition of County Business Patterns data about the number of US business establishments in 2011. Those data indicated that commercial printing establishments declined -4.1% compared to 2010. The biggest percentage declines were in establishments with 500 to 999 employees (between about $90 million to $200 million in sales), which fell by -11.5%, and establishments with 10 to 19 employees (about $1.5 million to $3.5 million) which fell -6.7%. (click chart to enlarge)

About Dr. Joe Webb

Dr. Joe Webb is one of the graphic arts industry's best-known consultants, forecasters, and commentators. He is the director of WhatTheyThink's Economics and Research Center.

Video Center

![]()

- New RISO Printing Unit Offers Easy Integration for Package Printing

- March 2024 Inkjet Installation Roundup

- Inkjet Integrator Profiles: Integrity Industrial Inkjet

- Revisiting the Samba printhead

- 2024 Inkjet Shopping Guide for Folding Carton Presses

- The Future of AI In Packaging

- Inkjet Integrator Profiles: DJM

- Spring Inkjet Update – Webinar

WhatTheyThink is the official show daily media partner of drupa 2024. More info about drupa programs

© 2024 WhatTheyThink. All Rights Reserved.