Over the past couple of weeks, some news stories caught my eye that were more important to our industry than most realize.

P&G Emphasizes the Low Cost & Success of Social Media

The CEO of Procter & Gamble made headlines with a desire to cut its $10 billion ad budget with a comment about media that rattled the advertising world. He said, “With things like Facebook and Google and others, we find that the return on investment of the advertising, when properly designed, when the big idea is there, can be much more efficient. One example is our Old Spice campaign, where we had 1.8 billion free impressions.” The words became a bit distorted indicating that “social media is free,” which of course it is not, but each additional impression reaches the “free” stage very quickly in digital media.

This story came out about the same time that Facebook released information about its initial public offering, valuing the company at about $100 billion (as I mentioned last week, that's about 25% more than the value of the entire commercial printing industry at 20x before-tax profits for the last four quarters). Facebook now has more than 845 million users, and more than 350 million of them also access Facebook with a mobile device. Obviously, P&G has a great interest in reaching Facebook users, since almost every living person can use some kind of P&G product.

Tablet Computer Ownership Doubles in Less than Two Months

Speaking of living beings, the Pew Internet Survey reported a near doubling of U.S. tablet computer owners in about a 4-6 week period: “The share of adults in the United States who own tablet computers nearly doubled from 10% to 19% between mid-December and early January and the same surge in growth also applied to e-book readers, which also jumped from 10% to 19% over the same time period.” Pew also stated that 36% of households earning more than $75,000 now have tablet computers, and almost one-third of those with college educations had them. There was a big leap in ownership for consumers under 50 years old. It has been rumored that Apple will officially introduce the iPad 3 in early March and sales will begin in early April, which should spur additional adoption.

Apple Profits are the Only Profits

According to an analyst interviewed on Bloomberg, Apple's profits in calendar Q4-2011 were $13.1 billion, which exceeded average analyst projections by 36%, and revenue beat their forecasts by $7.3 billion, with sales in the quarter of $46 billion. Great, Apple had an excellent quarter, and there's good reason why the stock broke the $500/share level. Except that's not the interesting story.

Apple is in the S&P 500 index, which had a gain in profits for calendar Q4-2011 of +4.4%. But if you drop Apple out of the calculation, the remaining “S&P 499” shows a decline of -4.2%. Now that's a story. So Apple’s $13 billion in profits, more than 25% of its revenues, is distorting the rest of the stock market. The disparity in performance is so large that investors are worried about diversification in exchange traded funds (ETFs); Apple's value now represents 16% of the value of the NASDAQ 100 index.

What's It All Mean?

The recent December printing shipments report was disappointing. The data continue to reflect a media trend that does not de-emphasize print, but selects other means to accomplish media-related tasks. Therefore, print in all formats declines accordingly. When the P&G CEO asserts the desire to increase social media use, it means that the company is decreasing all of its media, including broadcast, but rarely eliminating media formats. This ties in one of the fallacies found in surveys of media preference. Most media users in today's marketplace will have a preference for one medium over another, but they spread their time over many media. It's like the old saying about love, but it's about media: if I can't have the medium I want, I'll use the medium I'm near. Preference is almost meaningless; it's the actual behavior that matters, and the actions and transactions that result from that behavior. Print volume is a function of page size, number of pages, run length, and frequency, and not about preference. People can always prefer or like something, and just use it less often or use less of it, or use more of it.

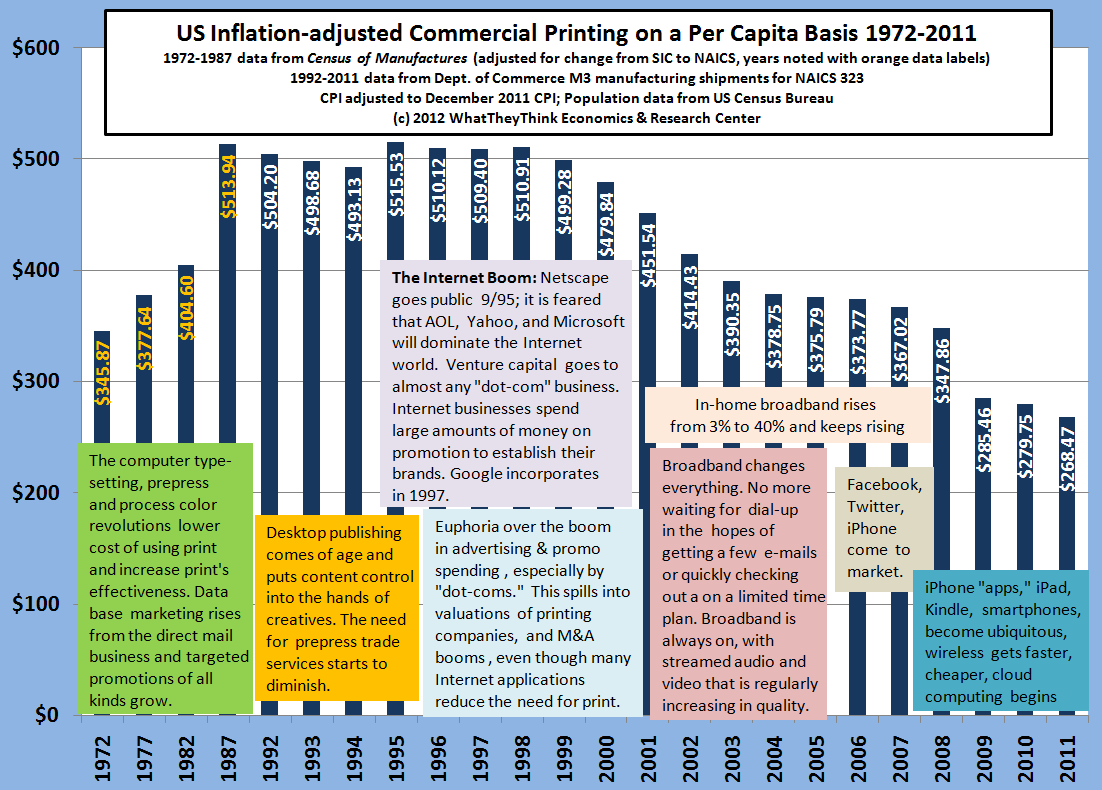

The chart below shows the change in commercial printing on a per capita basis from 1972 to 2011. In last week's blogpost, it was just a plain bar chart. I've now cluttered the chart up with notes, so it's worthwhile clicking on it to enlarge it (you may have to click more than once). The notes show the technological and economic factors that were in play for each period.

The data reminds me how much I miss the industry of the late 1970s and the 1980s (except for the music). From 1982 to 1987, commercial print per capita increased more than $100 per person. The full timeline is a clear reminder of how much things have changed in the way we use print, and the various events that occurred or drove the changes at the time. In that period, data bases were getting better and cheaper, and direct marketers were finally able to target subsets of their audiences. There was an explosion of specialty catalogs, facilitated by toll-free 800 phone numbers and by the ability to pay for orders by credit card over the phone. Newspaper insert volumes grew. Magazines started to explode because of process color printing. Why? Because other media formats, especially broadcast, were more expensive, and print was a better total cost alternative, and could be targeted to audiences with greater precision.

We're used to the concept of inflation adjustment, but we're not always familiar with population adjustment. Rescaling numbers to a per capita, or per person, basis does that. Remember, population grows at just under 1% per year in the U.S. (That is one reason why packaging markets are attractive, of course. Populations grow, and people live longer. The average age of death increases by about three months every year. This means that the U.S. population has steadily longer lives in which to consume goods and services, providing a safety net for the packaging business.) Commercial print would benefit from a rising population if there were no technological alternatives to it. As we can see from the chart, the years 1972-1987 saw a per-person rise in the use of print because our production costs (which were barriers to using print) dropped rather precipitously due to the introduction of phototypesetting and eventually various forms of color digital prepress. This expanded the market for print, even though the economy from 1972 to 1982 was always difficult and often somewhat horrid. Since 1987, the story is a bit different. Remember that Internet bubble where all businesses, including the commercial print business, seemed to be booming? Per capita consumption of print was flat. Since 1987, per capita consumption of print has dropped by about half, with most of the decline, about $20 per year, occurring since 2000.

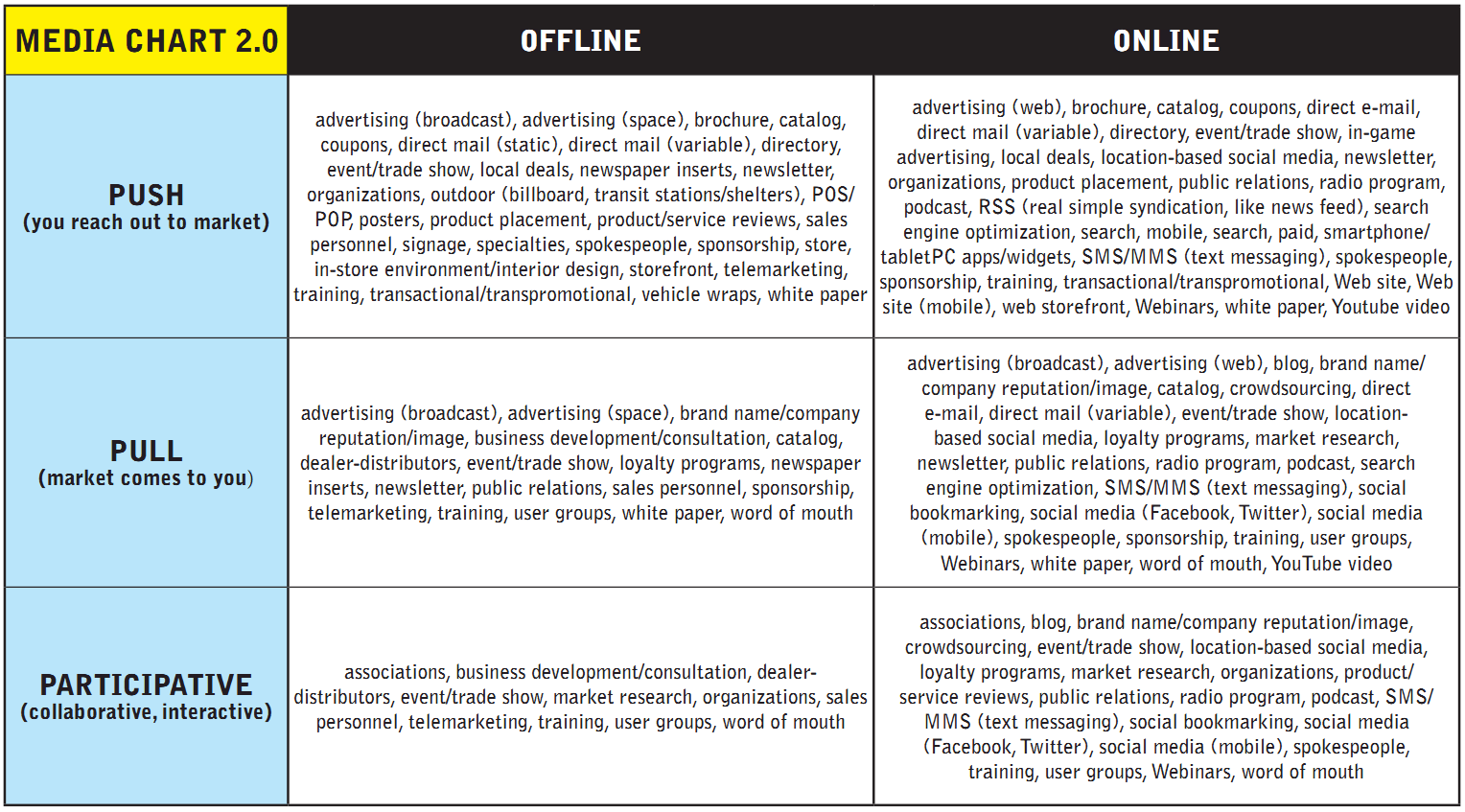

The Explosion in Media Formats

Richard Romano and I have been regularly updating our media chart which became the basis for the book Getting Business. It came from our work on Disrupting the Future, which remains a prescription for print businesses needing to understand what lies ahead and what it means for them, their investments, and their employees. Take a look at the updated media chart, and again, clicking on it will make it much easier to read.

I mention this here to remind readers that it has been about six years since some very disheartening words were uttered at an event hosted by Outsell, Inc. The company is a marketing consulting firm targeted at large companies and their communications professionals. Those words were, “print can be a legitimate spinoff from the Web.” It was quite a surprise to many who heard the words “can” (we had always believed that print was the backbone of communications plans), “legitimate” (Wait a second, print changed the world from the Reformation and various upheavals and revolutions to today, and now print's legitimacy is being questioned?) and “spinoff” (Gosh, 'spinoff'? You mean print is like “The Ropers” were a spinoff of “Three's Company” or “Maude” was a spinoff of “All in the Family”?)

It has become somewhat common to claim that one's media is the “backbone” of the communications process. It has been claimed by print, e-mail, and social media. Just by looking at the media chart, you know that none of that is true. Just by experience, we know that voice is a more reasonable backbone of communications, because of our interactions in person and on the phone, and voice is an integral part of all video, broadcast, and radio. But voice also originates from somewhere... It turns out that the backbone of all communications is not any specific medium, but the backbone is the idea behind the message. More and more, and as younger executives become involved in decisions related to advertising, public relations, and communications, they will not think of a single medium at a time to deploy their messages to their marketplaces, but think of several at one time. Many times they won't even think of media, but think of design elements, such as words and images, and immediately consider how they will be uniquely deployed across multiple media. These new executives think of multiple media all at once in a concurrent manner, not as individual mediums in an assembly-line and serial fashion. We need to be thinking that way as well.

Fortunes are being built without print or with only token amounts of it. Today's communications behemoths Apple, Google (whose ad revenue is about to exceed the print ad revenue of the entire U.S. newspaper industry), and Amazon (which has been selling more e-books than hard copies since the middle of 2011), all have moved up in the company rankings as information businesses or information facilitators, and they still have more to go.

It's Time to Get Out Ahead of It

There are many print businesses doing marvelous things in multiple channel communications, and they are distinguishing themselves from the commodity approach to marketing services (there, I said it... print buyers often say all printers are alike, and we're on the verge of all marketing services providers being alike, too). Profits in the industry are actually rising, which means that even though the number of printing establishments is declining, and our total employment is decreasing, and our share of GDP is getting smaller, the culling of weak companies seems to be occurring faster than usual. This is how markets are remade, even if it pains us to acknowledge it. This means that there are print businesses adapting to the media realities, but there are always some doing so better than others.

It's time for the industry to stop focusing on “saving print” and focus on the entrepreneurial challenges of re-creating and re-invigorating the business we once referred to as “print.” It's time to take a good hard look at that media chart and realize that communications has become more complex and more interesting, and re-position our businesses and capital investments to take advantage of that. The more confusing and the more difficult it becomes to communicate with a marketplace, the more opportunities there are for specialists to emerge in deployment and implementation.

In last week's blog, I assigned “homework,” and am doing so again. Renewing the Printing Industry is still available for free download. Though it was written before social media and smartphones made their recent mark, it still resonates. I was told by an industry consultant who works directly with printing companies that it's the best of the books I have written because of its basic approach and its outline of alternative core strategies for print businesses. Disrupting the Future is also available as a free download and has its own free resource page. Disrupting is the more popular of the two books, and if you read it before, it may be worth reading again. It is in process of being translated to Portuguese, Spanish, Russian and Japanese.

The issues that our industry is dealing with, which I believe will intensify in 2012, are all discussed in these books. Most of all, the books remind us that staying just a bit ahead of clients and prospects is the best and most insightful way to ensure that we have a future of our own creation. If you don't work to craft the future you want, you'll be stuck with the future you'll get. (Wish I was the first one to ever say that!)

Order copies of Dr. Webb's latest books, Getting Business, Does a Plumber Need a Website, and Changing Our Mindset. Click here.